Venezuela Crisis Oil Trading Strategy II: Sector Mapping

Part 2: Sector Mapping and the “Chess” Trade Logic

This is PART 2 of a standalone series on the Venezuela Crisis Oil Trading Strategy.

In Part 1, I laid out the scenario framework: four possible paths for post-Maduro Venezuela, with the “Libya Model” (prolonged instability) as the ~47-50% base case. The punchline was that directional oil isn’t the high-edge trade — the Sharpe ratio is too low given the variance across scenarios.

So what is the trade?

This part maps specific sectors and companies to our scenario framework, building a winners/losers matrix that reveals which exposures work across multiple paths. The goal is finding trades that don’t require us to be right about the headline.

As an amateur chess player, I’d say Math & Markets is not in the business of making a d4 move — we are not trying to define our board before the market knows it’s been defined. That’s for the big boys.

I would say treat this like Nd5 — redeploying capital to the square where the next act unfolds.

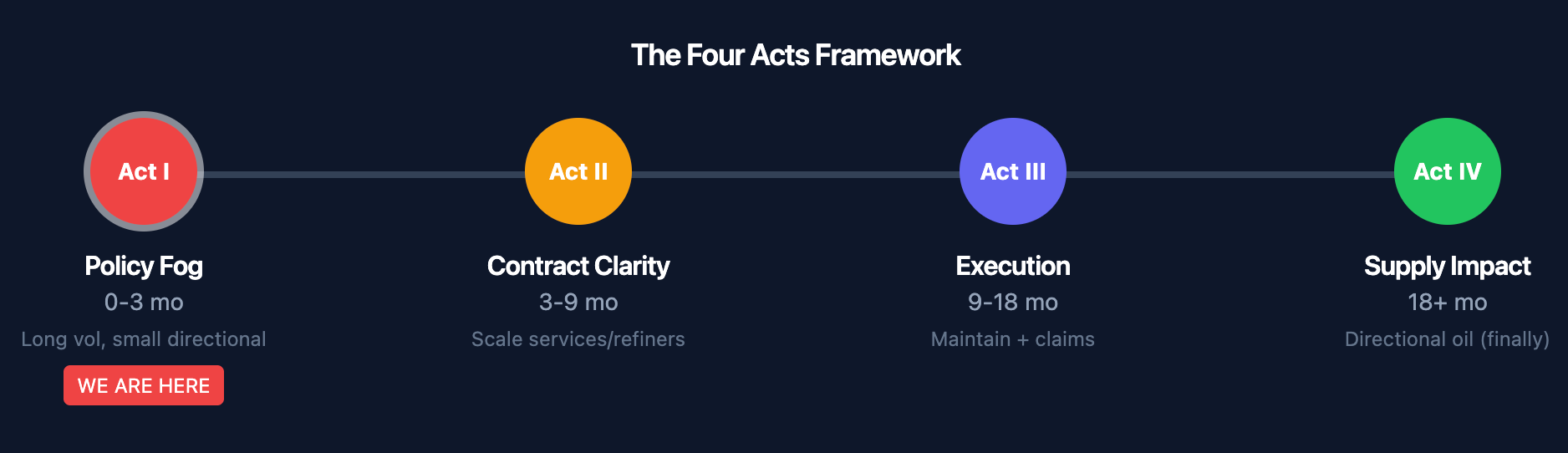

The “Chess” Framework: Four Acts

Before diving into company specifics, here’s the temporal structure. Venezuela will likely move through distinct phases, and each phase has different optimal exposures:

Act I (0–3 months): Policy Fog + Volatility

We’re here now. The Trump administration has made contradictory statements within 24 hours (”running the country” vs. State Department saying “not governing day-to-day”). Sanctions architecture is unclear. International response is still forming.

Optimal exposure: Long volatility, small directional positions

Avoid: Assuming immediate barrels, heavy capex plays

Act II (3–9 months): Contract Clarity + Early Tenders

If we move toward reopening, this is when licensing regimes crystallize, JV contracts get negotiated, and service companies start bidding on rehabilitation work.

Optimal exposure: Scale into services and refiners Monitor: OFAC announcements, Chevron operational status, tender activity

Act III (9–18 months): Execution + Capital Flows

Actual mobilization of equipment, crews, and capital. Infrastructure repairs begin. Claims settlements may accelerate if governance stabilizes.

Optimal exposure: Maintain services; add claims optionality Monitor: Rig counts, PDVSA bond prices, production data

Act IV (Optional): Physical Supply Impact

Only if Acts I-III succeed do we get sustained output increases. This is the “long oil” moment — but it’s 2+ years out in most scenarios.

Optimal exposure: Directional long oil becomes core (finally) Condition: Governance stability, multi-year capital inflows

The chess insight: You don’t win by predicting the next headline. You win by identifying which Act we’re in and holding the correct exposures for that phase.

Company and Sector Mapping

1. Chevron (CVX): The First-Mover

Theme: Operational footprint + continuity optionality

Chevron is the only major U.S. oil company currently operating in Venezuela, accounting for about 25% of current production (~140K bbl/day in Q4 2025). They never fully exited when others did, maintaining a skeleton presence through the sanctions era.

Pros:

Established relationships with PDVSA and local workforce

If reopening happens, they’re positioned to expand immediately

Policy optionality embedded in current operations

Cons:

Large-cap dilution: Venezuela is a rounding error on CVX’s $280B market cap

Near-term earnings impact: negligible even in bull case

Political risk: if things go wrong, they’re the visible target

Scenario Performance:

CVX BY SCENARIO

─────────────────────────────────────

Syria (quick) + First to expand

Libya (chaos) 0 Operations protected, no growth

Hybrid (grind) + Slow expansion, first-mover edge

Escalation + Geopolitical risk premium

─────────────────────────────────────Best use: Defensive energy exposure with embedded Venezuela optionality. Not the primary expression, but a reasonable place to park capital if you want broad energy exposure anyway.

2. Oil Services: Schlumberger (SLB) and Baker Hughes (BKR)

Theme: Rehabilitation and capex intensity

This is where the real torque is. Any Venezuela recovery story is fundamentally a capex and rehabilitation story — workovers, recompletions, midstream repairs, pipeline replacement, well interventions. That’s oil services.

Venezuela’s infrastructure needs are staggering:

50+ year-old pipelines

Decades of deferred maintenance

Expertise gap from brain drain

Equipment that hasn’t been serviced since the 2000s

If contracts become enforceable and foreign operators return, the service companies get paid first — before even a single new barrel flows.

Pros:

Highest torque to “rebuild” narrative

Revenue comes early in the recovery timeline (Act II-III)

Works even if oil prices are range-bound

Diversified global business provides downside support

Cons:

Requires contract enforceability and security

Mobilization takes time; equipment is elsewhere

Execution risk in unstable environment

Scenario Performance:

SLB/BKR BY SCENARIO

─────────────────────────────────────

Syria (quick) ++ Rebuild begins immediately

Libya (chaos) – No contracts, no mobilization

Hybrid (grind) ++ Slow but steady rehab work

Escalation + Delayed but eventual rebuild

─────────────────────────────────────Best use: Long services vs. short upstream (XLE or majors basket). This isolates the rehabilitation factor from commodity direction. The relative trade works even if oil is flat or down.

3. Claims Optionality: ConocoPhillips (COP) and ExxonMobil (XOM)

Theme: Settlement probability on historical expropriations

When Chávez nationalized the oil industry in 2007, foreign companies were kicked out. Some fought back:

ConocoPhillips won an $8.7B ICSID arbitration award in 2019 (never collected)

ExxonMobil received partial compensation but has outstanding claims

Other companies (ENI, Total, Repsol) have various unresolved disputes

Regime change — especially U.S.-backed regime change — increases the probability these claims get addressed. A new government seeking international legitimacy might prioritize settling with Western majors.

Pros:

Optionality on claim monetization

Settlement could be material for COP

New regime has incentive to clean up legal overhang

Cons:

Timing completely uncertain

NPV heavily discounted (could take years)

Enforcement remains question even post-settlement

Scenario Performance:

COP/XOM (CLAIMS) BY SCENARIO

─────────────────────────────────────

Syria (quick) + Settlement path opens

Libya (chaos) 0 Who do you sue?

Hybrid (grind) + Eventual resolution

Escalation 0/+ U.S. pressure may force resolution

─────────────────────────────────────Best use: Small, venture-like optionality position. Size it like a call option that might expire worthless. Don’t anchor your book on timing.

4. Refiners: Valero (VLO), Marathon Petroleum (MPC), PBF Energy (PBF)

Theme: Heavy crude availability + crack spread economics

This is the targeted play I flagged in Part 1. Venezuela produces Merey — heavy, sour crude that Gulf Coast refiners are specifically configured to process.

The economics:

Heavy crude trades at a discount to light sweet (quality differential)

Complex refiners like Valero can process heavy crude into high-value products

If Venezuelan supply tightens, heavy crude premium expands

If supply normalizes, crack spreads benefit from cheaper feedstock

Either way, refiners with heavy crude processing capability are positioned well.

Pros:

Benefits whether Venezuela supply tightens OR normalizes

Crack spread exposure partially independent of oil direction

Gulf Coast configuration is the right asset base

Cons:

Acute supply disruptions (sabotage) can compress margins temporarily

Policy could block Venezuelan crude flows entirely

Refining margins volatile for other reasons

Scenario Performance:

VLO/MPC/PBF (REFINERS) BY SCENARIO

─────────────────────────────────────

Syria (quick) + Cheap feedstock returns

Libya (chaos) – Heavy crude premium squeezes margins

Hybrid (grind) + Gradual feedstock normalization

Escalation – Acute supply disruption

─────────────────────────────────────Best use: Long refiners vs. short upstream E&Ps. This captures the heavy crude differential without taking oil direction risk.

5. Natural Gas

Conclusion: Not the cleanest Venezuela expression.

Venezuela has significant gas reserves, but:

The direct link to current events is weak

Infrastructure is even worse than oil

LNG export capacity doesn’t exist

Timeline for gas development is even longer than oil

The indirect link is via broader energy security risk premium — if you believe this event makes global energy supply less certain, LNG exporters and infrastructure plays benefit. But that’s a second-order effect.

If you want energy security exposure: Cheniere (LNG), Tellurian (TELL), midstream infrastructure. But don’t call it a Venezuela trade.

6. Critical Minerals and Mining: The Hidden Play

Theme: Long-term optionality on $1.36 trillion in non-oil resources

This is the angle most analysis misses. Venezuela’s Orinoco Mining Arc contains significant deposits of gold, coltan (niobium-tantalum), bauxite, iron ore, and potentially rare earths. The infrastructure is even more destroyed than oil, and most current extraction is illegal/informal — but regime change could eventually unlock this.

Key minerals and relevant exposures:

MINERALS TRADE EXPRESSIONS

═══════════════════════════════════════════════════════════════════

Mineral Why It Matters Potential Plays

───────────────────────────────────────────────────────────────────

Gold Latin America's NEM, GOLD, GDX

largest reserves (supply disruption OR

(10,000 tons) entry opportunity)

Coltan/Tantalum Critical for Limited pure-play;

capacitors, defense, watch supply chain

EVs, smartphones tightness

Bauxite/Aluminum Was major regional AA (Alcoa), CENX

producer; restart (Century Aluminum)

potential

Rare Earths Unverified but MP Materials (MP),

reported in Guayana REMX ETF

Shield

Mining Services Equipment for any CAT, DE, TEX

rehabilitation (long-dated)

───────────────────────────────────────────────────────────────────Scenario Performance:

MINERALS EXPOSURE BY SCENARIO

─────────────────────────────────────────

Syria (quick) ++ Fastest path to development

Libya (chaos) – Illegal mining continues, no investment

Hybrid (grind) + Slow progress, some tenders

Escalation 0 Uncertain—depends on specific dynamics

─────────────────────────────────────────Key insight: Minerals are an Act IV+ story — even longer timeline than oil. But they explain why the U.S. might stay committed longer than a pure oil calculus would suggest. Critical minerals are a bipartisan national security priority.

Best use: Small, long-dated optionality. LEAPS on gold miners or MP Materials if you believe the Syria/Hybrid scenarios play out over 2+ years. Not a near-term trade.

Watch for: Any mention of mining tenders, Orinoco Mining Arc policy, or Chinese company expulsions as signals that this angle is heating up.

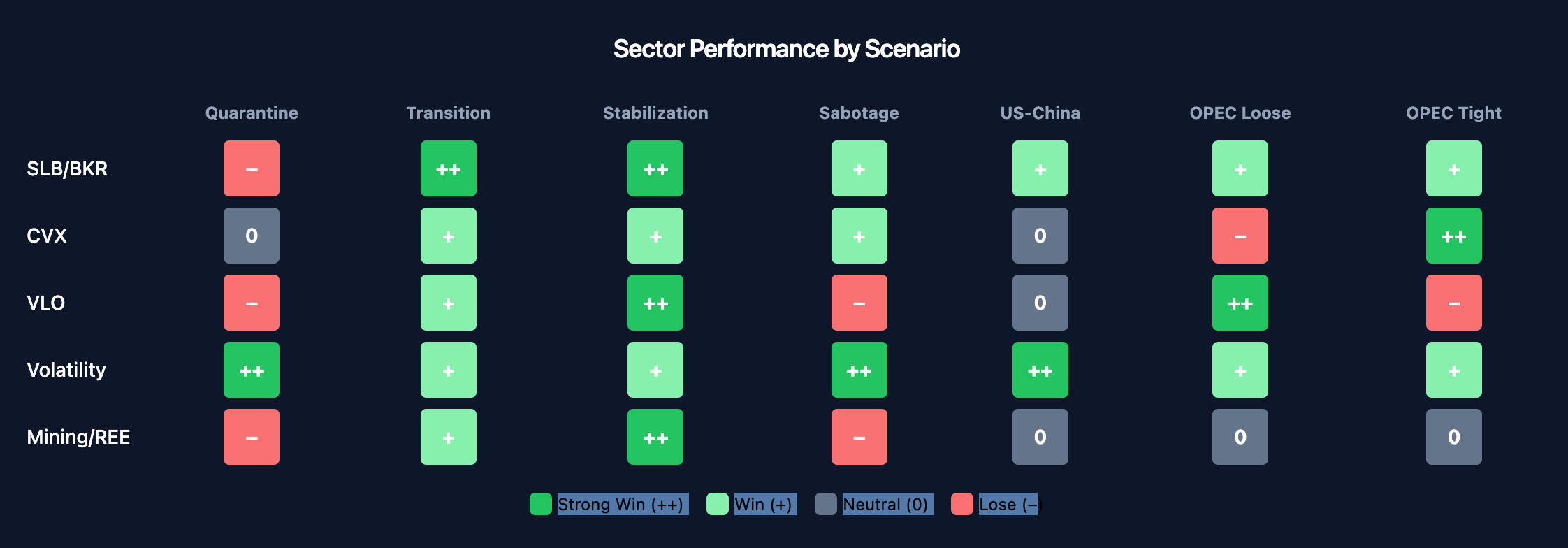

Winners/Losers Matrix: 6-18 Month Horizon

Here’s the full scenario matrix with ratings (++ strong winner, + winner, 0 mixed, - loser, -- strong loser):

SECTOR PERFORMANCE BY SCENARIO (6-18 Month Horizon)

====================================================================================================

Oil Vol SLB CVX XOM COP VLO Mining EM/ Best

Scenario Px /BKR Refin /REE LATAM Expression

----------------------------------------------------------------------------------------------------

S1. Quarantine 0/+ ++ - 0 0 0/+ - - -- Long vol +

/Blockade short rebuild

S2. Transition 0/+ + ++ + 0 + + + - Long services

+ Reopening vs short XLE

S3. Stabilization + + ++ + 0 + ++ ++ 0/- Long services

+ Rehab + refiners + miners

S4. Sabotage/ ++ ++ + + + 0/+ - - -- Long oil calls

Disruption (later) + vol

S5. US-China + ++ + 0/+ 0/+ 0 0/- 0/- -- Long vol +

Escalation (floor) barbell

S6. OPEC+ -/0 + + - - - ++ 0 0 Long refiners

Loosens + services

S7. OPEC+ ++ + + ++ ++ + - 0 - Long upstream

Tightens beta

====================================================================================================

Reading the matrix:

Look for sectors that show positive outcomes across multiple scenarios:

SLB/BKR (Services): Positive in 5 of 7 scenarios, only negative in quarantine/blockade

Volatility: Positive in all 7 scenarios - policy fog guarantees repricing events

VLO (Refiners): Mixed but positive in key scenarios (S2, S3, S6)

Mining/REE: Only positive in S2, S3 (transition/stabilization) - concentrated bet on rehabilitation

CVX: Positive-to-neutral across most scenarios, rarely negative

Pure oil long: Only clearly positive in S4, S5, S7 - requires specific conditions

The matrix tells you where the robust trades live. Minerals are high-upside but scenario-dependent.

Core Trade Logic: Volatility + Relative Value

Why Long Volatility is the Default Position

Policy fog is not going away soon. Within 24 hours of the operation, we had:

Trump: “We’re going to run the country”

State Department: “We’re not governing day-to-day”

Trump: Machado “doesn’t have the support” to govern

Machado’s coalition: “Ready to assume power”

This is not an environment where implied volatility should be low. Every headline creates repricing. OPEC+ decisions, UN Security Council votes, Congressional war powers resolutions, China’s response — each is a volatility catalyst.

The trade: Even if spot oil is range-bound, volatility can remain elevated. You get paid for owning optionality in uncertain regimes.

Why Relative Value Beats Outright Oil

If the base case is Libya-style instability with an oversupplied global market, oil spikes fade. The 2025 price action proved this: geopolitical risk generated headlines but prices ended the year down 20%.

But relative winners still re-rate:

Services outperform if rehabilitation is the story

Refiners outperform if heavy crude economics shift

These don’t require oil to trend up — just for capital to flow toward Venezuela exposure

The trade: Long services (SLB/BKR) vs. short XLE or majors. This is a factor bet on “Venezuela matters” without betting on oil direction.

What We’re Watching This Week

Sunday (tonight):

Futures open 6pm ET — watch for gap direction

OPEC+ monthly meeting — expect confirmation of Q1 pause

Monday:

UN Security Council meeting (Russia/China backing Venezuela’s complaint)

Congressional reaction to war powers resolution

This week:

Venezuelan military posture — are they fragmenting or consolidating?

Colectivos response — street violence = Libya scenario confirmation

Chevron operational status — any disruption is news

Key Takeaways (Part 2)

Services (SLB/BKR) are the highest-torque play - positive in 5 of 7 scenarios

Volatility wins in every scenario - policy fog guarantees repricing

Refiners (VLO) offer targeted heavy crude exposure without oil direction risk

Mining/REE is a concentrated bet - only works in S2/S3, but high upside if rehabilitation succeeds

CVX is defensive with optionality - not the primary expression but reasonable

Claims (COP) are venture-style optionality - size accordingly

The “chess” insight: Match your exposures to the current Act, not the final outcome

Relative value beats outright: Long services vs. short upstream works across scenarios

What’s Next

In Part 3, we get into implementation: specific option structures, position sizing, and how to express these views with defined risk.

In Part 4, the decision framework — what triggers cause us to update probabilities, how OPEC+ decisions shift the regime, and an operational playbook for the next 6-18 months.

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

These posts are about methodology, not recommendations. Some of the approaches discussed here involve commodities (like oil) and complex instruments (e.g., options and derivatives) and not suitable for all investors. Many of my analyses probably contain errors — if you find them, please let me know.

While I may hold positions in some of the underlying assets discussed here, my posts are not an endorsement or a recommendation of those underlying assets. This is a quickly emerging and fast-changing situation, so please be wary of information staleness.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.