QQQ Is Lying to You

The Tech Schism · Part 1 of 4. The Nasdaq splits a 70% rally and a 17% drawdown down the middle and calls it +15%. The split is structural.

The Nasdaq is up 15% this year. Inside it, $58 billion a quarter is being wired out of software income statements and into Nvidia’s, and the index is hiding the transfer.

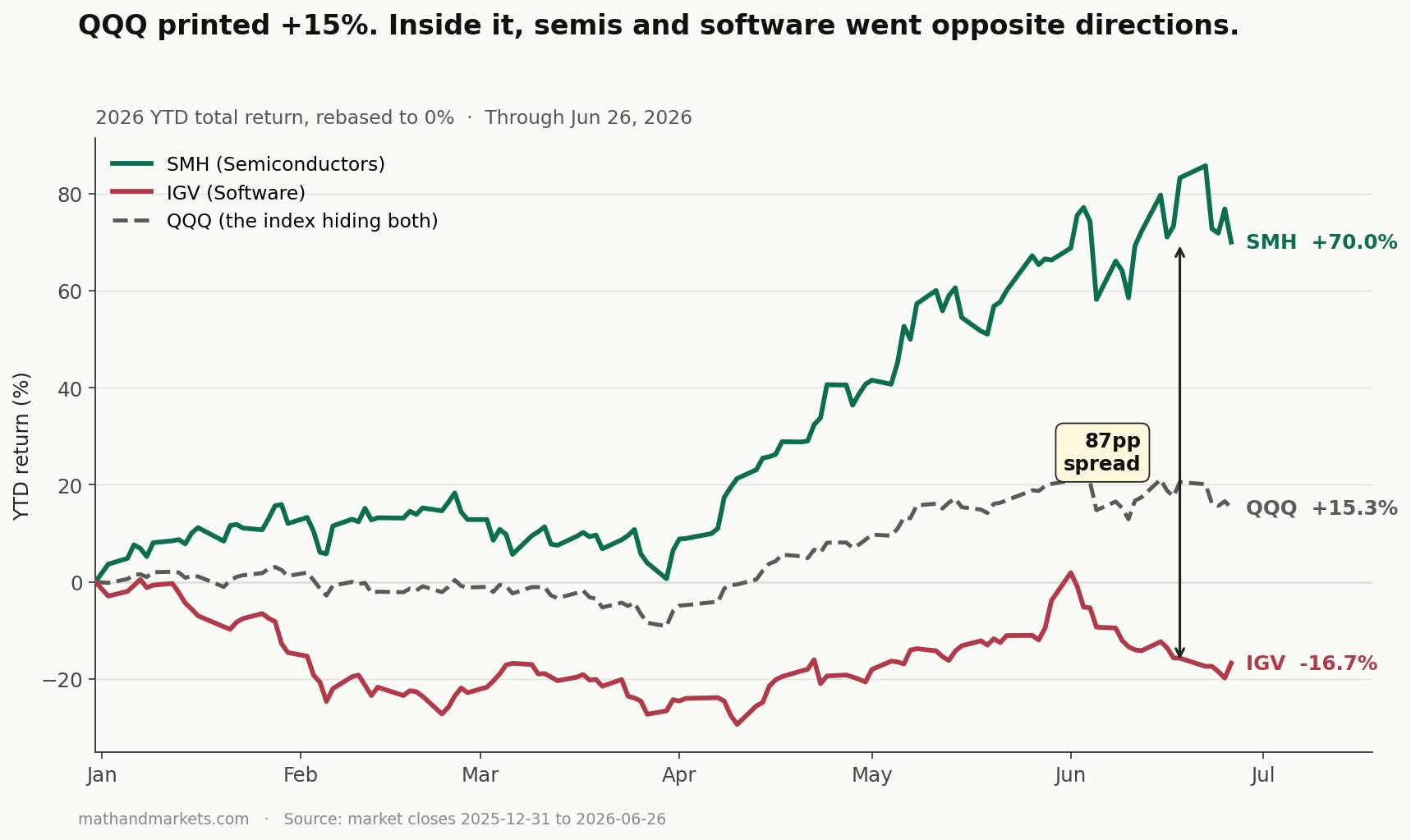

Look at QQQ year-to-date: +15.3%.

If you stopped there, you’d conclude that 2026 has been a perfectly normal year for big tech — maybe a little soft compared to 2024, but nothing broken, nothing screaming. The index is up and the bull is intact, and from that altitude the whole sector looks fine.

Now look inside it.

SMH (semiconductors): +70.0% YTD.

IGV (software): -16.7% YTD.

That’s an 86.7 percentage-point spread between two sectors that, eighteen months ago, were considered the same trade — both filed under “tech,” both living in QQQ, both showing up in the same long-only growth funds, momentum screens, and “AI beneficiary” baskets. They are not the same trade anymore, and they are not even moving in the same directionanymore. And QQQ — the instrument that millions of people use as their proxy for “tech” — is hiding it.

The arithmetic of a lie

QQQ is a market-cap-weighted index. When one component rips 70% and another bleeds 17%, the index doesn’t show you the fracture — it shows you the weighted average of the boom and the bust, and reports a polite, unremarkable +15.3%. This is not a metaphor for what’s happening, it’s the literal mechanism: the index is mathematically designed to smooth over exactly the kind of internal civil war that is happening right now inside it.

And the civil war has a name: AI capex is a margin transfer. Every incremental dollar Microsoft, Meta, Amazon, and Google spend on Nvidia GPUs is a dollar that used to live as software operating margin and now lives as silicon revenue. Software isn’t losing to “the AI story” — software is the AI story, just on the wrong end of the income statement. I’ll prove the capex side of that claim in a minute. Hold that thought.

The Mag-7 is no longer one trade

Look at the chart above. SMH and IGV started the year at the same point, the gap reached 30 points by April, widened to 75 by June, and sits at 87 today. The QQQ line — the grey dashed one — sits between them like a man trying to look casual at a knife fight.

A careful reader is going to ask the obvious question: if MSFT is down 36% from highs and META is down 32% and AAPL is down 13%, how is QQQ only up 15%? The answer is the cleanest possible proof of the bifurcation: QQQ is being held up almost single-handedly by NVDA and the semiconductor weight inside it, while the software-adjacent Mag-7 names get beaten down. The index isn’t lying about the average — it’s hiding that the average is the difference between two violent moves in opposite directions.

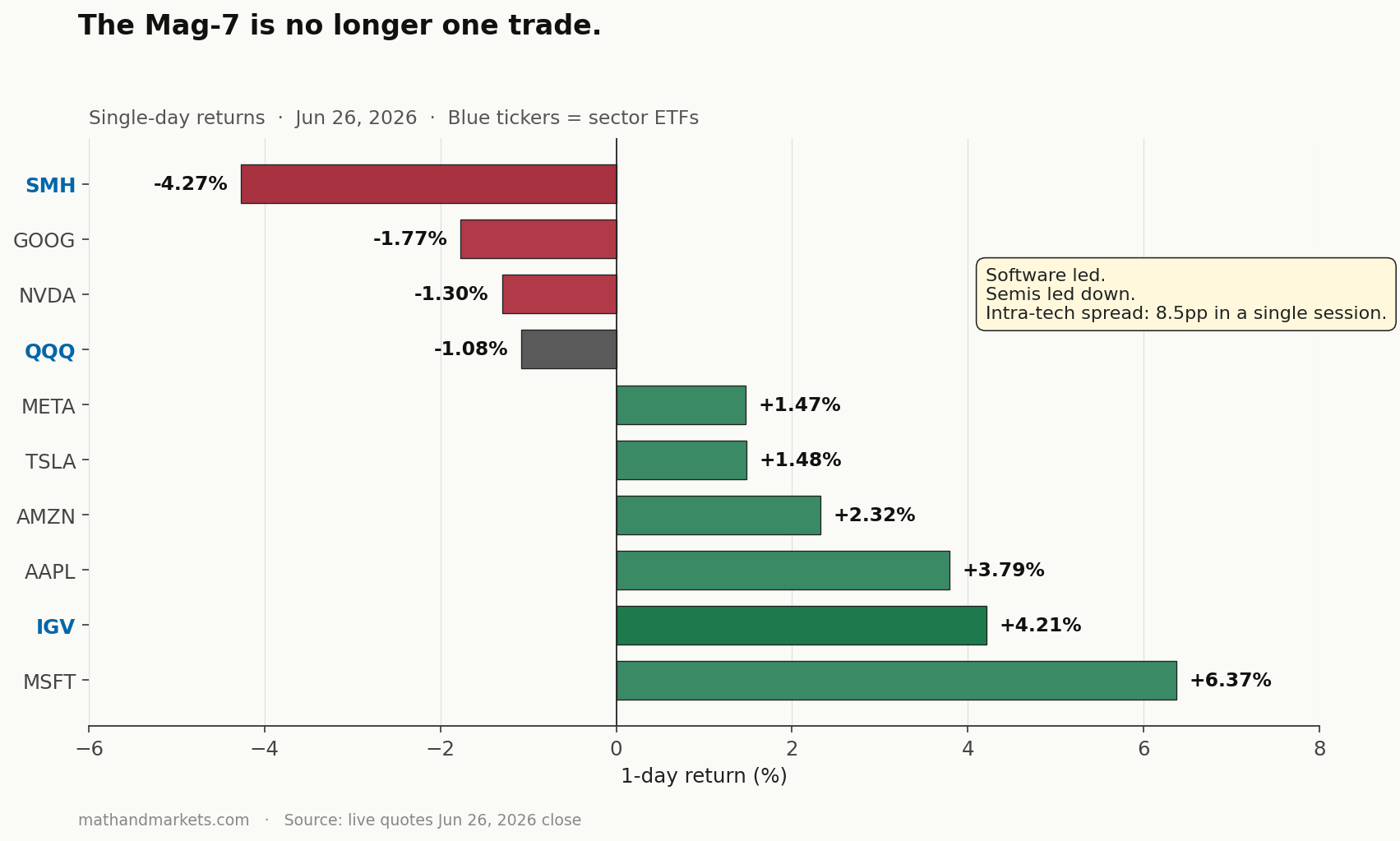

Friday’s tape made this concrete in a single session.

On Friday, software ripped and semis sold off — the opposite of the YTD trend:

MSFT: +6.37% · IGV: +4.21% · AAPL: +3.79%

SMH: -4.27% · NVDA: -1.30% · GOOG: -1.77%

QQQ closed -1.08% — down a single percent on a day where one of its components was +6.4% and another was -4.3%. Whether the schism is widening or briefly closing, the volatility is happening inside the index rather than to it, and that is the actual signal. Friday’s tape is not a refutation of the thesis; it is the thesis in miniature. Tech is no longer one trade, and now it’s not even one direction.

“But this will mean-revert”

The natural counter-argument is that this is a rubber band — software is too cheap, semis are too expensive, and mean reversion will eventually save the IGV longs. Friday’s rip in MSFT and IGV will fuel that argument hard over the next few weeks.

Mean reversion works when both sides of a spread are pricing the same flow and sentiment briefly gets out of sync, the way two correlated stocks oscillate around a pair ratio. It does not work when the spread is the visible artifact of a one-directional, contractually-committed capital flow — and that’s what this is. Look at the dollars.

Hyperscaler capex, this quarter vs one year ago:

MSFT: $16.7B → $30.9B (+84% YoY)

AMZN: $25.0B → $44.2B (+77% YoY)

META: $12.9B → $19.0B (+47% YoY)

GOOG: $17.2B → $35.7B (+107% YoY)

Big Four total: $71.9B → $129.8B per quarter, an additional $57.8B per quarter flowing into capex versus a year ago.

That is roughly the entire quarterly revenue of Salesforce, ServiceNow, Adobe, and Workday combined — being committed to capex every three months in incremental dollars alone, and most of it going to one place: silicon.

Capex of this size doesn’t oscillate. It is announced on earnings calls a year in advance, contracted with TSMC and Nvidia two years in advance, and built into power-purchase agreements three years in advance, with most of the spend already obligated by the time you read the press release. The hyperscalers can’t quietly walk it back without a guidance reset that crushes their own stocks. In the literal sense, the capital flow is locked in — the dollars going into silicon next quarter are already on order, and the dollars coming out of software margins to fund them are already on the budget. Mean reversion requires the flow to reverse, and the flow can’t reverse, because it’s signed.

Priced-in or observed?

Now here’s the honest part of this post, the part that makes me less certain than the rest.

Software margins haven’t actually compressed yet — not in most names. MSFT’s gross margin is essentially flat year-over-year (68.7% → 67.6%), Adobe is flat, Salesforce is flat. The one large software name that is showing real gross margin compression is **ServiceNow, down from 78.9% to 75.1% — nearly four full points of margin in a single year, which is enormous — but it is only one name.

So the bear case against the IGV trade is straightforward: this is anticipated deterioration, not observed deterioration.The market is pricing in margin compression that hasn’t fully arrived in the reported financials, which makes it at least possible that the market is wrong and the rubber band snaps back when next quarter’s software earnings come in fine.

I don’t think that’s what happens, but I want to lay out why honestly. The capex is being spent right now, every quarter, in real dollars; depreciation on $130 billion per quarter of GPU and datacenter capex is going to start hitting income statements as those assets get placed in service, and that is not a forecast but an accounting identity. Once it hits, gross margins compress mechanically rather than at management’s discretion. But that sequence — capex first, depreciation second, margin compression third — is still a thesis, not a fact. The fact is the capex; the thesis is what the capex will eventually do to software margins. If you’re going to short IGV on the back of this, you should know which is which.

Who is getting hurt

The people getting hurt by the QQQ lie are not the index investors — the index is doing exactly what it was designed to do, which is to average things. The people getting hurt are the active managers, the long-only growth funds, the “AI thematic” ETFs, and the retail investors who own software names because they believed in the AI story, and they are getting hurt because every dollar the AI story raised in capital, attention, and capex went into the silicon side of the trade and is being extracted out of the software side.

If you own IGV — or if you own a basket of “AI software” names because somebody told you AI would expand software TAM — you have been on the wrong side of the largest sector rotation in modern tech history, and your QQQ benchmark has been quietly telling you that you’re “only a little behind.” You are not a little behind; you are catastrophically behind, and the index is camouflaging the magnitude of your underperformance. Friday’s rip in MSFT and IGV may have closed the gap by a couple of points, but it does not close 87.

This is the most dangerous kind of bear market: the one that doesn’t look like a bear market on the chart everyone is watching.

What to do with this post

If you take one thing from this piece, take this: stop using QQQ as your proxy for “tech.” It hasn’t been a single sector for at least six months — it is two sectors stapled together, moving in opposite directions, and the index is hiding the divergence from you.

If you are long “tech” and underperforming, the question isn’t whether you’re right or wrong but which half of QQQ you actually own. If it’s the silicon half, you’re winning and you don’t know it. If it’s the software half, you’re losing and your benchmark is lying to you about how badly. So pull up your portfolio, look at the tech sleeve, and ask which half of the schism it lives on. The answer matters more than your YTD number.

Next Saturday: “Software Is Dead. Long Live Silicon.” A closer look at the margin transfer — when the depreciation actually hits, which names get crushed first, and why the coal-to-natural-gas analogy is more literal than you think.

If this reframed how you look at your tech book, restack it. Someone in your feed is benchmarking themselves to QQQ tonight and doesn’t know what it’s hiding.

As always, the material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

Alpha is never guaranteed and the backtest is a liar until proven otherwise.

What to do now if already missed the AI growth run? Chase at these levels or keep buying QQQ?

Good article by the way