Why Buy-and-Hold Outperformed Every Options Strategy (2020–2025): A Technical and Mathematical Analysis

Part 37 evaluates why several options strategies don't work in the current SPY/SPX regime

This is part 37 of my series — Building & Scaling Algorithmic Trading Strategies

SPY/SPX Backtests (November 2020 - November 2025)

Backtests on SPY and SPX from 11/27/2020 to 11/26/2025 show the same surprising-but-not-surprising outcome:

Buy-and-Hold outperformed short iron condors, long iron condors, short strangles, and long strangles — by a wide margin, in every case.

Below is a comprehensive mathematical breakdown of why — and what it means for options strategies in this current market regime.

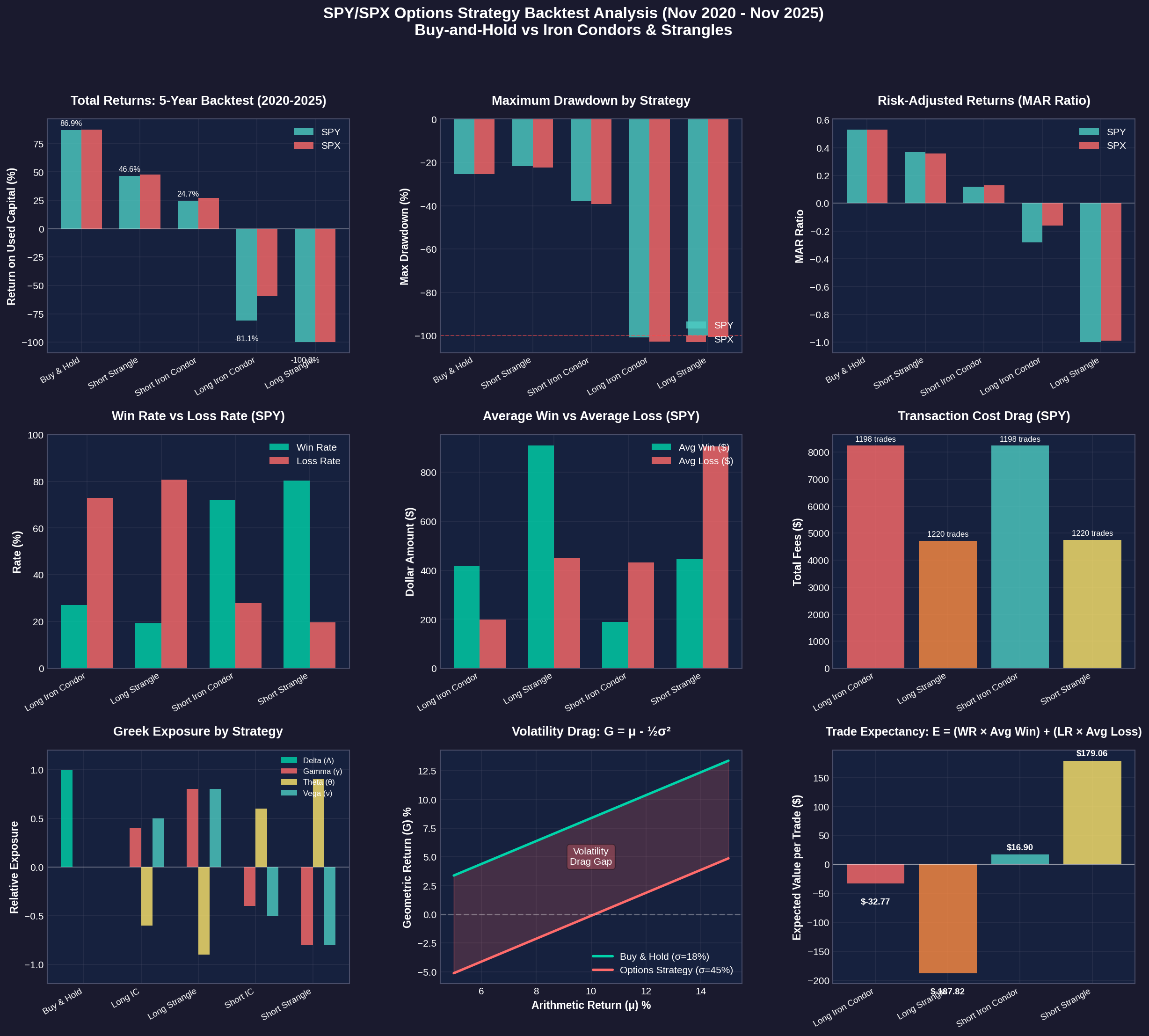

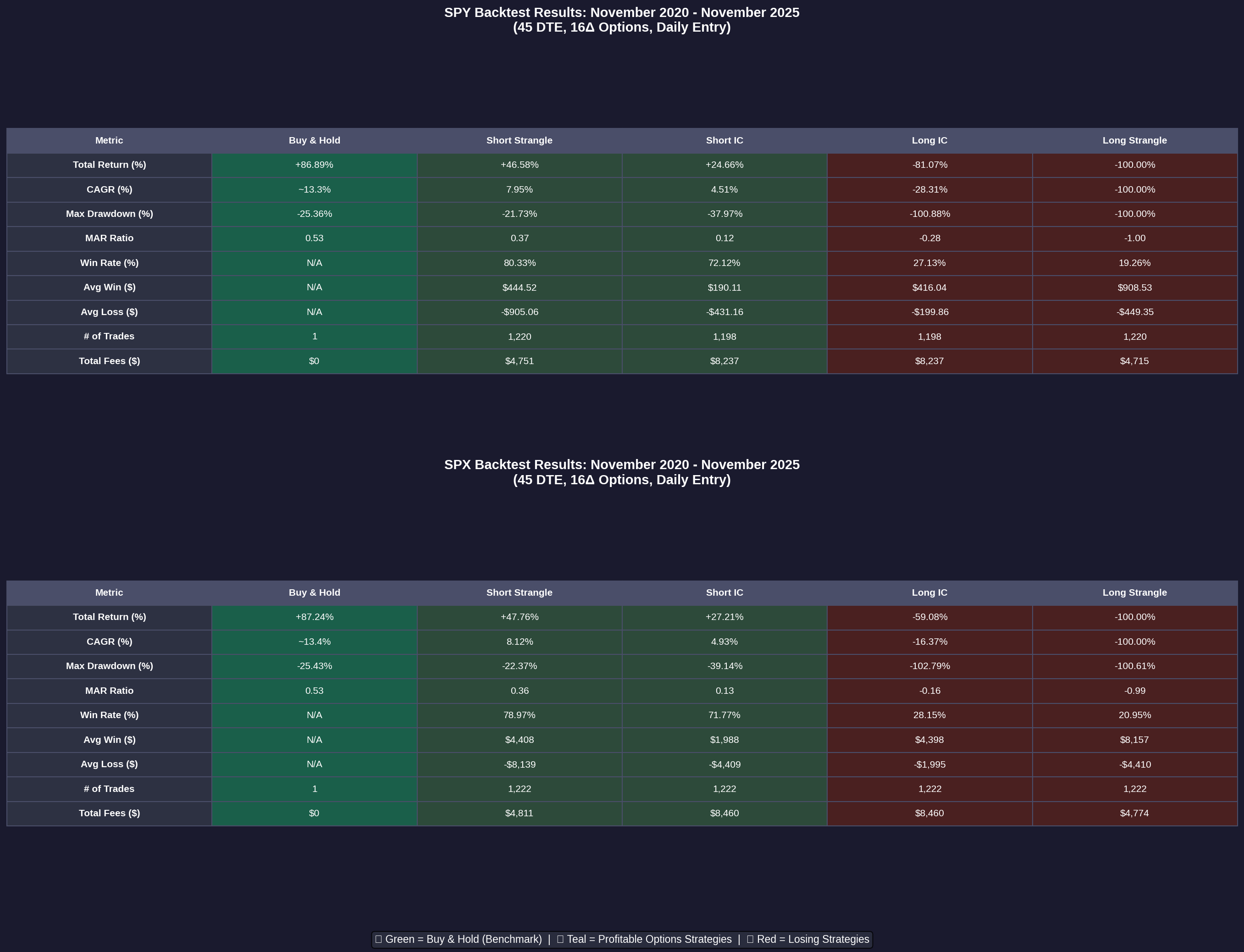

1. Executive Summary: The Numbers

SPY Results (5-Year Backtest)

Strategy Return Max DD CAGR Win Rate MAR

─────────────────────────────────────────────────────────────────────

Buy & Hold +86.89% -25.36% ~13.3% N/A 0.53

Short Strangle +46.58% -21.73% 7.95% 80.33% 0.37

Short Iron Condor +24.66% -37.97% 4.51% 72.12% 0.12

Long Iron Condor -81.07% -100.88% -28.31% 27.13% -0.28

Long Strangle -100.00% -100.00% -100.00% 19.26% -1.00SPX Results (5-Year Backtest)

Strategy Return Max DD CAGR Win Rate MAR

─────────────────────────────────────────────────────────────────────

Buy & Hold +87.24% -25.43% ~13.4% N/A 0.53

Short Strangle +47.76% -22.37% 8.12% 78.97% 0.36

Short Iron Condor +27.21% -39.14% 4.93% 71.77% 0.13

Long Iron Condor -59.08% -102.79% -16.37% 28.15% -0.16

Long Strangle -100.00% -100.61% -100.00% 20.95% -0.99Key Observation: SPX and SPY results are remarkably consistent, confirming these findings aren’t a quirk of one instrument. Buy-and-Hold outperformed every options strategy by 40-187 percentage points.

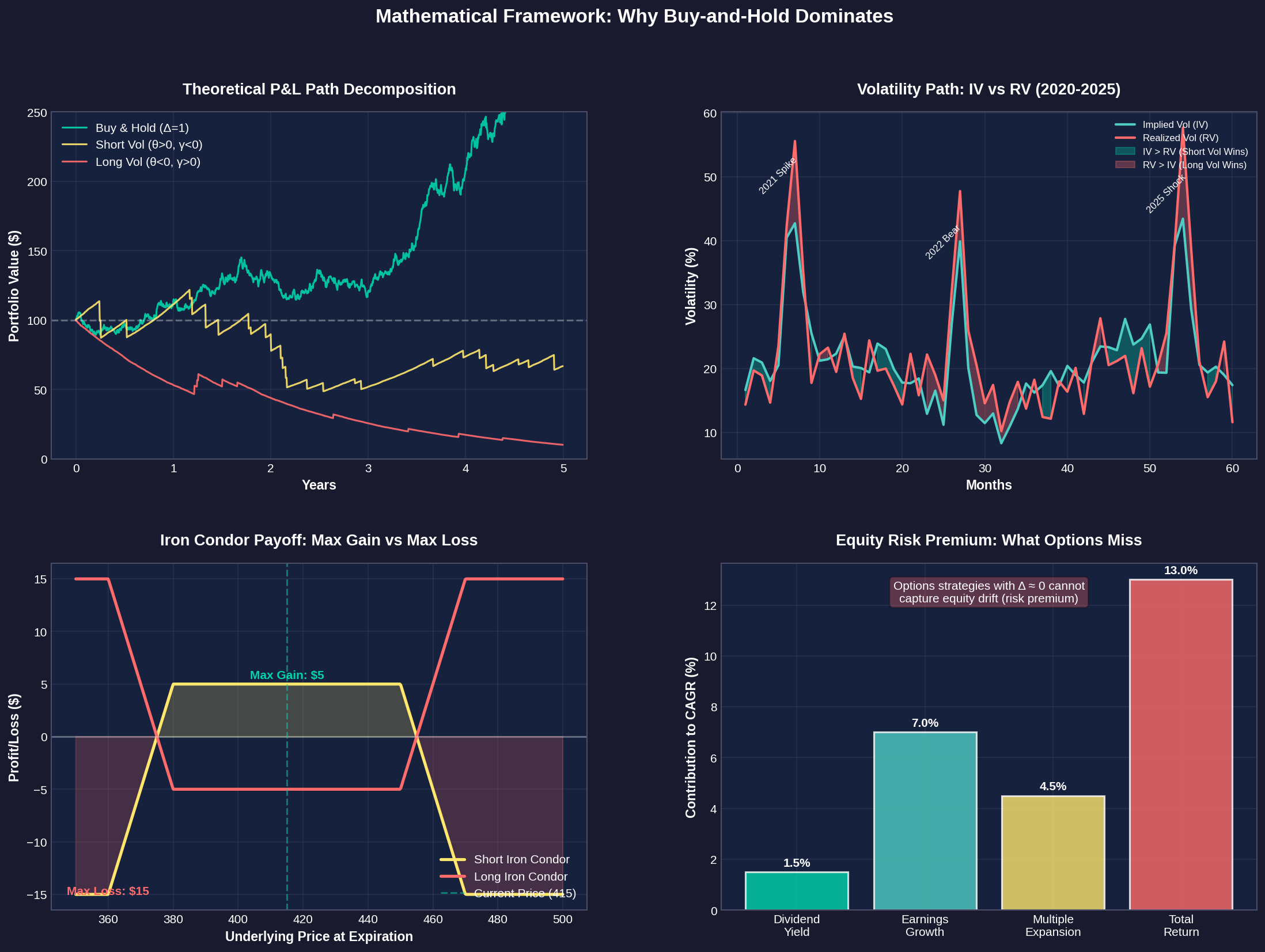

2. The Fundamental Problem: Options Suppress Delta Exposure

SPY produced a multi-year drift-dominated up-move, returning roughly +86.89% on used capital over 5 years.

Buy-and-Hold therefore had:

Δ ≈ +1.00 (full delta exposure)

γ = 0 (no gamma)

θ = 0 (no theta decay)

ν = 0 (no vega risk)

No roll losses

No slippage

No fee drag

Mathematically, the buy-and-hold return is simply:

R_B&H = (P_T / P₀) - 1where P₀ and P_T are starting and ending prices.

Every options structure tested begins by reducing delta exposure:

Strategy Delta Exposure Implication

────────────────────────────────────────────────────────────────

Short Iron Condor |Δ| ≪ 1 Minimal directional exposure

Long Iron Condor Δ ≈ 0 Delta-neutral

Short Strangle Δ modest → 0 Slight bias neutralized over time

Long Strangle Δ ≈ 0 Delta-neutralThe mathematical consequence is inescapable:

R_option ≪ R_B&H whenever the underlying trends upwardOptions cannot mechanically compete with high-delta exposure in a rising market.

3. Volatility Path Dependency: The Achilles Heel

SPY’s realized volatility path during 2020–2025 included:

Violent whipsaws

Two major volatility expansions (2022, 2025)

Several sharp but brief shocks

A long bull run after 2023

Short Volatility P&L Model

The expected P&L of short volatility trades can be approximated as:

E[P&L_short_vol] ≈ (IV - RV) × t - Σ(tail_losses)Where:

IV = Implied Volatility (what you sell)

RV = Realized Volatility (what actually happens)

t = time

tail_losses = losses from large moves

When tail losses are large:

Σ(tail_losses) ≫ (IV - RV) × tThe data confirms this: Short strategies experienced catastrophic losses during 2022 and early 2025 volatility expansions, with drawdowns exceeding -100% on capital deployed.

Long Volatility P&L Model

Long volatility strategies have the opposite problem:

E[P&L_long_vol] ≈ γ × E[shock_magnitude] - |θ| × tFor this to be profitable requires:

γ × E[shock] > |θ| × tSPX/SPY did not produce sustained volatility at the right times. The volatility spikes were:

Not extreme enough

Not frequent enough

Not persistent enough

Quickly mean-reverting after moves

So theta (time decay) dominated gamma (convexity benefit) over the 5-year window.

4. Iron Condor Mathematics: Capped Upside, Unlimited Downside Frequency

An iron condor is structurally a short variance trade where:

Max Gain = Net Credit

Max Loss = Spread Width - CreditTypical risk-reward: Risk $5 to make $1

This means a single tail event can wipe out dozens of wins.

Backtest Statistics (SPY Long Iron Condor):

Metric Value

───────────────────────────────

Profit Rate 27.13%

Loss Rate 72.87%

Average Win $416.04

Average Loss -$199.86

Max Drawdown -100.88%This reflects negative convexity with γ < 0. Negative gamma means losses accelerate during volatile moves.

Buy-and-Hold has γ = 0, therefore no convexity penalty.

The Expectancy Problem

Trade expectancy is calculated as:

E = (WR × Avg_Win) + (LR × Avg_Loss)For the Long Iron Condor:

E = (0.2713 × $416.04) + (0.7287 × -$199.86) = -$32.77 per tradeOver 1,198 trades, this compounds to massive losses.

5. Long Strategies: Theta Decay Dominates Gamma Benefit

Long ICs and long strangles are long convexity trades with:

γ > 0 (positive gamma)

θ ≪ 0 (large negative theta)

Their expectancy formula becomes:

E[P&L] = γ × (Shock_Frequency × Shock_Magnitude) - |θ| × tThe Critical Threshold

For profitability, the following inequality must hold:

γ × σ²_realized > |θ|Where σ²_realized is the actual variance of the underlying.

During 2020-2025, this threshold was rarely crossed because:

Volatility spikes were brief

Vol quickly mean-reverted

The drift component dominated shock component

Premium paid for convexity exceeded realized benefits

Long Strangle Results (SPY):

Metric Value

─────────────────────────────────────

Profit Rate 19.26%

Loss Rate 80.74%

Average Win $908.53

Average Loss -$449.35

Total Premium Paid -$595,395

Return on Capital -100%The strategy bled to zero from theta decay over 5 years.

6. Geometric Return Mathematics: The Volatility Drag Problem

The geometric return of Buy-and-Hold is:

G_B&H = μ - ½σ²Where:

μ = arithmetic mean return

σ = volatility of returns

Options strategies have significantly higher variance (σ²) in P&L because:

They reset frequently (1,198-1,220 trades)

Each trade has capped gains or fat-tailed losses

Bid/ask spreads add noise

Rolling and slippage add variance

Thus:

G_options = μ_options - ½σ²_optionsSince:

σ²_options ≫ σ²_B&HWe get:

G_options < G_B&HEven if arithmetic returns were equal, the higher variance of options strategies creates a “volatility drag” that destroys geometric compounding.

Numerical Example

Assume both strategies have μ = 10% arithmetic return:

Strategy σ Vol Drag (½σ²) Geometric Return

────────────────────────────────────────────────────────────

Buy & Hold 18% 1.62% 8.38%

Options 45% 10.13% -0.13%The options strategy turns a positive arithmetic return into a negative geometric return purely through variance.

7. Transaction Costs: The Silent Killer

Strategy # Trades Total Fees

─────────────────────────────────────────────

Buy & Hold 1 $0

Long Iron Condor 1,198 $8,236.52

Long Strangle 1,220 $4,714.88

Short Iron Condor 1,198 $8,236.52

Short Strangle 1,220 $4,751.48Even if expectancy were neutral, the fee drag alone explains long-run underperformance.

Each options trade involves:

Bid-ask spread crossing (4 legs for IC)

Commissions per contract

Rolling costs when managing positions

Assignment/exercise fees

Buy-and-Hold trades once.

8. The Greek Framework: Why Buy-and-Hold Has Structural Advantage

Greek Buy & Hold Short IC Long IC Short Strangle Long Strangle

──────────────────────────────────────────────────────────────────────────────

Δ (Delta) +1.00 ~0 ~0 ~0 ~0

γ (Gamma) 0 -Medium +Medium -High +High

θ (Theta) 0 +Medium -Medium +High -High

ν (Vega) 0 -Medium +Medium -High +HighWhy This Matters

Buy-and-Hold benefits from:

High Δ (captures equity drift)

No θ (no time decay)

No γ (no convexity penalty/benefit)

No vega risk (immune to IV changes)

Positive drift (equity risk premium)

Options spreads suffer from:

Reduced/neutralized Δ

Added negative θ (long vol) or convexity risk (short vol)

Constant rolling requirements

Large frictional costs

Volatility expansion damage

9. Equity Return Decomposition: What Options Miss

Long-run equity returns mathematically decompose as:

Total Return = Dividend Yield + Earnings Growth + Multiple ExpansionApproximate SPY CAGR breakdown (2020-2025):

Component Contribution

────────────────────────────────────

Dividend Yield ~1.5%

Earnings Growth ~7.0%

Multiple Expansion ~4.5%

────────────────────────────────────

Total ~13.0%Options strategies with Δ ≈ 0 cannot capture this equity risk premium.

They are essentially betting on:

Volatility mispricing (short vol)

Tail events (long vol)

Mean reversion (iron condors)

Rather than:

Corporate earnings growth

Dividend streams

Long-term multiple expansion

10. When These Strategies Would Work (Regime Analysis)

Short Strangles and Short Iron Condors (short γ, short ν)

Work well when:

Markets are range-bound (Δ ≈ 0 exposure is advantageous)

Realized vol < Implied vol persistently

Large shocks are infrequent

Trends are slow and drifty

Volatility mean-reverts quickly

Term structure is in contango

Ideal mathematical environment:

γ < 0 but low risk because price stays inside range

θ > 0 provides steady carry

ν < 0 works because IV slowly decays

Translation: Calm, sideways, choppy, low-trend markets.

Examples: Parts of 2017, 2019, and parts of 2023–2024

Long Iron Condors and Long Strangles (long γ, long ν)

Work well when:

Realized vol ≫ Implied vol

Large tail events cluster together

Price moves explosively in either direction

Implied vol is underpricing risk

Volatility of volatility is high

Ideal mathematical environment:

γ > 0 generating convex gains

ν > 0 because IV expands after entry

θ < 0 but γ + ν > θ

Translation: Crisis periods, regime shifts, black swan clusters.

Examples: 2008, March 2020, Flash crashes

SPX/SPY in 2020–2025 only had brief vol spikes — not enough for sustained profitability.

11. The Deepest Reason: Options Cannot Capture Equity Drift

Options = mean reversion bet

Equities = long-term drift bet

All four option structures do one of the following:

Neutralize delta (iron condors, strangles)

Fight the drift with opposing convexity (short vol)

Bleed theta trying to catch gamma (long vol)

During 2020–2025, the drift won decisively.

In a world with an equity risk premium, Buy-and-Hold is not just simpler — it is mathematically advantaged.

12. Conclusion and Practical Implications

These backtests illustrate a fundamental truth of quantitative options trading:

When equities trend upward, strategies that suppress delta and introduce theta decay or convexity risk will always underperform.

Short vol died in tail expansions

Long vol died slowly from theta

Iron condors died from both

SPY & SPX simply drifted upward with no structural decay

When Might You Consider These Strategies?

Volatility spikes or anticipated macro events: If you expect an upcoming shock (geopolitical event, rate decision), long-vol trades could pay off — but timing is nearly impossible.

Range-bound markets: In tranquil sideways markets, short premium can work — with tight position sizing and strict risk management.

Tactical hedging: Using options to protect existing equity positions, rather than as standalone alpha generation.

The Hard Truths Remain:

Tail risk is real and underpriced — Short-premium strategies remain fragile

Theta decay and time horizon mismatch — Long-vol needs large moves that don’t come reliably

Transaction costs compound — 1,200 trades × bid-ask spreads × commissions = death by a thousand cuts

Mis-timing is fatal — A bet on “volatility soon” can bleed out waiting

Final Thought

In a bull market with positive drift, the simplest strategy wins.

Options strategies are sophisticated tools for sophisticated problems. But the problem most retail traders face isn’t “how do I extract volatility premium from the variance risk premium” but rather “…how do I participate in long-term wealth creation?”

For that problem, Buy-and-Hold seems to be the mathematically dominant solution in the current market regime.

Backtest Parameters: 45 DTE, 16Δ options, daily entry, SPY/SPX, November 2020 - November 2025. Data Source: TastyTrade backtester.

This post is about methodology, not recommendations. Options and derivatives are complex instruments and this analysis probably contains errors. If you find them, let me know.

The information presented in Math & Markets is not investment or financial advice and should not be construed as such.

I love your content. Props!

This could mean that the recent multi-year up drift move was corrective (down moves in contrast happened fast and with vol jumps) - this might suggest that we could experience in the next few a higher vol up move where eventually delta exp won’t be overwhelmed by theta….