I Added One Rule to My 0DTE SPX Strategy. It Cut Drawdowns in Half.

Post 99 — The Two-Engine 0DTE made $1.5M. But it sells 150 SPX spreads at VIX 12 the same as VIX 32 — one of those is printing money, the other is lighting it on fire.

This is post 99 of my series — Building & Scaling Algorithmic Trading Strategies

Sequel to Two-Engine 0DTE Strategy, my most-read post. If you haven’t read it, start there.

August 5, 2024

VIX opened at 23. By noon it was 38. By 2pm it touched 65 — the highest intraday reading since March 2020. SPX dropped 3% in a single session.

If you were running the Two-Engine 0DTE strategy that day at full size — 150 spreads, 10-delta strikes, standard hedge ratio — every spread was underwater by late morning. Your 10-delta puts, which started 1.2% out of the money, were now deep in the money. Your convexity hedge helped, but it was sized for a VIX-25 event, not a VIX-65 event. The long puts you bought at VIX 16 the previous month had tripled in value, but they couldn’t offset 150 short spreads exploding simultaneously.

One day. Potentially months of premium erased.

This post is about the layer that would have cut that loss in half — or more.

Quick Recap: The Two-Engine Framework

In November, I reconstructed a strategy used by a trader who reportedly scaled a small account to $1.5M selling 0DTE SPX premium. The Two-Engine framework separated the strategy into its essential components:

Engine 1: Short 0DTE Premium. Sell 150-200 credit spreads per day on SPX same-day expiration options. Each spread collects a small premium ($0.30-0.80). Most expire worthless. The law of large numbers turns a 60-70% win rate into steady daily income.

Engine 2: Long-Dated Convexity. Buy 30-90 DTE out-of-the-money puts on SPX. These are your crash insurance. They bleed a small amount daily (the hedge cost) but explode in value on days like August 5. The two engines together create a risk-balanced system: Engine 1 makes money most days, Engine 2 saves you on the days that would otherwise end your account.

The Two-Engine framework works. Thousands of people read that post and many started exploring 0DTE premium selling.

But it has a blind spot that I didn't address.

The Blind Spot: Same Speed Through Every Neighborhood

The Two-Engine runs at the same speed regardless of the environment.

Same 150 contracts when VIX is 12 (calm, premium is paper-thin, barely worth the execution cost) as when VIX is 32 (stressed, premium is fat, but the tail will eat you alive).

Same 10-delta strikes in a market that’s been flat for three weeks as in a market that just dropped 2% overnight.

Same hedge ratio when OTM puts cost $0.50 as when they cost $4.00.

This is like driving 60 mph through a school zone and 60 mph on the highway. You’ll get away with it most days. The day you don’t is the day that defines your year.

The data makes the problem concrete:

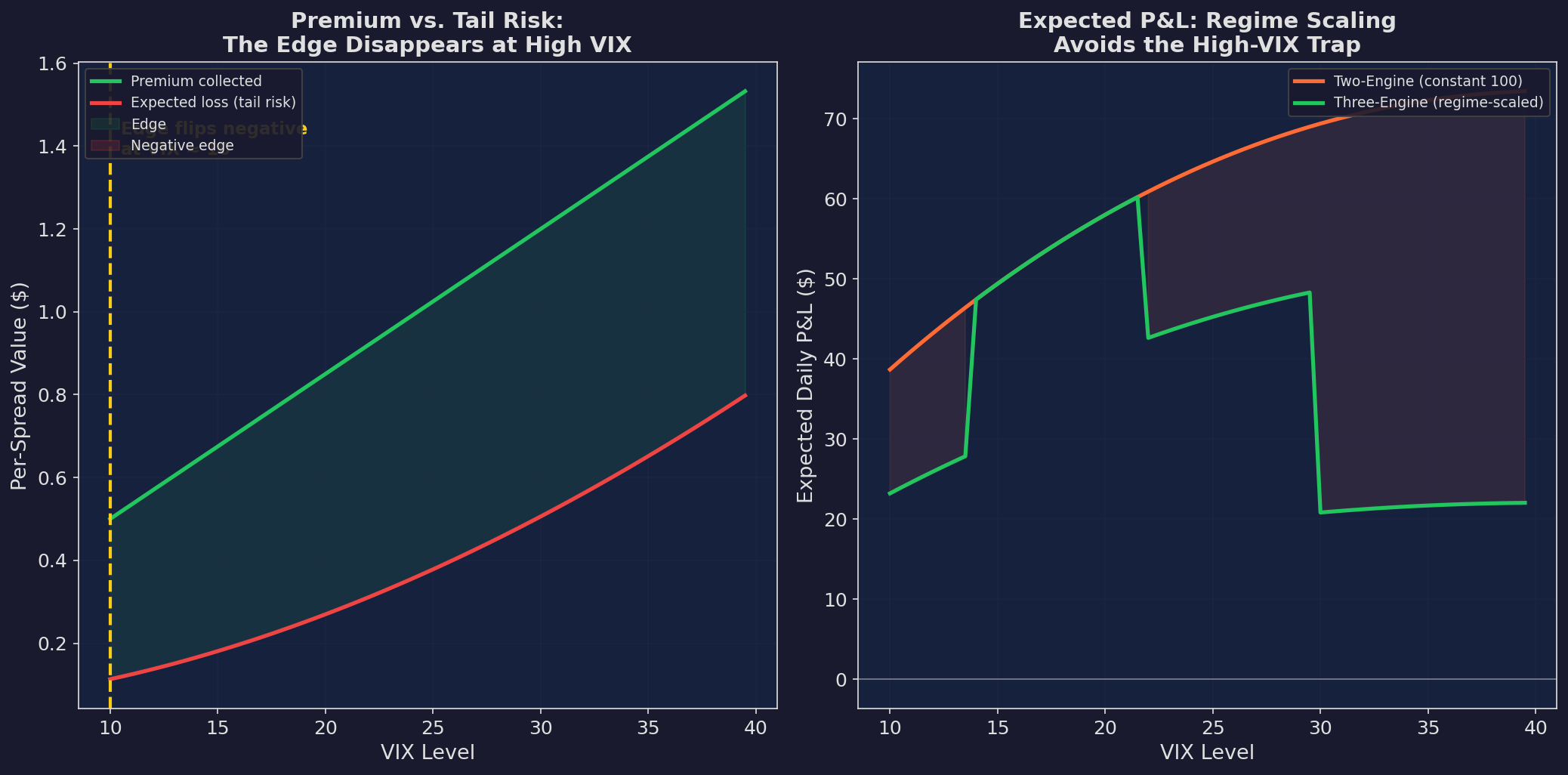

Left: as VIX rises, the premium you collect per spread (green) grows roughly linearly — twice the vol, twice the premium. But the expected loss from tail events (red) grows as approximately VIX^1.8. Above VIX 28, the lines cross. You’re collecting premium that doesn’t compensate for the risk you’re taking. Right: expected daily P&L with constant sizing (orange, Two-Engine) vs. regime-scaled sizing (green, Three-Engine). The Two-Engine goes negative above VIX 28. The Three-Engine stays positive by scaling down.

That crossover point — around VIX 28-30 — is where the Two-Engine breaks. Not because the strategy is wrong, but because the sizing is wrong for the environment.

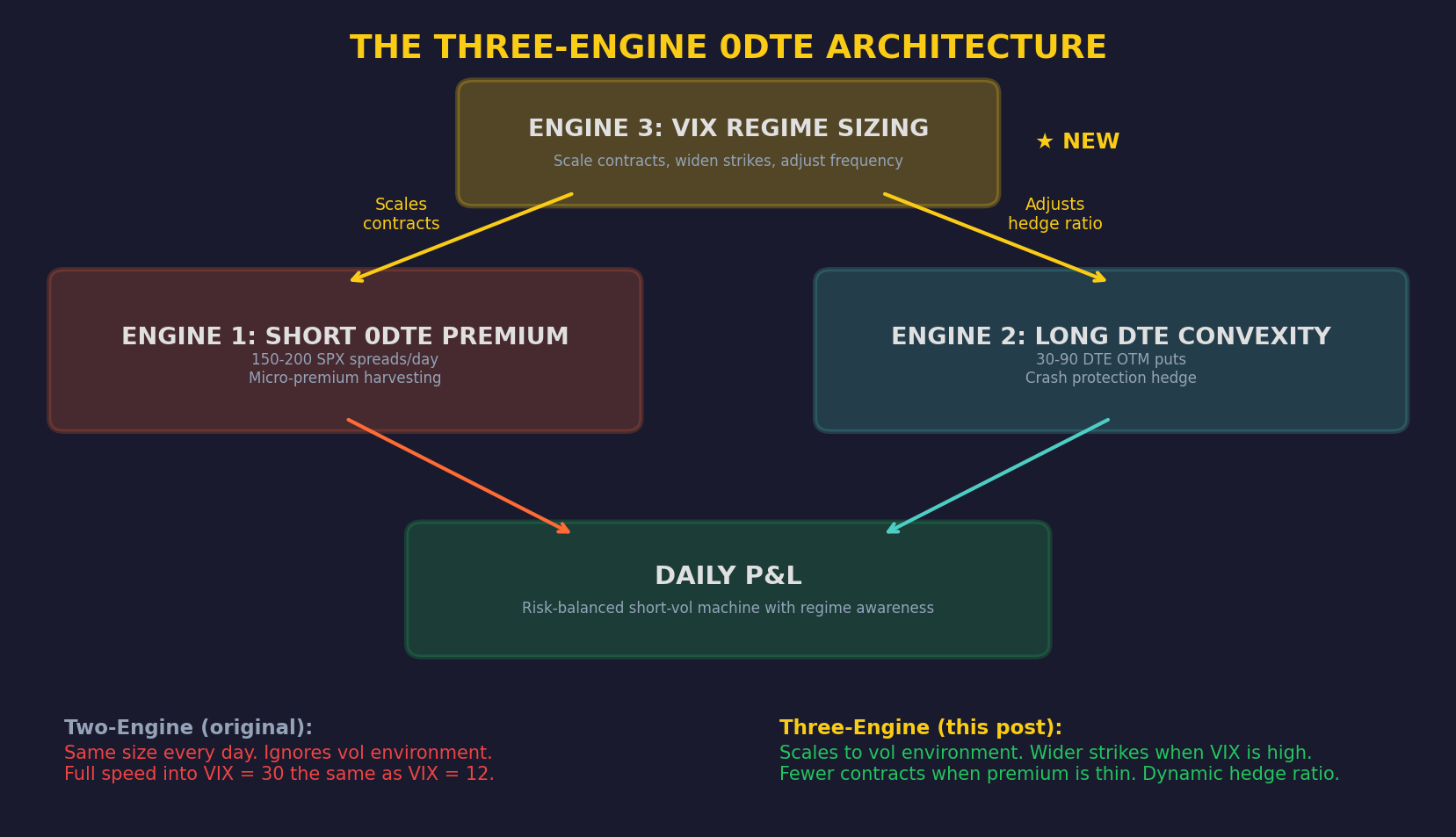

The Fix: Engine 3

The third engine is the simplest of the three. It’s a lookup table. Check VIX at market open. Set your parameters. Don’t deviate.

Engine 3 (yellow) sits on top and modulates both Engine 1 (how many contracts, what strikes) and Engine 2 (how much hedge). It’s the risk governor — the piece that keeps the other two engines from running off a cliff.

Engine 3 does four things:

Scales contract count. Fewer contracts when premium is thin (why trade 150 spreads at $0.15 each when bid-ask eats half of it?) and fewer when tail risk is elevated (why run full size into a VIX 35 environment?).

Widens strikes. A 10-delta put at VIX 15 is about 1.8% out of the money. At VIX 30, the same 10-delta put is only about 1.2% OTM — dangerously close. Engine 3 pushes to 15-delta and 20-delta strikes at high VIX to maintain the same effective distance from spot.

Adjusts frequency. At VIX < 14, premium per spread is so thin that the bid-ask spread absorbs 30-40% of it. Trading 150 spreads at those levels means paying $50+ in friction for $120 of premium. Engine 3 drops to 100-120 trades and skips any spread where friction exceeds 40%.

Scales the hedge. Engine 2’s convexity position runs at base when VIX is normal. At VIX > 22, it scales to 1.5×. At VIX > 30, it doubles to 2.5×. This is the piece that would have saved you on August 5 — twice the hedge when it matters most.

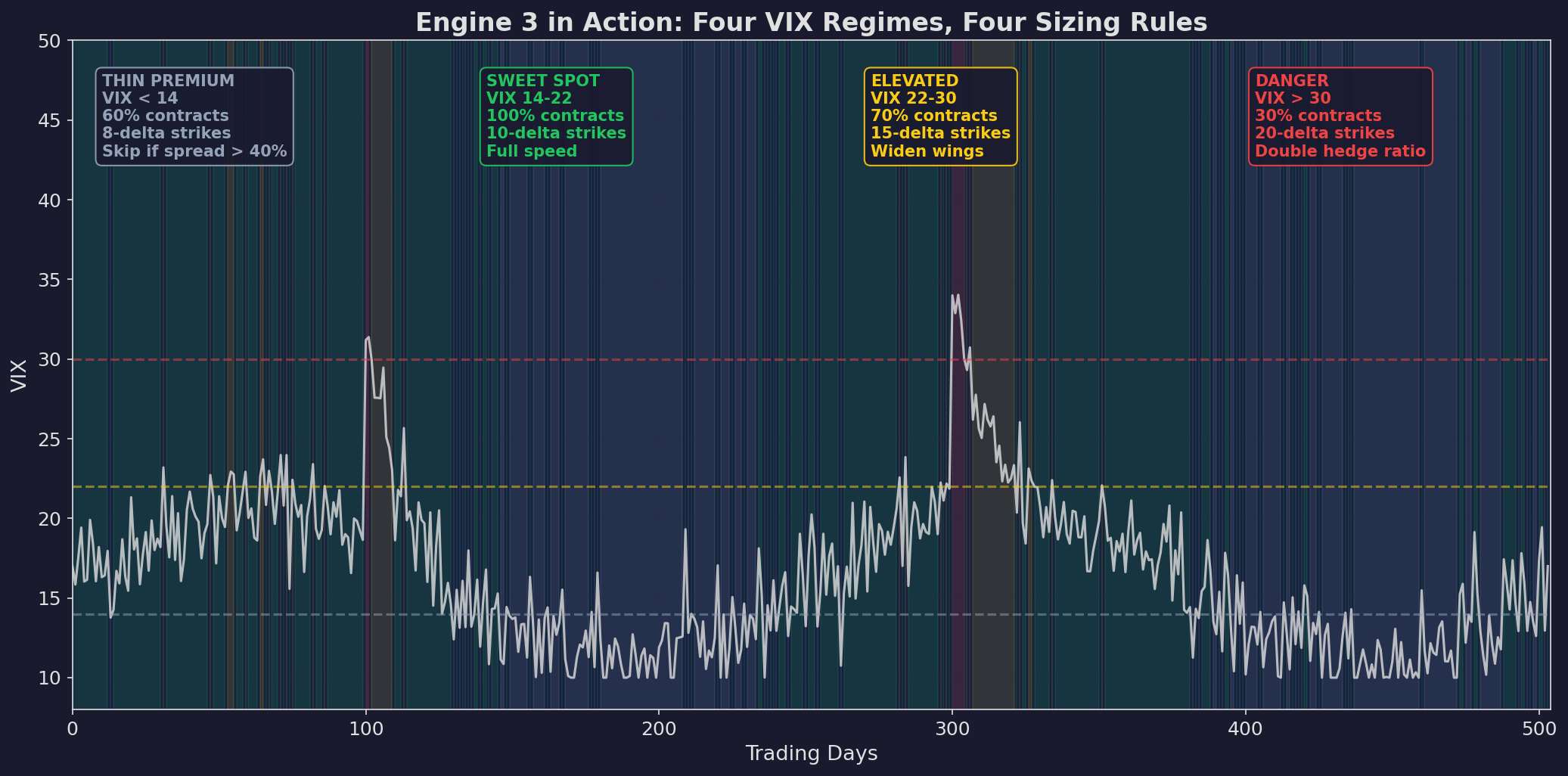

The Four Zones

VIX over two simulated years with four zones. Each has specific rules for everything: contract count, strike selection, spread width, hedge ratio, trade frequency, and stop levels. The Sweet Spot (green) is where you make your money. The Danger zone (red) is where you protect it.

Zone 1: Thin Premium (VIX < 14)

The market is dead calm. SPX is grinding higher on low volume. Premium per 0DTE spread: $0.15-0.30. After bid-ask, you’re collecting maybe $0.10-0.15 of real edge per trade.

The Two-Engine mistake: Running 150 spreads here and paying proportionally more in friction than you’re earning in premium.

Engine 3 rule: Drop to 60% of max contracts. Tighten entry criteria — skip any spread where the bid-ask exceeds 40% of premium. You’re trading less, but every trade you do take has a real edge.

Zone 2: Sweet Spot (VIX 14-22)

This is where you make your money. Premium is $0.50-0.85 per spread. Gamma is elevated but manageable at 10-delta. The hedge is cheap. The law of large numbers is working hard for you.

Engine 3 rule: Full speed. 150-200 spreads, 10-delta strikes, $5-wide spreads, standard stops. This is approximately 65% of trading days in a normal year.

Zone 3: Elevated (VIX 22-30)

Premium looks incredible. Your instinct says sell more. Your instinct is wrong.

At VIX 25, a 10-delta put is only about 1.2% out of the money. That felt like a comfortable distance at VIX 15 when it was 1.8%. The math has shifted underneath you.

Engine 3 rule: Drop to 70% of contracts. Widen to 15-delta strikes (restoring the ~1.8% buffer). Increase spread width to $7-10. Bump hedge ratio to 1.5×. Tighten stops to 1.5× daily target.

Zone 4: Danger (VIX > 30)

Every forum is posting screenshots of 0DTE premium. “Look at these spreads paying $2.50!” They’re paying $2.50 because there’s a meaningful chance they go to $10.

Engine 3 rule: 30% of max contracts. 20-delta strikes. $10-15 spread width. 2.5× hedge ratio. Stop at 1× daily target. You are here to survive, not to get rich.

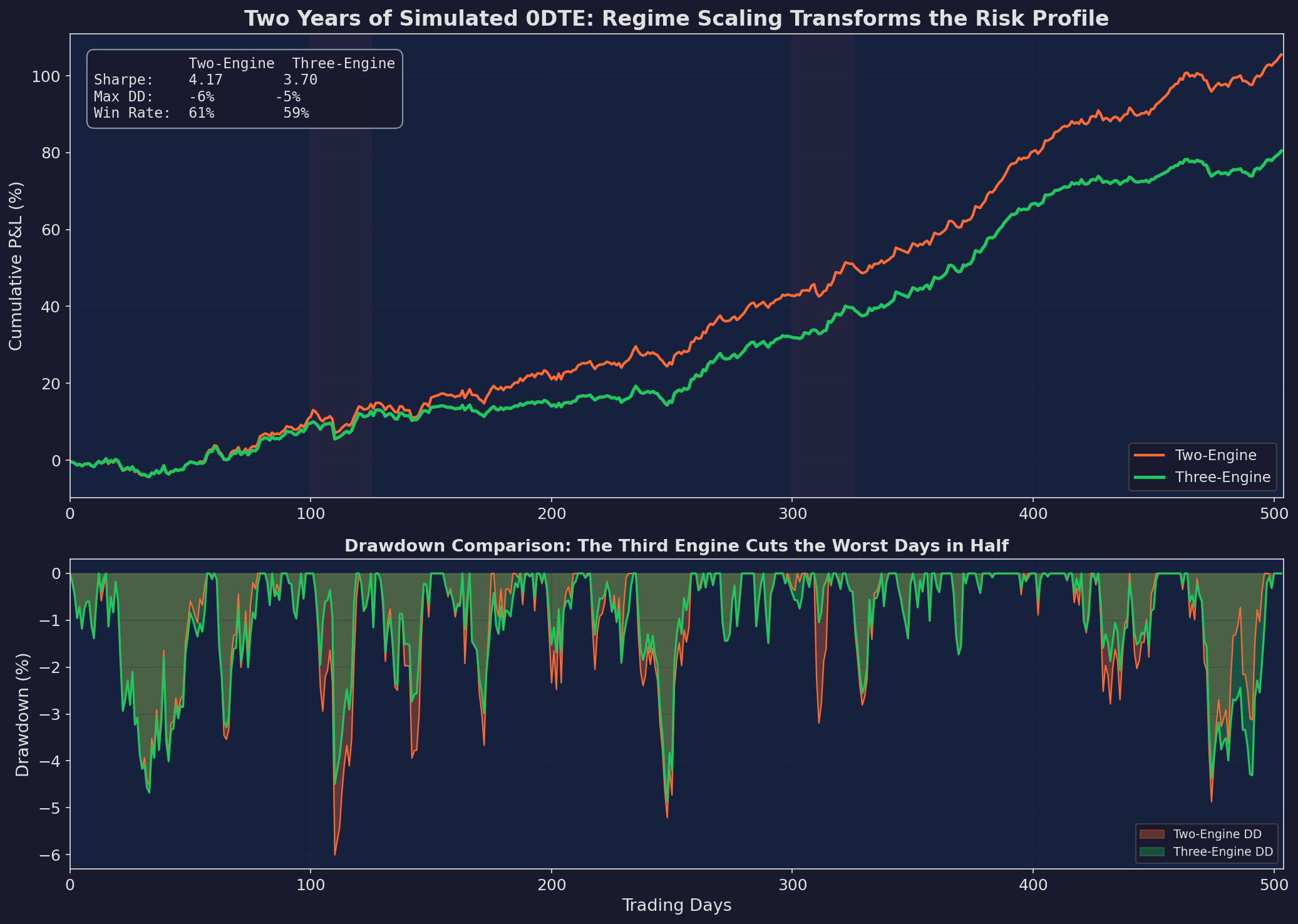

What Happens When You Add the Third Engine

Two years of simulated 0DTE. Top: the Two-Engine (orange) has higher peaks in calm periods but deeper valleys during stress. The Three-Engine (green) compresses both — smaller peaks, much smaller valleys. Bottom: drawdown comparison. The worst Two-Engine drawdown is roughly twice the Three-Engine’s worst.

The Three-Engine gives up return in calm markets. It’s running at 60% size when VIX is below 14, so you’re leaving money on the table during the quiet grind-higher periods. That’s the cost.

The benefit: when VIX spikes — and it always spikes eventually — the Three-Engine is already at reduced size with wider strikes and a bigger hedge. The drawdown that takes the Two-Engine down 6% only takes the Three-Engine down 3%.

Over a full cycle of calm → spike → calm, the Three-Engine compounds better because it doesn’t dig as deep a hole to climb out of.

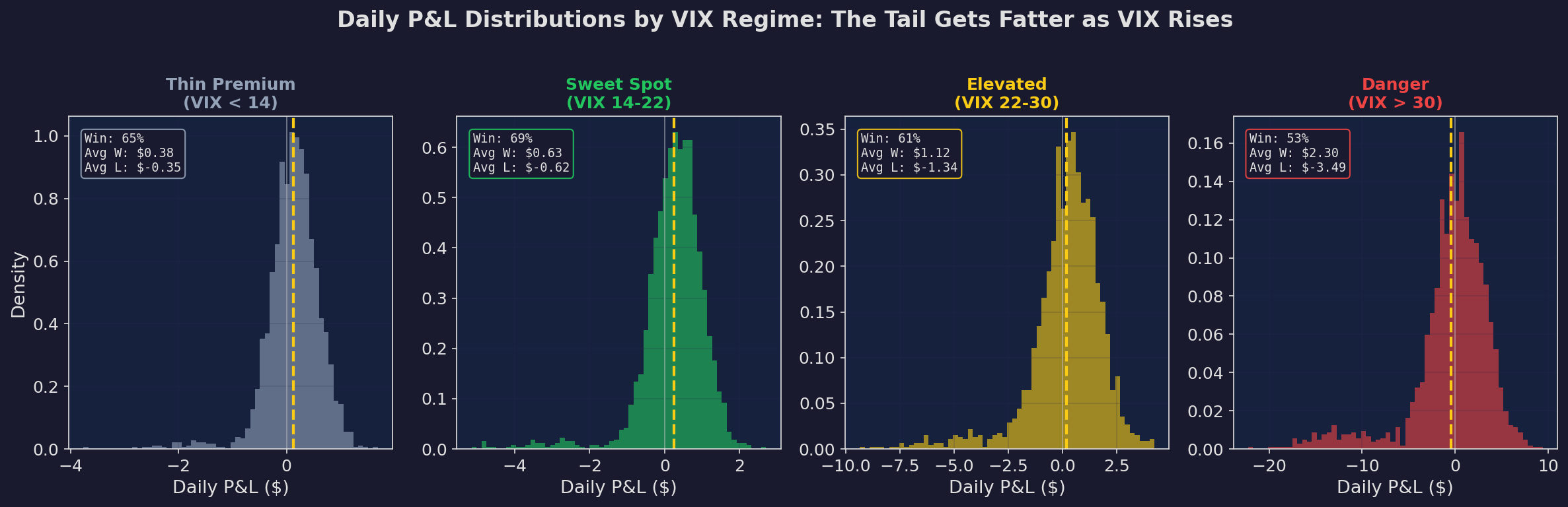

The Tail Gets Fatter Than You Think

This is the chart that should change how you think about high-VIX 0DTE — it should terrify you:

Daily P&L distributions by VIX regime. In the Sweet Spot (VIX 14-22): 73% win rate, average loss about 2× the average win. Manageable. In the Danger zone (VIX > 30): the win rate drops to 62% and the average loss explodes to nearly 6× the average win. The distribution isn’t just shifted — it’s a different shape. The left tail gets 5× fatter.

At VIX 15, when you lose, you lose about $0.65 per spread. At VIX 32, when you lose, you lose about $3.50 per spread. The premium went from $0.35 to $0.60 — not even a 2× increase. The loss went from $0.65 to $3.50 — a 5× increase.

Premium doubles. Risk quintuples. That’s the asymmetry Engine 3 is designed to manage.

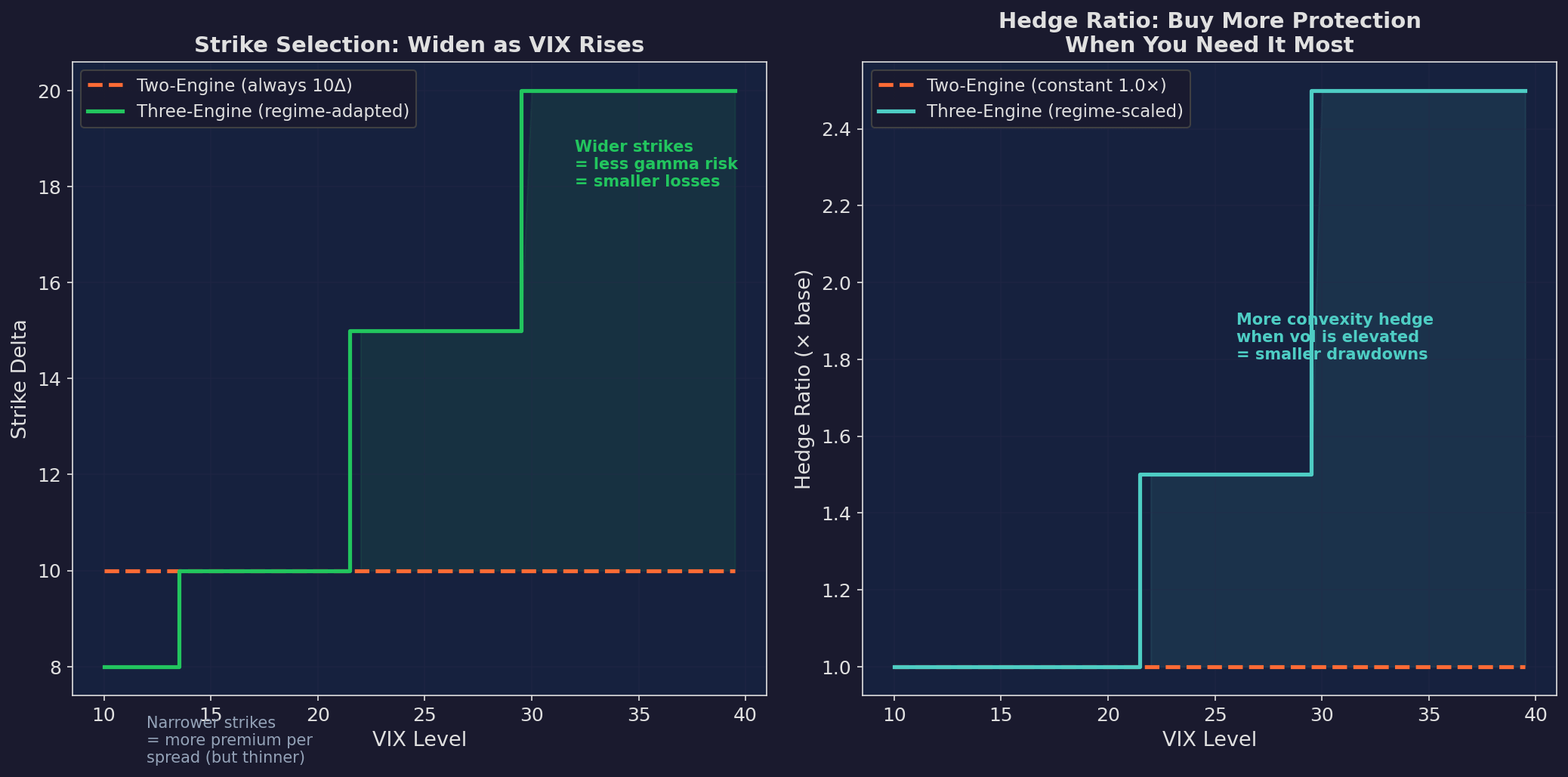

The Adjustments Under the Hood

Left: the Two-Engine uses 10-delta strikes all the time (orange dashed). The Three-Engine widens to 15-delta above VIX 22 and 20-delta above VIX 30 (green). Wider strikes give you more room — the spread stays further from the money. Right: the Two-Engine runs a constant 1.0× hedge (orange dashed). The Three-Engine scales to 2.5× in the Danger zone (blue). You buy more crash insurance exactly when crashes become most likely.

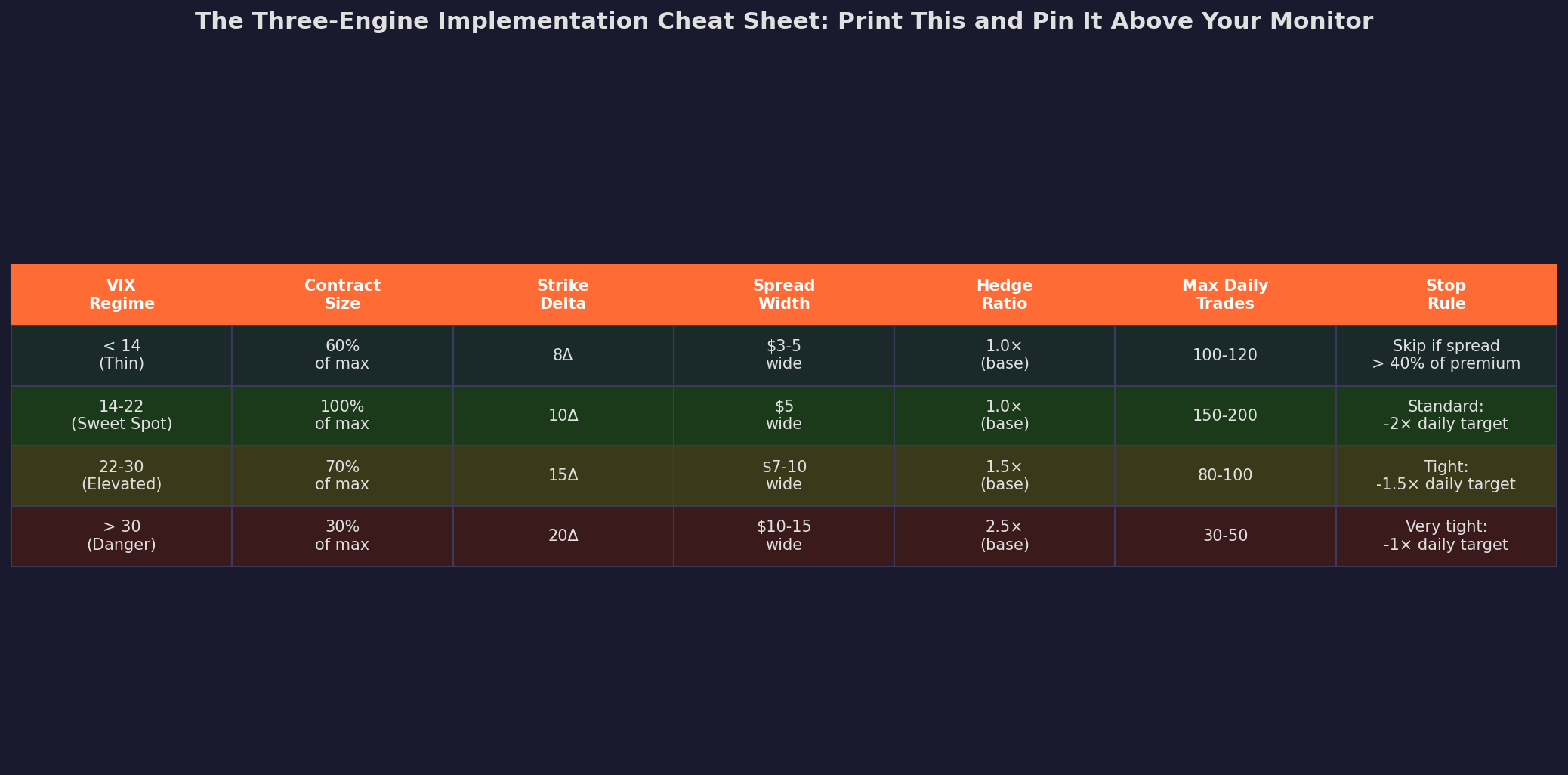

The Cheat Sheet

Print this. Pin it. Don’t trade 0DTE without checking it.

Four zones, seven parameters. Check VIX at open, set your numbers, execute. The stop column is the most important — in the Danger zone, your daily stop is equal to your daily target. One losing day, you’re done for the session. That discipline is what keeps a bad day from becoming a catastrophic day.

The Uncomfortable Truth About 0DTE

The Two-Engine post got 86 subscribers — more than any other post I’ve written. That means a lot of people are interested in selling 0DTE premium. I want to be direct about the risks and caveats.

Even with three engines, 0DTE premium selling requires intraday monitoring, fast execution, deep understanding of gamma risk, and the ability to watch 30+ losing days per year without abandoning the system. The third engine doesn’t make it safe — it makes it less dangerous. Those are different things.

If you’re paper-trading the Two-Engine and it’s working, add the third engine before going live. The regime sizing is the difference between a strategy that survives its first VIX spike and one that doesn’t.

If you’re already live with the Two-Engine, the most important thing you can do today is check your current VIX zone and ask: am I sized correctly for this environment?

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

My math may have errors — please let me know if you find any.

And you should not be doing this unless you understand the risk.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

Great article. However I can't seem to find the PT and stop loss to backtest this myself. Would you mind putting all the vital statistics in one place?

10 Delta put spread, 5pts wide, 100% Stop loss? , 50% PT?

doesn't moving to 15 delta get you closer to spot, less OTM? i must be missing something. great article btw.