Venezuela Crisis Oil Trading Strategy IV: Decision Framework

Part 4: Decision Framework, OPEC+ Scenarios, and the Operational Playbook

This is the PART 4 of a standalone series on the Venezuela Crisis Oil Trading Strategy.

The previous three parts established the thesis (volatility + relative value > directional oil), mapped the sectors (services and refiners win across scenarios), and detailed implementation (option structures and sizing).

This final part provides the operating system: how to update views as information arrives, how OPEC+ decisions shift the entire regime, and a one-page playbook for the next 6-18 months.

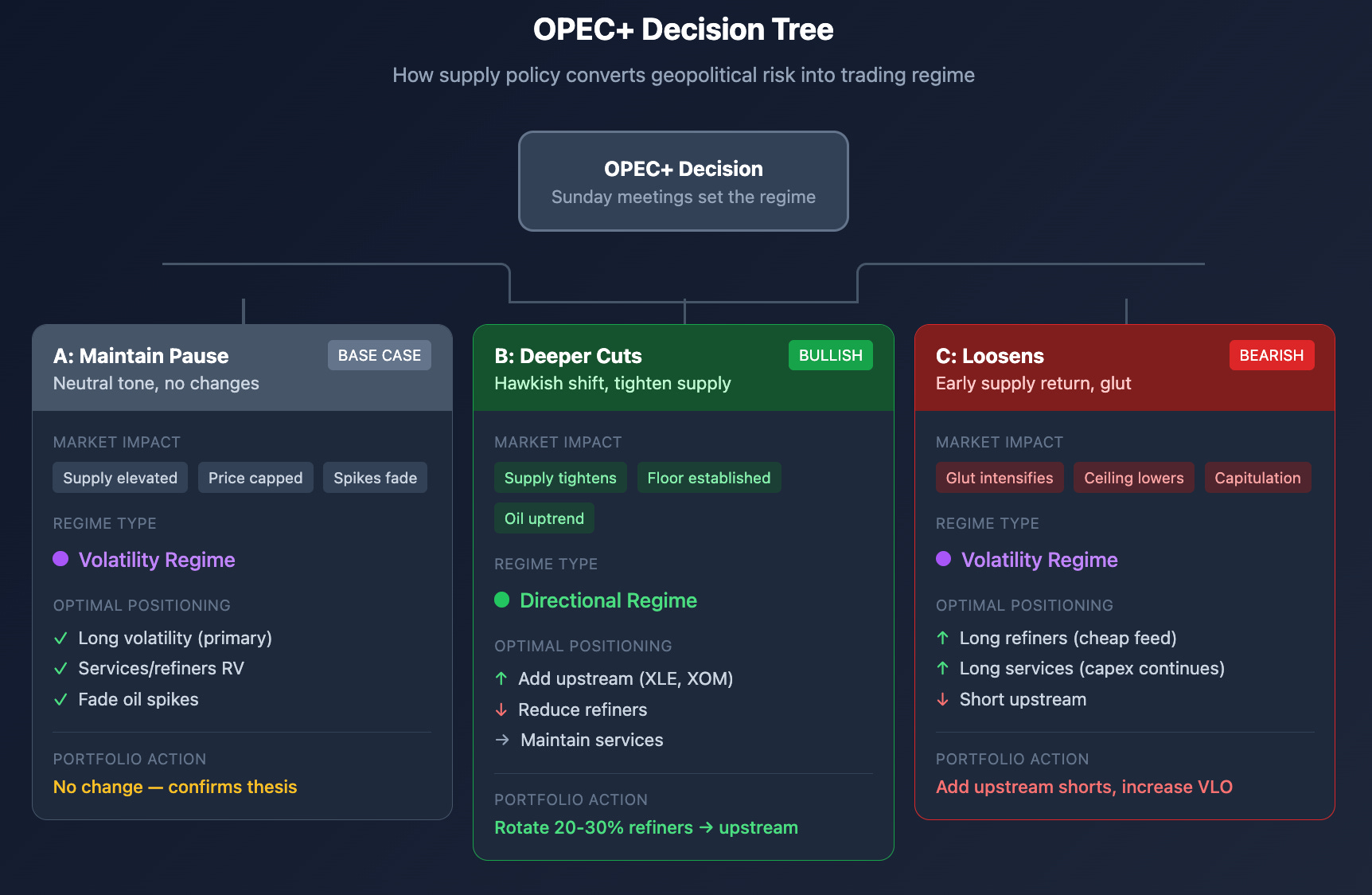

The OPEC+ Decision Tree

OPEC+ is the swing factor that converts geopolitical risk into either:

A volatility regime (if supply stays loose), or

A directional oil regime (if supply tightens)

Their Sunday meeting is expected to confirm a pause on production changes through Q1 2026. But subsequent meetings will be pivotal. Here’s how each outcome changes the trade:

OPEC+ Scenario A: Maintain Pause + Neutral Tone (Base Case)

What it means:

Supply stays elevated

Oil price capped

Spikes fade

Optimal positioning:

Long volatility (primary)

Services/refiners relative value

Fade oil rallies after geopolitical spikes

Portfolio adjustment: None — this confirms base case thesis.

OPEC+ Scenario B: Hawkish Shift / Deeper Cuts

What it means:

Supply tightens

Durable floor established

Potential oil uptrend

Optimal positioning:

Add upstream beta (XLE, XOM, CVX outright)

Reduce refiner overweight (crack spread compression risk)

Maintain services (still benefits from any investment)

Portfolio adjustment:

Rotate 20-30% from refiners to upstream

Convert put spreads on oil to call spreads

Tighten stops on fade trades

OPEC+ Scenario C: Looser Compliance / Early Supply Return

What it means:

Supply glut intensifies

Oil price ceiling lowered

Producer capitulation risk

Optimal positioning:

Long refiners (cheap feedstock + solid margins)

Long services (capex still happens at lower prices)

Short upstream (weak pricing power)

Portfolio adjustment:

Increase refiner allocation

Add explicit upstream shorts

Maintain vol positions (chaos still reprices)

If/Then Decision Triggers

Rather than reacting to every headline, we use specific trigger events that cause material probability shifts. When a trigger fires, we adjust.

Trigger 1: OPEC+ Shifts Toward Deeper Cuts

Signal: Official statement announcing production reductions beyond current commitments, or hawkish surprise from Saudi/UAE leadership.

Probability shift: S7 (OPEC+ tightens) increases from background to primary scenario.

Action:

Increase upstream beta (long CVX/XOM calls)

Reduce refiner overweight by 50%

Convert any short oil calls to long calls

Trigger 2: U.S. Policy Solidifies Around Quarantine/Blockade

Signal: Official designation of oil exports as sanctioned, enforcement actions against buyers, sustained rhetoric against reopening.

Probability shift: S1 (quarantine) becomes dominant; rehabilitation scenarios fade.

Action:

Shrink rebuild exposure (reduce SLB/BKR by 50%)

Emphasize vol + defensive hedges

Short the rebuild basket vs. long volatility

Trigger 3: Contract Reopening + Tenders Begin

Signal: OFAC licenses issued, PDVSA announces international tenders, Chevron announces expansion plans, other majors signal return.

Probability shift: S2/S3 (transition + rehab) probability increases significantly.

Action:

Complete SLB/BKR position build-out

Add second tranche of refiner exposure

Reduce pure volatility positions (vol may compress as uncertainty resolves)

Trigger 4: Sabotage/Export Disruptions Confirmed

Signal: Attacks on oil infrastructure, port blockages, pipeline incidents, production shut-ins.

Probability shift: S4 (sabotage/disruption) moves from 5% to 20%+.

Action:

Remove any short oil calls immediately

Add oil upside via call spreads

Hedge refiner positions (short-term margin compression)

Services still valid but delayed

Trigger 5: China Retaliation Escalates Beyond Rhetoric

Signal: Trade measures specifically targeting U.S. energy sector, military positioning, cyber incidents, shipping interference.

Probability shift: S5 (U.S.-China escalation) increases from background to material.

Action:

Increase volatility and tail hedges

Reduce EM exposure (LATAM especially)

Barbell positioning: energy upside + defense stocks

Avoid concentration in any single scenario bet

Trigger 6: Mining Sector Policy Crystallizes

Signal: Orinoco Mining Arc tenders announced, Chinese mining companies expelled, U.S. critical minerals task force includes Venezuela, any major (Rio Tinto, BHP, Newmont) announces exploration interest.

Probability shift: Minerals angle moves from background optionality to active trade.

Action:

Deploy minerals LEAPS allocation (Structure 8)

Add gold miners (NEM, GDX) if supply disruption narrative

Add MP Materials if rare earth access narrative

Watch for CAT/mining equipment as infrastructure play

Key insight: Minerals signal U.S. commitment to long-term engagement. If minerals policy crystallizes, the Syria/Hybrid scenarios become more likely because the U.S. has strategic reasons to stay committed.

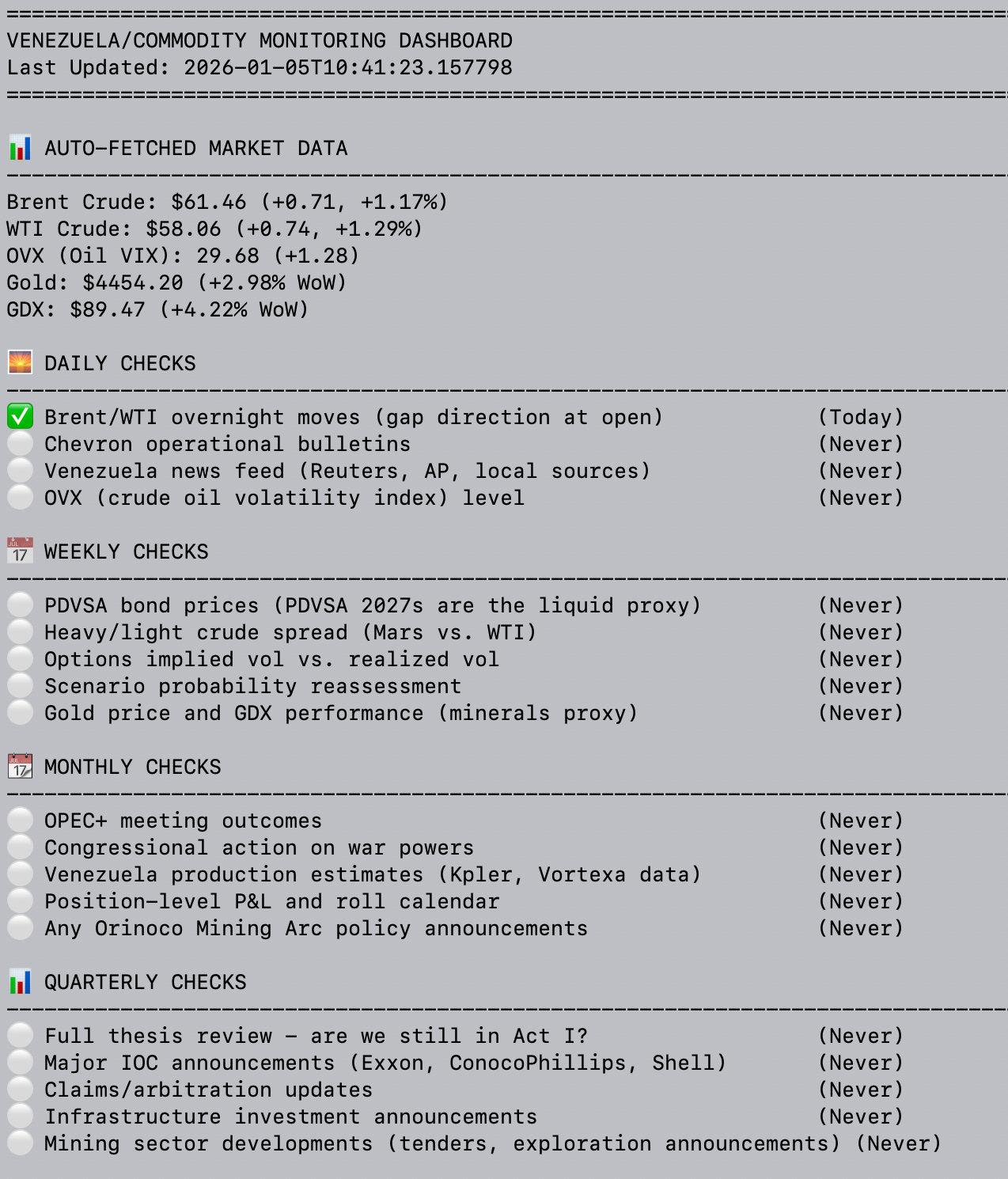

Monitoring Dashboard

Daily Checks

[ ] Brent/WTI overnight moves (gap direction at open)

[ ] Chevron operational bulletins

[ ] Venezuela news feed (Reuters, AP, local sources)

[ ] OVX (crude oil volatility index) level

Weekly Checks

[ ] PDVSA bond prices (PDVSA 2027s are the liquid proxy)

[ ] Heavy/light crude spread (Mars vs. WTI)

[ ] Options implied vol vs. realized vol

[ ] Scenario probability reassessment

[ ] Gold price and GDX performance (minerals proxy)

Monthly Checks

[ ] OPEC+ meeting outcomes

[ ] Congressional action on war powers

[ ] Venezuela production estimates (Kpler, Vortexa data)

[ ] Position-level P&L and roll calendar

[ ] Any Orinoco Mining Arc policy announcements

Quarterly Checks

[ ] Full thesis review - are we still in Act I?

[ ] Major IOC announcements (Exxon, ConocoPhillips, Shell)

[ ] Claims/arbitration updates

[ ] Infrastructure investment announcements

[ ] Mining sector developments (tenders, exploration announcements)

One-Page Operational Playbook

If U.S. Policy = Quarantine/Blockade

→ Long volatility

→ Short rebuild basket

→ Avoid services directional

→ Maintain defensive energy exposure (CVX)

If U.S. Policy = Transition + Tenders

→ Long SLB/BKR vs. short XLE

→ Add VLO/refiners

→ Reduce pure vol allocation

→ Watch for Act II → Act III transition

If Sabotage/Disruption Emerges

→ Long oil calls + long volatility

→ Hedge refiners (short-term margin risk)

→ Close any short oil positions immediately

→ Services valid but delayed—hold, don't add

If OPEC+ Tightens

→ Increase upstream exposure (CVX, XOM calls)

→ Reduce refiner overweight

→ Services still work—maintain

→ Directional long oil becomes viable

If OPEC+ Loosens / Oversupply Persists

→ Long refiners + services

→ Short upstream (E&Ps, majors)

→ Fade oil spikes

→ Vol still elevated—don't abandon

Historical Analogues: What Worked and What Didn’t

Understanding past interventions helps calibrate expectations:

Panama (1989)

Event: U.S. invasion, Noriega captured

Oil impact: +8% spike, fully reverted in 2 weeks

Lesson: Low stakes = low lasting impact

Iraq Invasion (2003)

Event: Major military operation, regime change

Oil impact: +25% run-up, then -30% collapse

Lesson: Market overpriced disruption risk, then corrected

What worked: Fading the spike after initial panic

Libya Civil War (2011)

Event: Gaddafi overthrown, prolonged instability

Oil impact: +20% sustained for 2+ years

Lesson: Light sweet crude disruption is harder to replace

What worked: Sustained long on vol and quality spreads

Venezuela Sanctions (2019)

Event: U.S. sanctions on PDVSA

Oil impact: +5% then fade within 3 months

Lesson: Market already expected disruption; production already declining

What worked: Nothing material—event was priced

Key pattern: Markets typically overprice immediate disruption risk, then underprice prolonged instability. The edge is in timing — not predicting the event, but predicting the fade or the persistence.

The 4 Acts: Where Are We Now?

Final Position Sizing Summary

POSITION SIZING SUMMARY

==============================================================================

Position Allocation Entry Now? Scaling Trigger

------------------------------------------------------------------------------

XLE vol structure 18% Yes Already entered

SLB call spread 15% Yes (50% now) Tenders -> full position

BKR diagonal 10% Yes -

VLO collar 12% After UN meeting OPEC+ clarity

Pairs (SLB vs XLE) 15% Wait Act II confirmed

USO put spread 8% After first spike Spike > $65

COP LEAPS 5% No Settlement mechanism

Mining/REE LEAPS 5% No Mining Arc tenders

Hedge (GLD/macro) 12% Yes - (also minerals proxy)

==============================================================================

Total risk budget: ~6% of portfolio (half-Kelly)

Note: GLD allocation does double duty as escalation hedge AND gold/minerals proxy — but Mohamed A. El-Erian noted that Gold and Oil (as commodities) will likely decouple

Series Conclusion: The Core Thesis

After all of this analysis, the thesis distills to this:

The Venezuela shock is primarily a volatility and relative value opportunity, not a directional oil bet.

Volatility wins in every scenario because policy fog creates repeated repricing events

Services (SLB/BKR) are the highest-torque play because any recovery is a capex story first

Refiners (VLO) offer targeted exposure to heavy crude economics without oil direction risk

Critical minerals are the hidden story - $1.36T in gold, coltan, rare earths explains U.S. strategic commitment

Directional oil is a low-Sharpe trade given the variance across scenarios

The “chess” approach means matching exposures to the current Act, not predicting the finale

The market wants you to bet on headlines. The edge is in betting on structure.

Full Series Index

Part 1: The Event, The Scenarios, and Why This Isn’t About “Oil Up”

Part 3: Implementation - Option Structures, Position Sizing, and Risk Management

Part 4: Decision Framework, OPEC+ Scenarios, and the Operational Playbook (this post)

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

These posts are about methodology, not recommendations. Some of the approaches discussed here involve commodities (like oil) and complex instruments (e.g., options and derivatives) and not suitable for all investors. Many of my analyses probably contain errors — if you find them, please let me know.

While I may hold positions in some of the underlying assets discussed here, my posts are not an endorsement or a recommendation of those underlying assets. This is a quickly emerging and fast-changing situation, so please be wary of information staleness.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

What is the definition of the term "Probability shift"?

Also what is "S7"? (if it is a "scenario" I do not see it listed)