Four 0DTE SPX Trades I’d Make With $25K (And Two I Wouldn’t Touch)

Specific setups, exact dollar amounts, position sizing math, and the two popular trades that will blow up a small account

This is part 100 of my series — Building & Scaling Algorithmic Trading Strategies

The Trades

Every other week there’s a variation of this on various Reddit trading subs: “I have $25K. What 0DTE trades should I actually be making?”

Not “it depends on your risk tolerance.” Not “paper trade first.” The actual trades. Strikes, dollars, what you’re risking, what you’re making.

Well, here are the four I’d run — with SPX at 7,400 — and what each one looks like at expiry.

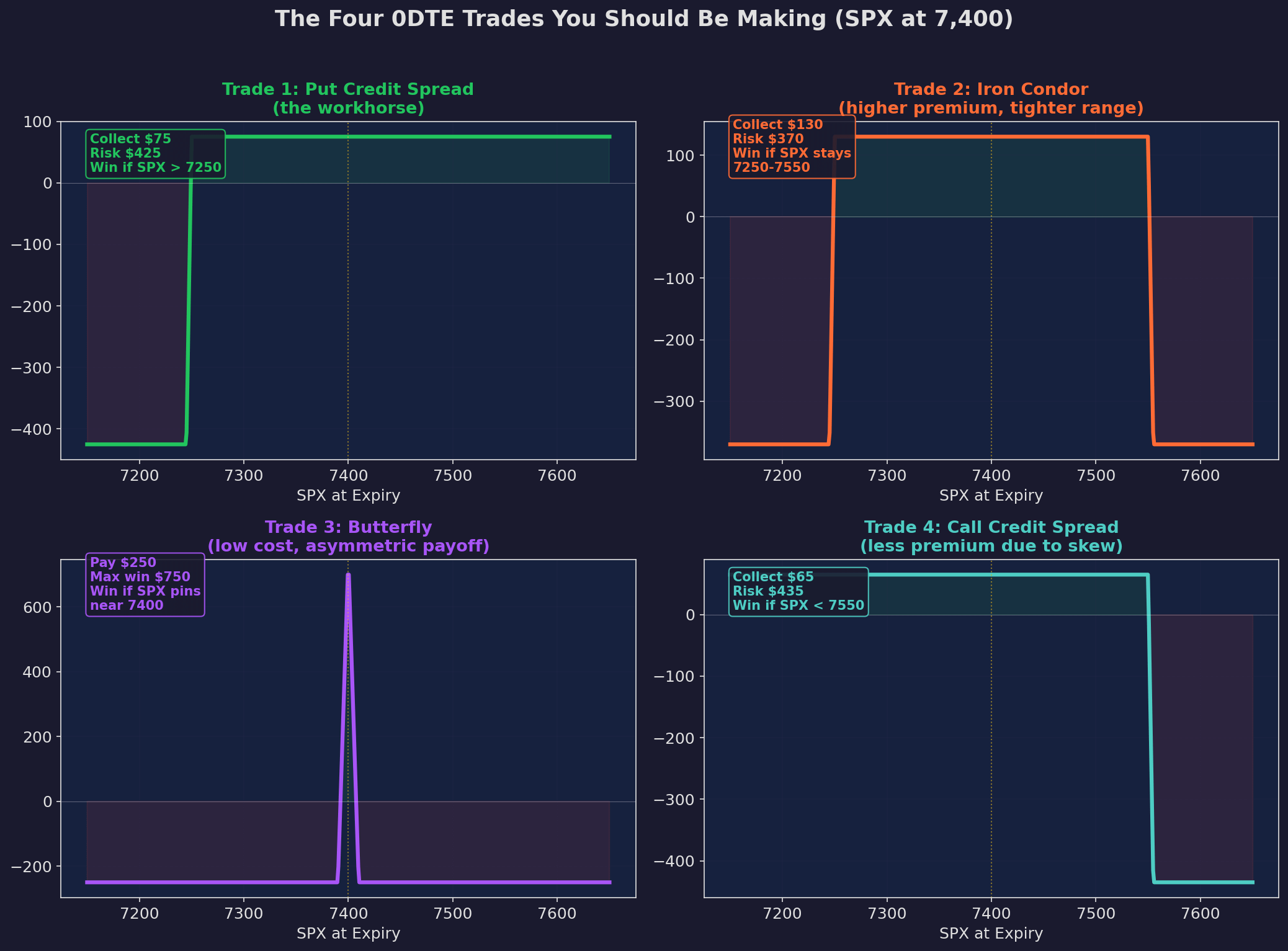

Four trades, four payoff profiles. Top left: the put credit spread — your daily workhorse, collect $75, risk $425, win if SPX stays above 7,250. Top right: the iron condor — higher premium ($130), tighter range (7,250-7,550), win if SPX goes nowhere. Bottom left: the butterfly — only $250 at risk, but if SPX pins near 7,400 you make $750. Bottom right: the call credit spread — same structure as the put spread but on the upside, slightly less premium because of skew.

Trade 1: The Put Credit Spread

This is the one you do every day. The one that compounds your account while you’re eating lunch.

10:30am. Not at open — the bid-ask spread at 9:30 is 30-50% wider than it will be an hour later. You’re paying $20-40 in invisible friction for the privilege of being early. Just wait.

Sell the 10-delta put. With SPX at 7,400 and VIX at 18, that’s roughly the 7,250 strike — about 1.5% below spot. Buy the put $5 below it (7,245). Collect $0.65-0.85 in premium per spread.

You just bet that SPX won’t fall 1.5% by 4pm. Historically, SPX stays above its 10-delta put about 72% of the time. On the 72% of days you’re right, you keep $65-85. On the 28% you’re wrong, you lose $425-435.

Expected value per spread: roughly +$5. Not exciting per trade. But 3 spreads a day, 252 days a year — that’s the math behind a 19% annual return on a $25K account. We’ll get to the growth path.

When to skip: VIX below 14 (premium is $0.15 — not worth the execution cost) or VIX above 25 (widen to 15-delta strikes per the Three-Engine framework).

Trade 2: The Iron Condor

Same concept, both sides. You’re selling the put credit spread AND a call credit spread. Betting SPX stays in a box.

Sell the 10-delta put spread (7,250/7,245) AND the 10-delta call spread (7,550/7,555). Collect $1.10-1.40 combined.

More premium than a standalone spread — $130 vs. $75. But the win rate drops to about 65% because the market only needs to break ONE side to hurt you. On big directional days, you give back the extra premium and then some.

Use it when: You have zero directional view and VIX is in the 16-22 sweet spot. This is a pure vol trade — you’re selling the market’s expectation of movement.

Don’t use it when: There’s a Fed meeting, CPI print, or any catalyst that could send SPX 1%+ in either direction. On catalyst days, sell one side — the side you think won’t get hit.

Trade 3: The Butterfly

This is the underrated one. The trade nobody on Reddit talks about because the win rate is ugly — roughly 30%. But the risk/reward is inverted.

Buy the 7,390 call. Sell two 7,400 calls. Buy the 7,410 call. Cost: $2.00-3.00 per fly ($200-300).

If SPX closes anywhere near 7,400, you make $400-750. If it doesn’t, you lose your $250. That’s it.

The math doesn’t work on any single day. It works across 30 days. You put on 3-4 butterflies a day at $250 each, risk $750-1,000 (3-4% of account), and the 30% that hit near the center strike cover the 70% that don’t.

The secret: Low-VIX days when the market is grinding sideways. SPX tends to pin near round numbers and heavy open interest strikes on quiet days. The butterfly is a pinning bet — and on days when the market cooperates, the payoff is 3:1.

Why it’s perfect for small accounts: $250 at risk. Not $500. You can take four shots per day and your worst-case daily loss is $1,000. Compare that to the iron condor where one bad day costs $500.

Trade 4: The Call Credit Spread

Mirror image of Trade 1, on the upside.

Sell the 10-delta call (~6000 strike) and buy the call $5 above it. Collect $0.55-0.75.

Less premium than the put spread. Always. That’s skew — the market charges more for downside protection than upside protection because crashes happen more violently than rallies. At the same 10-delta, the put is always more expensive than the call.

Use it when: You’re bearish or neutral. After a large rally (SPX rarely does back-to-back 1%+ up days). Or to balance a put credit spread into a piecemeal iron condor — sell the put spread in the morning, add the call spread after lunch if the market’s been flat.

Two Trades That Will Blow Up Your Account

People run these on $25K accounts all the time. They shouldn’t.

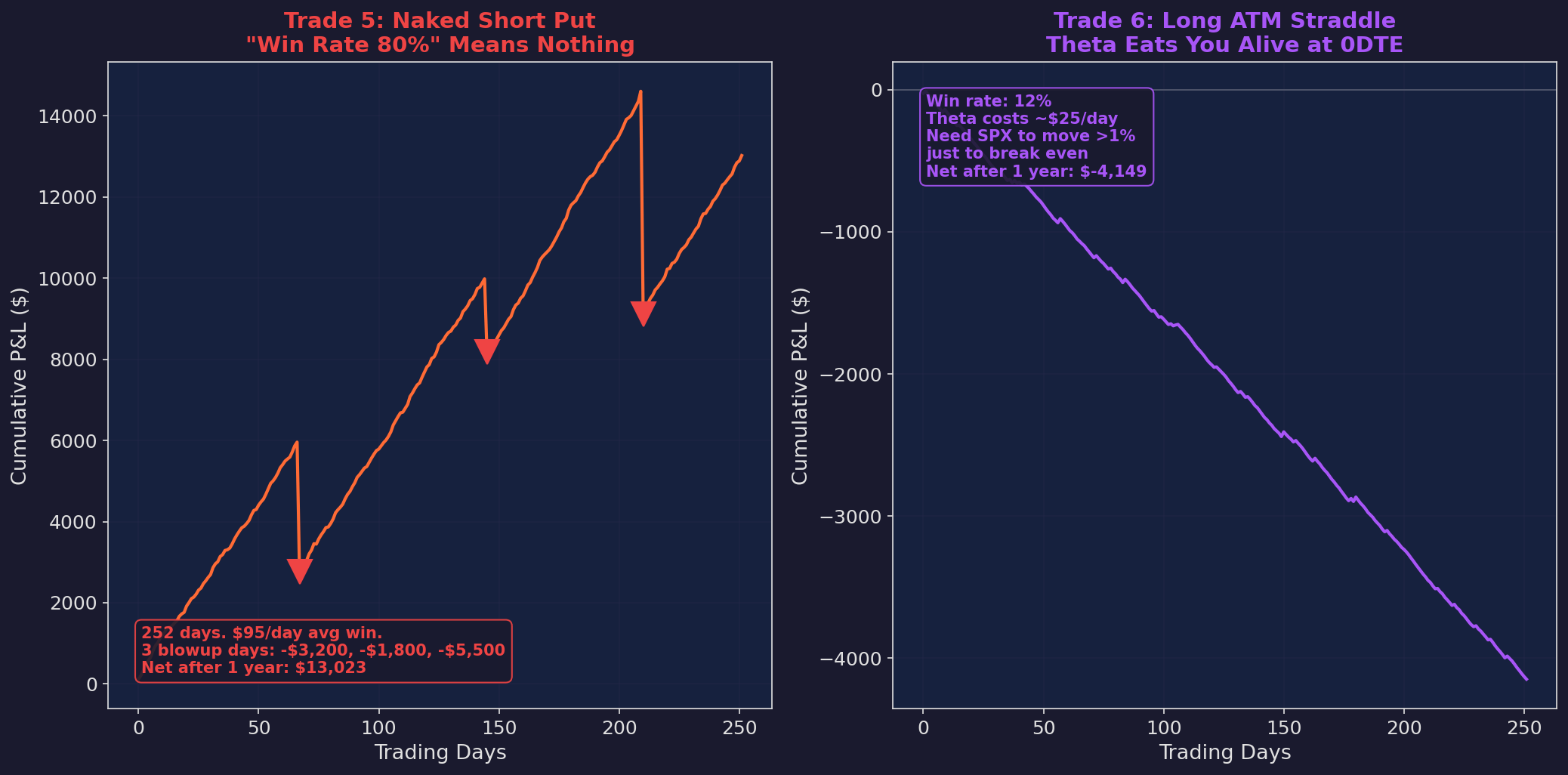

Trade 5: The Naked Short Put

“But the win rate is 80%!”

Look at the left panel. A naked put averages $95 per day. Beautiful equity curve going up and to the right — until it isn’t. Three blowup days: -$3,200, -$1,800, -$5,500. That $5,500 loss is 22% of a $25K account in a single session.

And that’s a good outcome. The naked put has no defined maximum loss. A flash crash, a gap down, an August 5th VIX spike — your $25K account could go negative. Not to zero. Negative. You can owe your broker money.

The margin requirement alone is disqualifying: $5,000+ for a single naked SPX put. That’s 20% of your account on one position with unlimited downside.

If you want to sell puts, sell put spreads. The $5-wide spread costs you $10 in premium but caps your loss at $500. That cap is what lets you trade every day and still be here next month.

Trade 6: The Long ATM Straddle

This is the “something big is about to happen” trade. At 0DTE, it’s a theta incinerator.

An ATM straddle costs $20-30 at 0DTE. SPX needs to move 0.5%+ AFTER you enter just to break even. On most days, SPX’s total daily range is less than 0.5%.

Right panel: 12% win rate. Steady bleed of $25/day. After a year: -$4,149. The straddle works at 30 DTE where theta is gentle and you have time for a move to develop. At 0DTE, theta is a chainsaw. It cuts through your position minute by minute, and unless SPX makes a violent intraday move, you’re paying premium to watch your trade decay to zero.

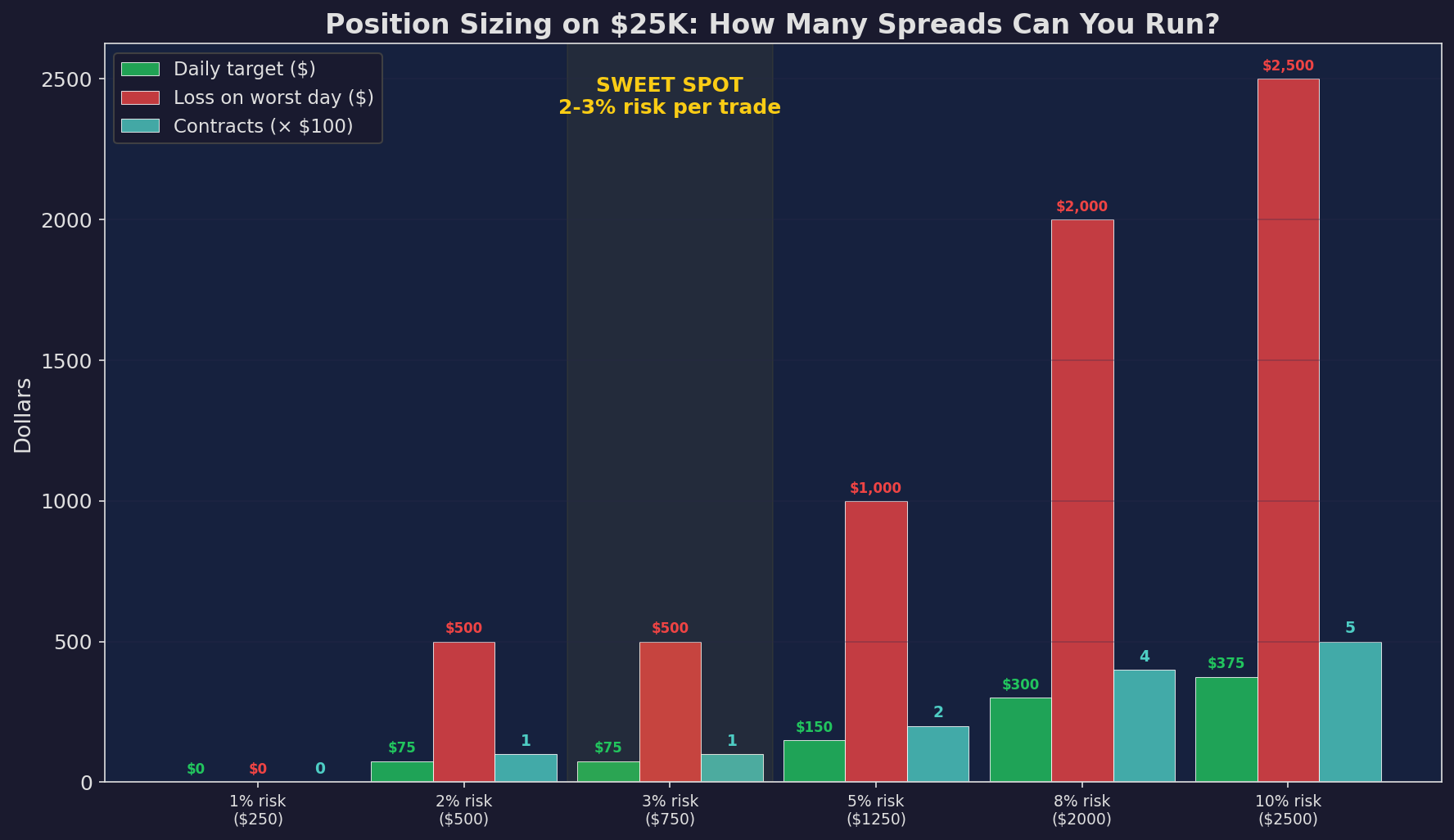

How Many Spreads Can You Actually Run?

At 2% risk per trade ($500), you run 1 spread per entry. At 3% risk ($750), still 1 spread but with room for wider wings. The sweet spot is 2-3%. At 5%+ you’re one bad streak from a blown account.

The rule that keeps you alive: max 2-3% of your account per trade. On $25K, that’s $500-750 at risk per entry.

A $5-wide SPX spread has a $500 max loss. So you run one spread per entry. Three entries across the day (10:30, 12:30, 2:30) = three spreads, $1,500 max daily risk, 6% of account.

“One spread? That only makes $75!” Yes. Three of them make $225 on a good day. That’s $1,125 per good week. The compounding does the rest.

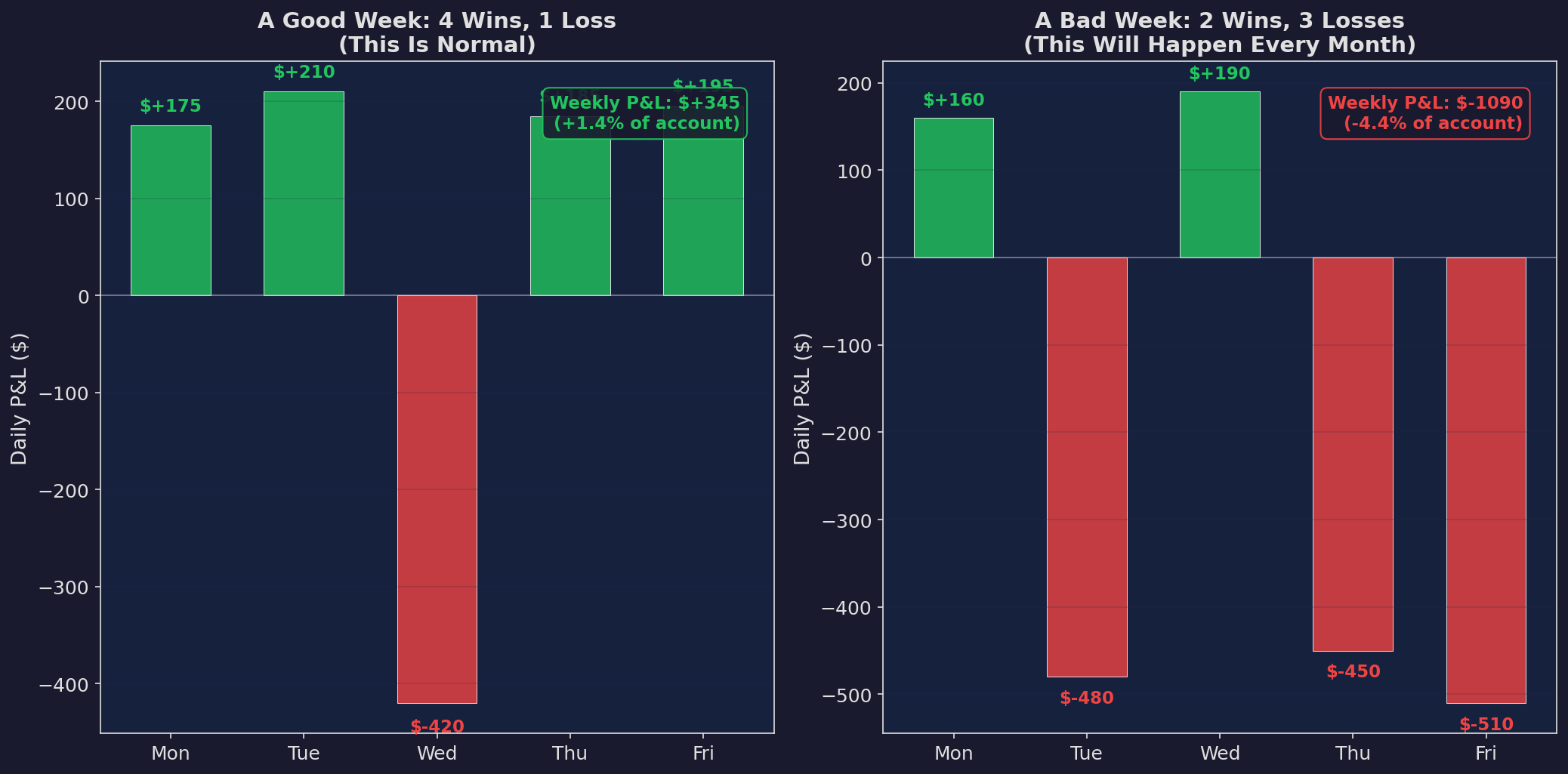

What a Real Week Looks Like

This is the part nobody posts on social media.

Left: four wins, one loss, net +$345 (+1.4%). This is a good week. Right: two wins, three losses, net -$1,090 (-4.4%). This is a bad week. Both happen regularly. The bad week will happen roughly once a month.

The bad week is the test. Not whether the strategy works — the math says it does. Whether you can sit through three losing days in a row without changing your approach, increasing your size, or abandoning the system entirely.

If looking at -$1,090 on a Friday makes you want to double your contracts on Monday, this isn’t for you. The strategy needs 200+ trades to express its edge. You need to let it.

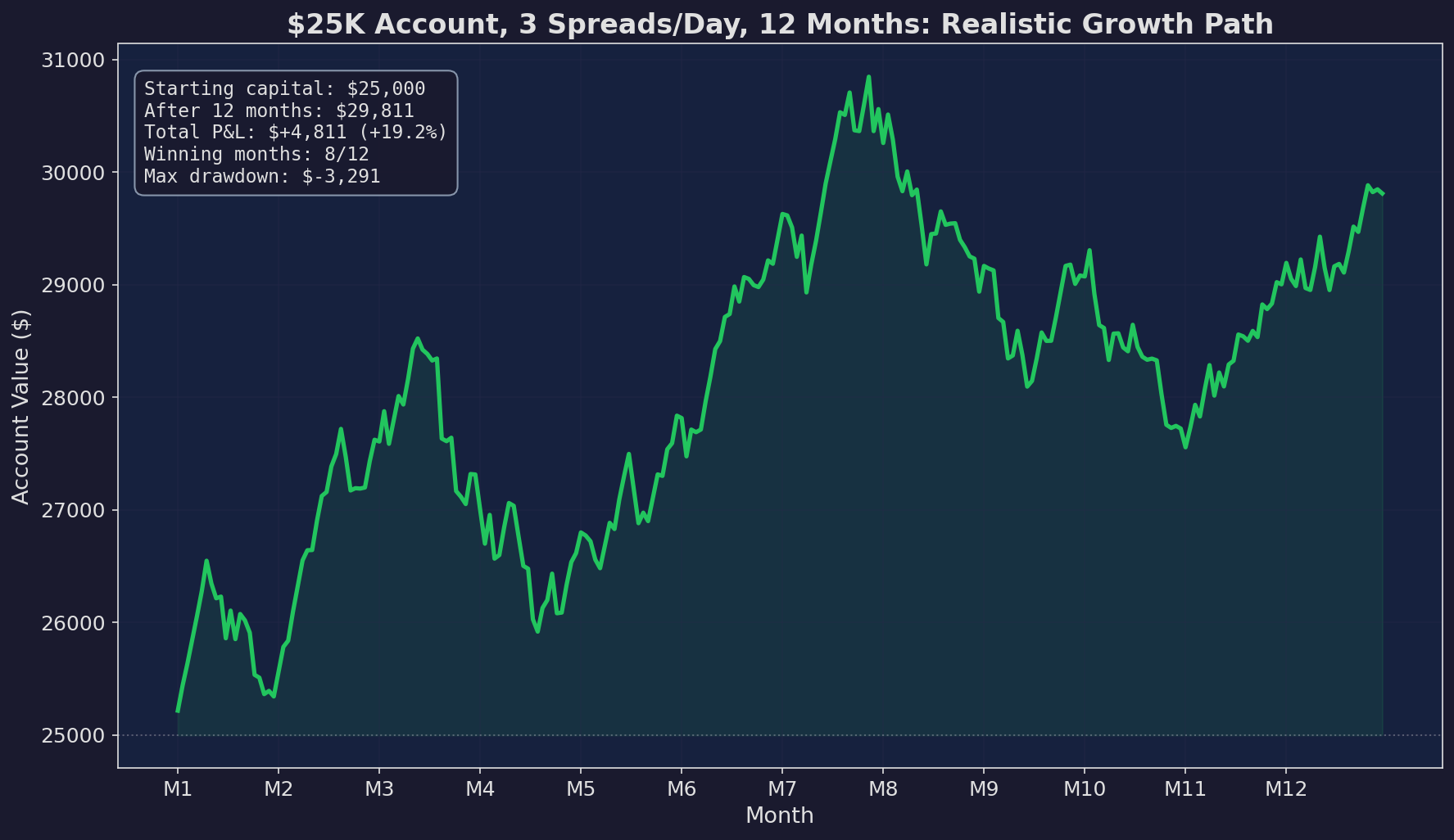

The 12-Month Reality Check

$25K to $29,811 in 12 months. +19.2%. Eight winning months out of twelve. Max drawdown $3,291. This is what “realistic” looks like.

Nobody’s screenshotting +19% for Reddit. There’s no 10-bagger, no “turned $500 into $50K” story. Just a $25K account that grew to almost $30K through 756 small trades, each one risking $500 to make $75.

Year 2 at the same rate on $30K: $5,700 in profit. Year 3: $6,800. By year 5 you’re north of $50K and running 5-6 spreads per day.

The path to $1.5M isn’t one trade. It’s 3,000 of them.

Five Rules, Non-Negotiable

1. Max 2% of account per trade. Survive losing streaks. Five losses in a row = -10%, not -50%. Break it and you blow up on the first bad week.

2. No trades in the first 15 minutes. Spreads are widest at open — you pay 30-50% more in friction. Death by a thousand cuts.

3. Close at 50% profit or let expire. Taking profits at 50% frees capital and avoids late-day gamma spikes. Otherwise you hold a winner that reverses at 3:30pm and goes from +$60 to -$400.

4. Daily stop: 2× your target. One bad day should cost two good days, not ten. A VIX spike catches you at full size and you lose a month of premium.

5. Check VIX before your first trade. VIX > 25 = widen strikes, reduce size. Sell 10-delta into VIX 30 without adjusting and wonder why your “safe” spread lost $500.

The hardest one for me is the daily stop. Two losing trades by 1pm and every instinct screams “one more to get back to even.” That’s how a $500 loss becomes a $1,500 loss. The stop exists for the days when your judgment is worst — which are always the days you’re losing.

I don’t care who you are — all of us are human, and it’s important to have a degree of self awareness.

The VIX Check

Before your first trade, check VIX. Every day. If you’ve read the Three-Engine 0DTE post, you know the full framework. The short version:

VIX < 14: Run 1-2 spreads instead of 3. Premium is thin. Don’t force it.

VIX 14-22: Full speed. This is your money zone.

VIX 22-30: Widen to 15-delta. Run 2 spreads. Tighten stops.

VIX > 30: One spread max, or sit out entirely. The best 0DTE trade on a VIX-35 day is no trade at all.

Where to Start

If this is your first 0DTE post:

Two-Engine 0DTE — the original framework

Three-Engine 0DTE — adding VIX regime sizing

This post — the specific trades for a $25K account

Paper trade for two weeks. Track every entry, every exit, every P&L. Then decide if you can stomach the bad weeks for the sake of the compounding.

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

Hey there - help me out with the math on trade 1 :

“On the 72% of days you’re right, you keep $65-85. On the 28% you’re wrong, you lose $425-435.”

Winning 1 unit 3 days then losing 6 units on the 4th day is a *heavily* negative EV proposition. What am I missing here?

wow, great content!