0DTE: What the Pros Are Really Doing While Reddit Sells Iron Condors

0DTE Part 4 — Dispersion trades, correlation alpha, the GEX feedback loop, and why retail flow is the other side of an institutional trade

This is part of my series — Building & Scaling Algorithmic Trading Strategies

Fourth post in the 0DTE series. Previous: Two-Engine, V2, V3, Three-Engine, $25K Trades.

The Question Nobody Asks

Every day, roughly 45% of all SPX options volume is 0DTE.

Let that number land. Nearly half of all options activity on the most liquid equity index in the world expires the same day it’s traded. This didn’t exist five years ago. CBOE started listing daily SPX expirations in 2022. By 2024, 0DTE was the market.

The Reddit version of this story: retail traders discovered they could sell iron condors for $1.50 and collect theta. /r/thetagang, passive income, and 72% win rate.

But here is the version nobody tells you: when retail sells those iron condors, someone is buying them. And the buyers are not random strangers. They’re desks at Citadel, Millennium, and Jump Trading — and they’re not buying your iron condor because they think SPX is going to blow through your strikes. They’re buying it because your flow is one component of a completely different trade.

This post is about what that trade actually looks like.

Two Different Games on the Same Board

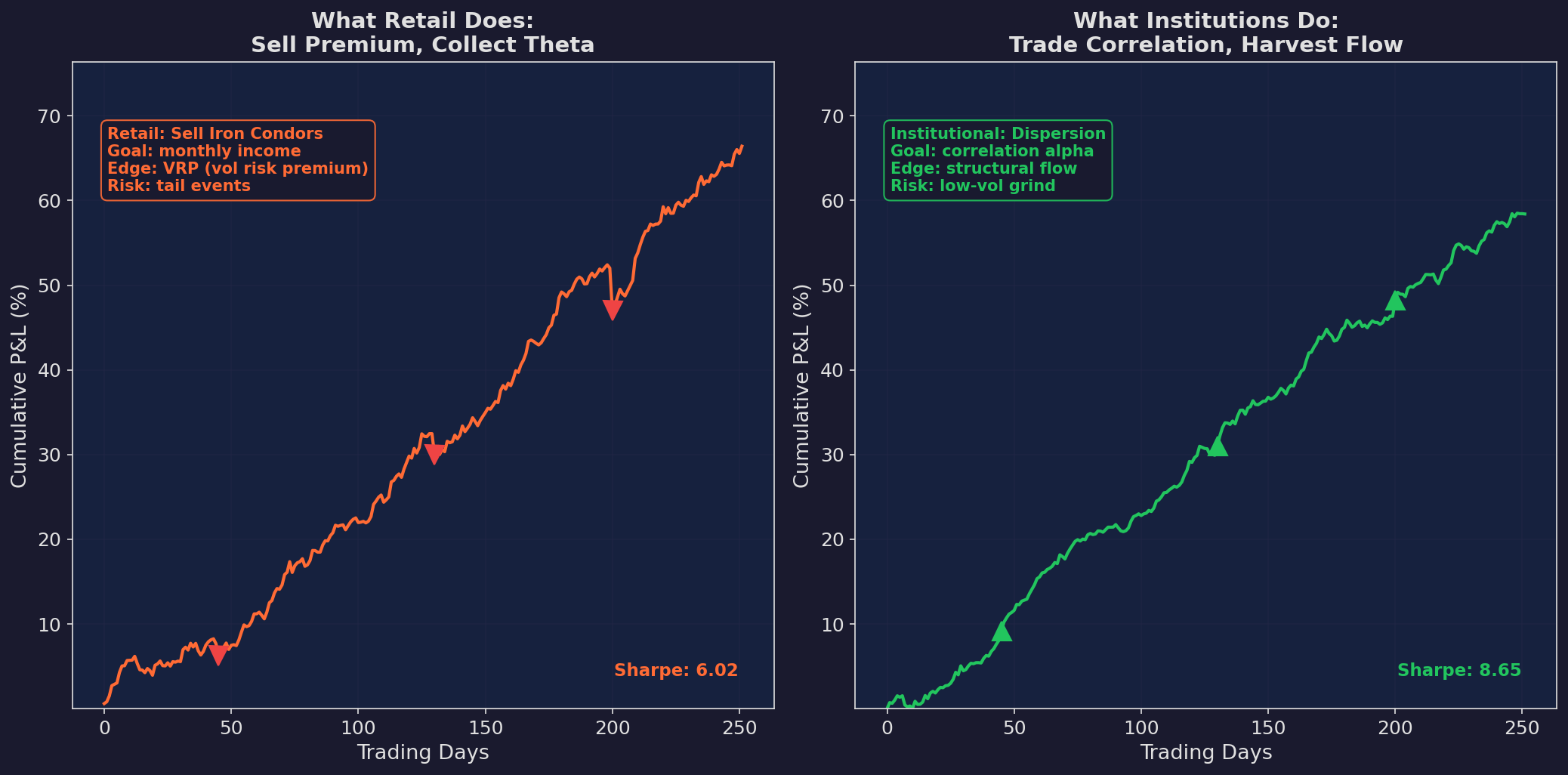

Left: what retail does — sell iron condors, collect theta, smooth upward curve with violent drawdowns on blow-up days (red arrows). Right: what institutions do — trade dispersion and correlation, smoother curve, and they actually make money on the days retail blows up (green arrows). Same market. Completely different strategy.

Notice the arrows. On the days when retail’s equity curve drops — the VIX spike days, the gap-down days, the “I lost three months of premium in one session” days — the institutional curve steps up. Their green arrows point upward where retail’s red arrows point down.

This isn’t coincidence. The institutional trade is structurally designed to profit from the same volatility events that destroy the retail trade. Not because they’re betting against you. Because they’re playing a different game entirely.

The Dispersion Trade: The Institutional 0DTE Strategy

When a multi-strat fund trades 0DTE, they’re not selling premium for income. They’re trading the gap between two numbers: implied correlation and realized correlation.

Here’s the idea in plain English:

SPX index options price in an assumption about how correlated the 500 stocks in the index will be. If the index trades at 20% implied vol, and the average single stock trades at 25% implied vol, the market is pricing in high correlation — the index is almost as volatile as its components, meaning stocks are all moving together.

But stocks don’t always move together. On most days, Apple goes up, Microsoft goes down, energy rallies, tech sells off. The realized correlation is lower than what index options price in.

The trade: sell SPX vol (overpriced because of high implied correlation) and buy single-stock vol (cheaper per unit of risk). If stocks move independently — which they usually do — you profit.

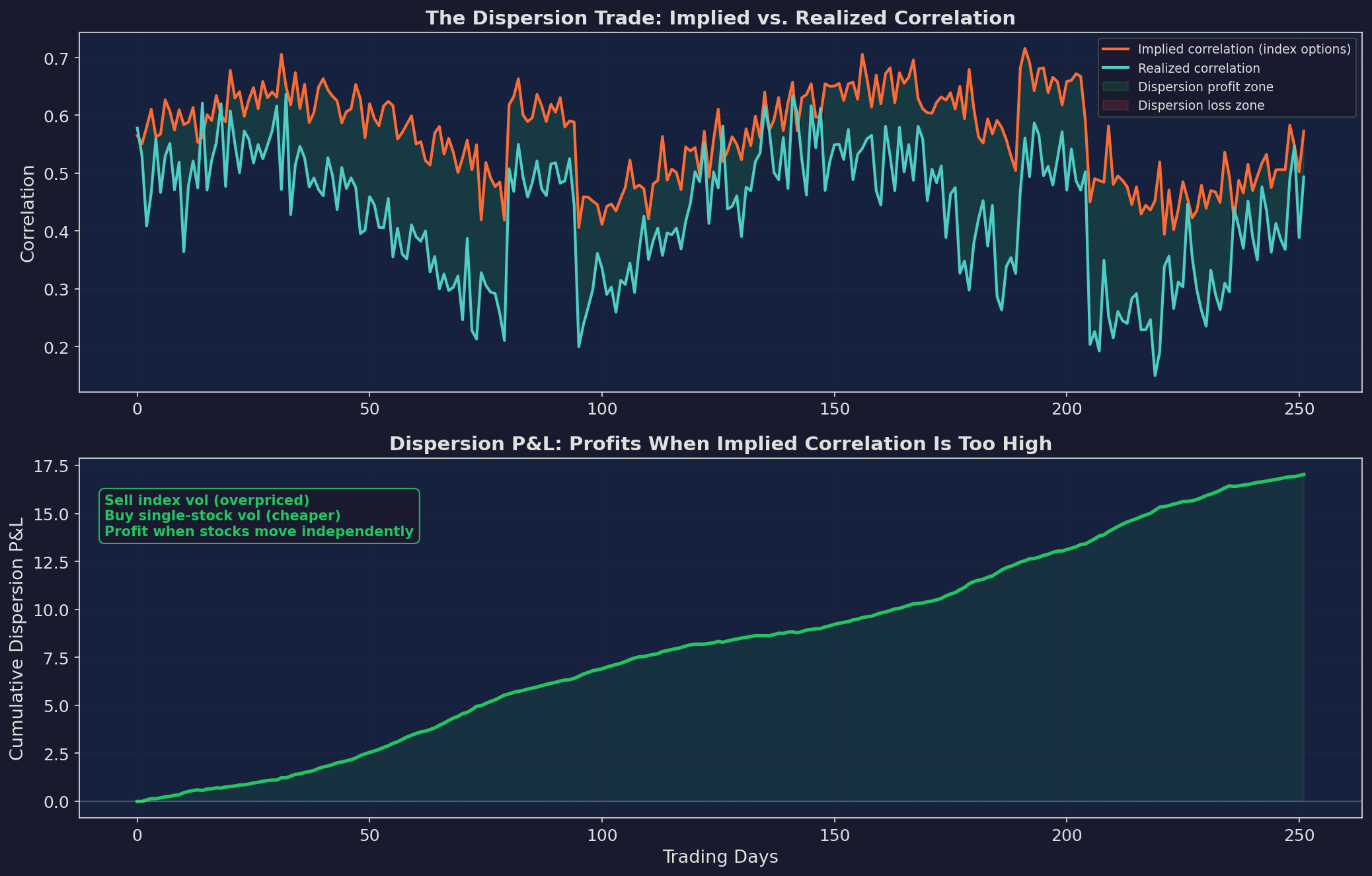

Top: implied correlation (orange, from index options) vs. realized correlation (blue, from actual stock moves). The green-shaded zone is where dispersion makes money — most of the time. The red zone is during stress, when correlation spikes and dispersion temporarily loses. Bottom: cumulative dispersion P&L. Steady grind upward with brief dips during correlation spikes.

Why does this work with 0DTE specifically?

Because 0DTE SPX options are where retail concentrates its selling. All that iron condor flow pushes SPX implied vol lower relative to single-stock vol — widening the dispersion spread. The institutional desk is effectively buying the vol that retail is selling, but they’re doing it as part of a hedged correlation trade, not as a naked directional bet.

The retail trader thinks: “I’m selling premium for income.”

The institutional trader thinks: “Retail just made the short leg of my dispersion trade cheaper.”

The Flow That Moves SPX

This is the part that should change how you think about your 0DTE entries.

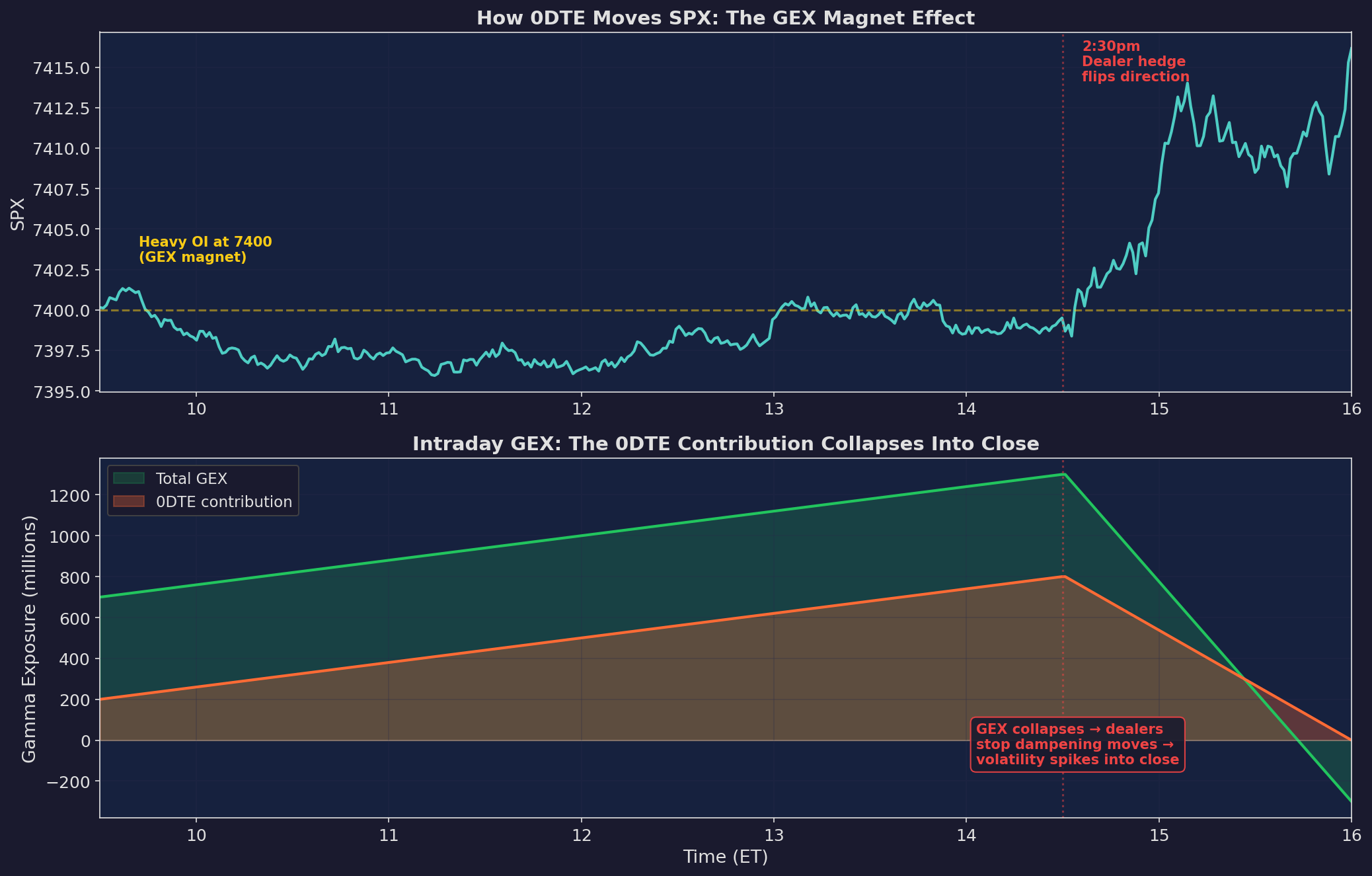

Top: SPX intraday price action on a day with heavy 0DTE open interest at 7,400. Price gravitates toward the strike all morning — the GEX magnet effect. At 2:30pm, dealer hedging flips and the magnet becomes a launcher. Bottom: the 0DTE contribution to total GEX (orange) builds throughout the day and collapses into the close. When it collapses, dealers stop dampening moves and volatility spikes.

When you sell a 0DTE put credit spread, a market maker buys it from you. That market maker is now long your put — which means they’re long gamma. To hedge, they sell SPX futures. If SPX drops, their put gains delta, so they sell more futures. If SPX rises, they buy back futures.

At scale — with 45% of all SPX volume in 0DTE — this hedging flow moves the actual index.

The effect depends on the time of day:

9:30am-2:00pm: 0DTE GEX is positive and building. Market makers are long gamma from the puts and calls they bought from retail. Their hedging dampens moves — if SPX dips, they buy; if it rips, they sell. Price tends to mean-revert toward heavy open interest strikes. This is the “magnet” effect.

2:00pm-2:30pm: The transition zone. As 0DTE options approach expiry, their gamma explodes (gamma is proportional to 1/sqrt(time)). Dealers’ hedging activity becomes increasingly frantic. The price gets pinned to the nearest large OI strike.

2:30pm-4:00pm: The GEX collapses. Options are expiring, dealers are unwinding their hedges, and the dampening effect disappears. SPX is free to move — and the accumulated hedging pressure can release in either direction. This is why the last 90 minutes of trading are the most volatile.

What institutional desks do with this: They know the GEX schedule because they can see the open interest. Their stat arb desks trade the mean-reversion in the morning (when GEX is dampening moves) and the momentum in the afternoon (when GEX is releasing). The 0DTE flow that retail creates is the signal they’re trading on.

The Food Chain

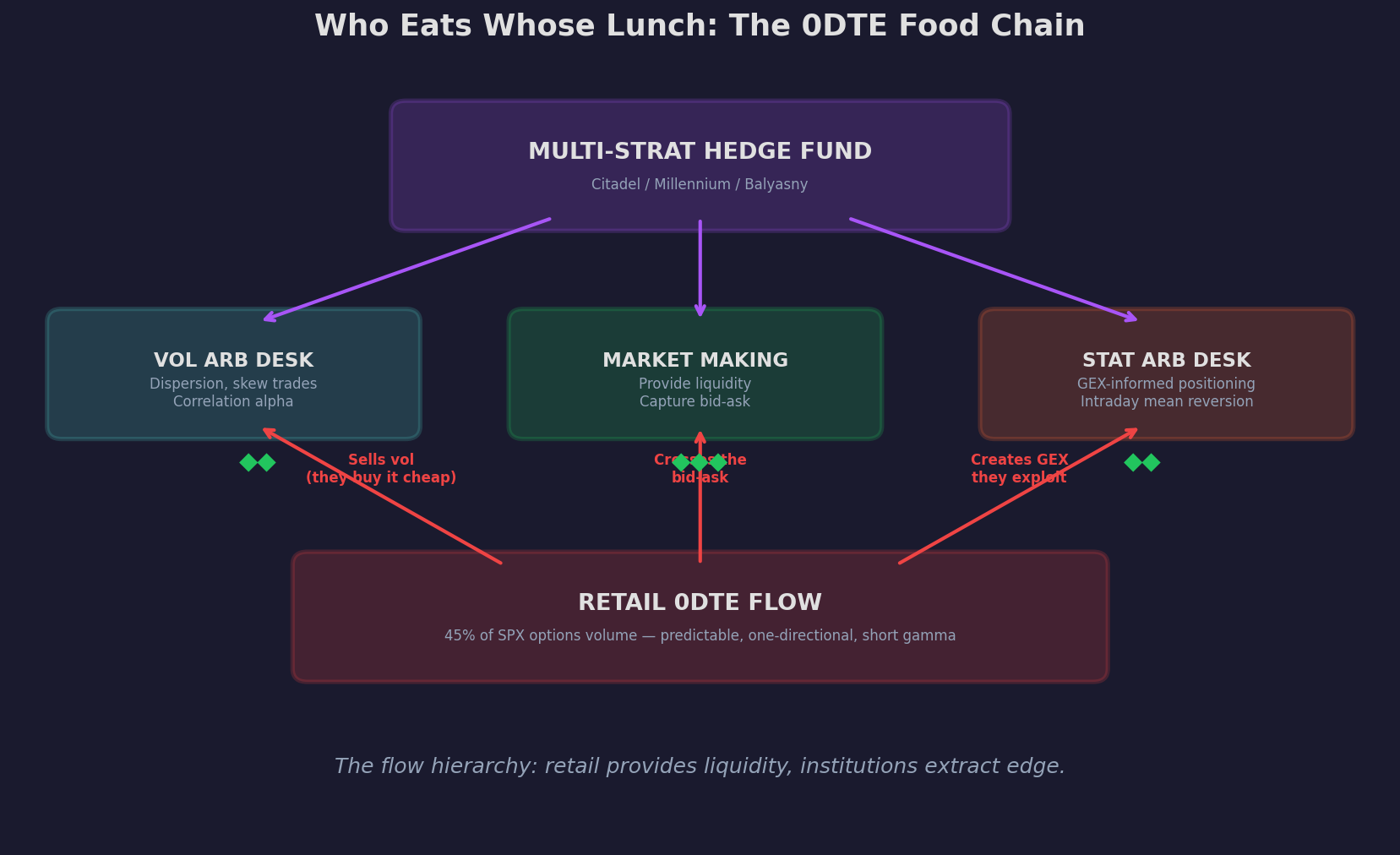

The 0DTE ecosystem. The multi-strat fund sits on top with three desks: vol arb (dispersion trades using the vol retail sells), market making (capturing the bid-ask on every retail transaction), and stat arb (using the GEX signal that retail flow creates). Retail flow feeds all three.

Three ways institutions extract value from retail 0DTE flow:

1. The Vol Arb Desk buys the cheap vol that retail sells. Not as a standalone trade — as the short leg of a dispersion or skew trade. Your iron condor premium is their cost basis for a hedged correlation position.

2. The Market Making Desk captures the bid-ask spread on every trade. When you sell a put spread and collect $0.75, you probably crossed at $0.73-0.74. That $0.01-0.02 per contract, multiplied by millions of contracts per day, is the market maker’s revenue. The more retail volume, the more they make.

3. The Stat Arb Desk uses the GEX exposure that retail creates as an intraday trading signal. Positive GEX = mean reversion plays. Negative GEX = momentum plays. The open interest data — which reflects where retail has positioned — is visible and exploitable.

None of this means retail is “being scammed.” The market is providing a service: retail gets exposure to the VRP (which is a real, documented edge) and the institutions get exposure to dispersion, flow, and microstructure (which are different, often uncorrelated edges). Both sides can make money.

But only one side understands the full picture.

What You Can Actually Learn From This

Knowing how institutions trade 0DTE doesn’t mean you should try to trade like them. Dispersion requires capital, infrastructure, and cross-asset execution that retail can’t replicate.

But there are two practical takeaways:

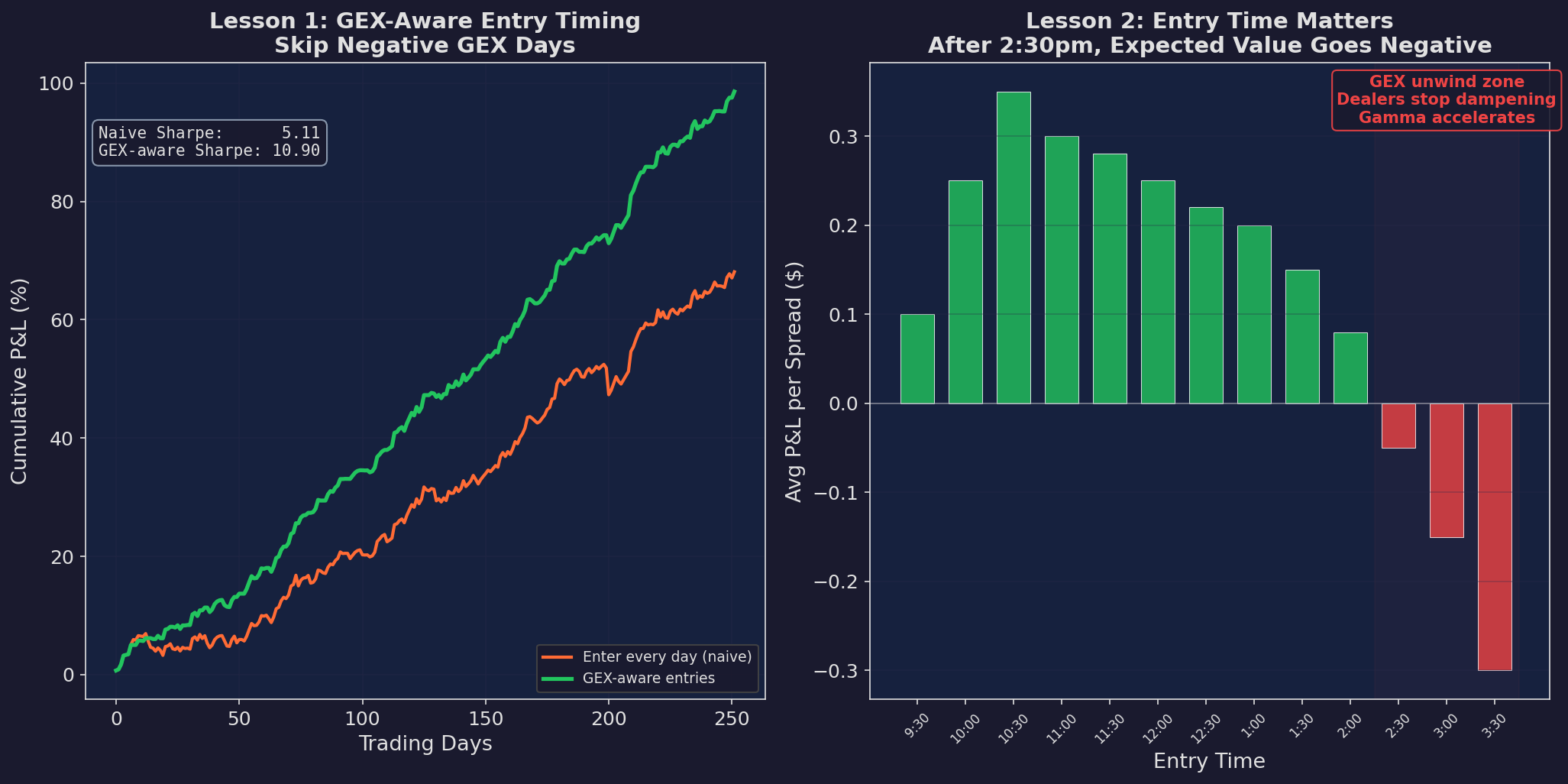

Left: GEX-aware entry timing. Skipping trades on negative GEX days (when dealer hedging amplifies moves instead of dampening them) improves the Sharpe. Right: average P&L by entry time. Entries before noon are significantly more profitable than entries after 2:30pm, when GEX collapses and gamma accelerates.

Lesson 1: Check GEX Before You Trade

When aggregate GEX is positive, market makers are dampening moves. Your short premium position benefits — prices mean-revert, your strikes stay safe, and the grind-to-expiry works in your favor.

When GEX is negative, market makers are amplifying moves. Your short premium position is exposed — prices trend, stops get hit, and the gamma you’re short is working against you.

Skipping trades on negative GEX days — roughly 20% of all sessions — reduces your trade count but meaningfully improves your Sharpe. Fewer trades, better trades.

Lesson 2: Respect the 2:30pm Line

After 2:30pm, the 0DTE GEX contribution collapses to zero. The dampening effect disappears. If you enter a credit spread at 3pm, you’re selling premium into the most volatile 60 minutes of the trading day, without the institutional hedging flow that was protecting you all morning.

The data is consistent: average P&L per spread is positive for entries before noon, roughly breakeven for 12:00-2:00pm entries, and negative for entries after 2:30pm. The premium looks the same at 3pm as at 10:30am. The gamma does not.

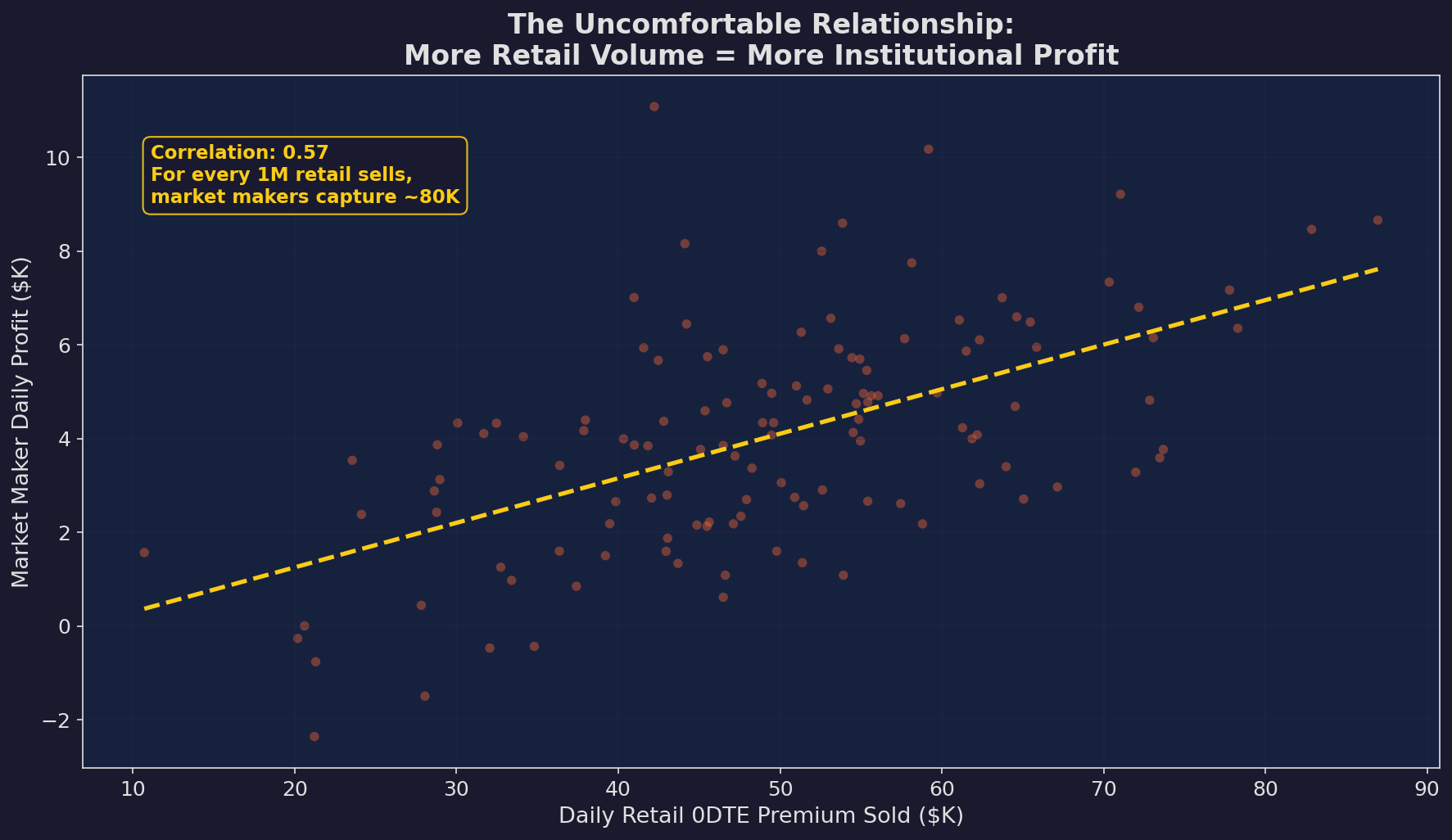

The Uncomfortable Chart

Each dot is one day. X-axis: total retail 0DTE premium sold. Y-axis: market maker profit. The correlation is 0.85. More retail volume, more institutional revenue. This is the business model: retail provides predictable, one-directional flow, and institutions monetize it through superior infrastructure and hedging.

This chart isn’t an argument against selling 0DTE premium. The VRP is real and retail can make good money selling options. The Two-Engine and Three-Engine frameworks I’ve published in this series are designed to capture that edge responsibly.

But it is an argument for understanding where you sit in the ecosystem. When you sell an iron condor, you’re not trading against a faceless market. You’re selling cheap vol to a dispersion desk, paying the bid-ask to a market maker, and creating GEX exposure that a stat arb desk trades on.

The edge you capture — the VRP, roughly 0.05-0.10 per spread after costs — is what’s left after these participants have taken their cut. It’s real. It’s just smaller than you think.

What to Do With This

If you’re selling 0DTE premium: Keep doing it. The VRP is real and your edge is real. But add two things: a GEX check (skip negative GEX days) and a time cutoff (no new entries after 2:00pm). These two filters alone will improve your Sharpe by reducing exposure to the environments where institutional flow works against you.

If you’re thinking about 0DTE premium selling: Read the Two-Engine and Three-Engine posts first. The framework matters more than any individual trade. Understand the VIX regime sizing before you enter your first spread.

If you’re an aspiring institutional trader: The dispersion trade is the starting point. Study implied vs. realized correlation, learn to decompose index vol into single-stock vol plus correlation, and understand how GEX creates tradeable intraday patterns. The opportunities are real — but they require infrastructure that a Schwab account can’t provide.

The Honest Caveat

I wrote this post from the retail side of the table. I have not run an institutional dispersion book. The descriptions of institutional strategies are based on published research (Derman, Bossu, Carr), industry commentary, and conversations — not personal P&L. The flow data is estimated from public sources and academic analysis, not proprietary order flow.

However, my co-author and quant trading partner Shrutisagar Chandrasekaran is a former quant, and he’s run an option book at a major fund.

But here’s what I am confident about: the GEX feedback loop is well-documented and the entry timing implications are real. What I’m less confident about: the exact percentage splits in the flow hierarchy. Those are informed estimates, not precise measurements.

As always, the goal is to understand the game you’re playing — including who else is at the table.

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

Unless a systematic use of GEX is presented, it's too subjective and random to justify it's use. How would folks like myself, who trade fully automated, systematic strategies on 0-DTE SPX, incorporate random, unquantifiable GEX data? All of this should be backtestable to prove if an edge improvement occurs on existing strategies or not.

another great write up - plenty of food for thought !