Venezuela Crisis Oil Trading Strategy III: Implementation

Part 3: Implementation — Option Structures, Position Sizing, and Risk Management

This is PART 3 of a standalone series on the Venezuela Crisis Oil Trading Strategy.

It’s Monday and I wanted to get this published before the markets open!

Parts 1 and 2 established the thesis: the Venezuela shock is primarily a volatility and relative value opportunity, not a directional oil bet. Services (SLB/BKR) and refiners (VLO) are the cleanest expressions, with volatility ownership as the meta-trade across all scenarios.

Now we can talk implementation.

This part covers specific option structures, position sizing rules, and portfolio blueprints for conservative, moderate, and aggressive risk appetites. I’ll include strike selection logic, roll plans, and the math behind sizing decisions.

First Principles: Why Options?

The Exchange Sacrifice

In chess, an exchange sacrifice is when you give up a rook (worth 5 points) for a knight or bishop (worth 3 points). On paper, you’re down material. But you’re trading static value for dynamic compensation — better piece coordination, control of key squares, or attacking chances that are hard to quantify.

Options premium works the same way.

When you buy a collarized call spread instead of holding the underlying, you’re sacrificing some upside (the cap) and paying theta (time decay). On a spreadsheet, the expected value of owning the stock outright might look higher.

But you’re getting something the spreadsheet doesn’t capture:

Defined risk — You know your max loss before you enter

Convexity — Small premium, asymmetric payoff in tail scenarios

Flexibility — Capital freed up for other positions

Survivability — You can be wrong on timing and still stay in the game

Petrosian, the world champion famous for prophylactic play, once said: “Some sacrifices are sound, the rest are mine.” His opponents couldn’t calculate whether his sacrifices were brilliant or bluffs — and that uncertainty itself was an edge.

The structures in this section are Petrosian trades. We’re giving up some expected value on the best-case path in exchange for robustness across all paths. The half-Kelly sizing, the defined-risk structures, the roll discipline — these aren’t concessions in my view. They ARE the strategy.

The WSBer sees the capped upside and thinks we’re leaving money on the table. Readers of Math & Markets (hopefully) see a position that survives long enough for the thesis to play out.

On a serious note, for a scenario-driven thesis with high uncertainty, options are the right tool for several reasons:

Defined risk: Premium paid is max loss

Convexity: Asymmetric payoff if tail scenarios materialize

Flexibility: Can express views on direction, volatility, or both

Capital efficiency: Free up capital for diversification

The downside is theta decay — time eats your position (r/thetagang celeberates). The structures below are designed to minimize bleed while maintaining exposure to the scenarios we care about.

Strategy Menu (Ranked by Clarity of Edge)

Strategy 1: Long Energy Volatility

Goal: Monetize repeated repricing events

Edge clarity: High (policy fog is persistent)

Strategy 2: Long Services vs. Short Energy Beta

Goal: Isolate rebuild/capex factor

Edge clarity: High (works across most scenarios)

Strategy 3: Long Refiners vs. Short Upstream

Goal: Capture heavy crude economics

Edge clarity: Medium-high (depends on supply dynamics)

Strategy 4: Claims Optionality

Goal: Monetize settlement probability

Edge clarity: Medium (timing uncertain)

Strategy 5: Fade Oil Spikes (Conditional)

Goal: Exploit oversupply regime

Edge clarity: Lower (requires disruption to NOT occur — yes, really)

Detailed Option Structures

A. Core: Long Volatility Without Excess Bleed

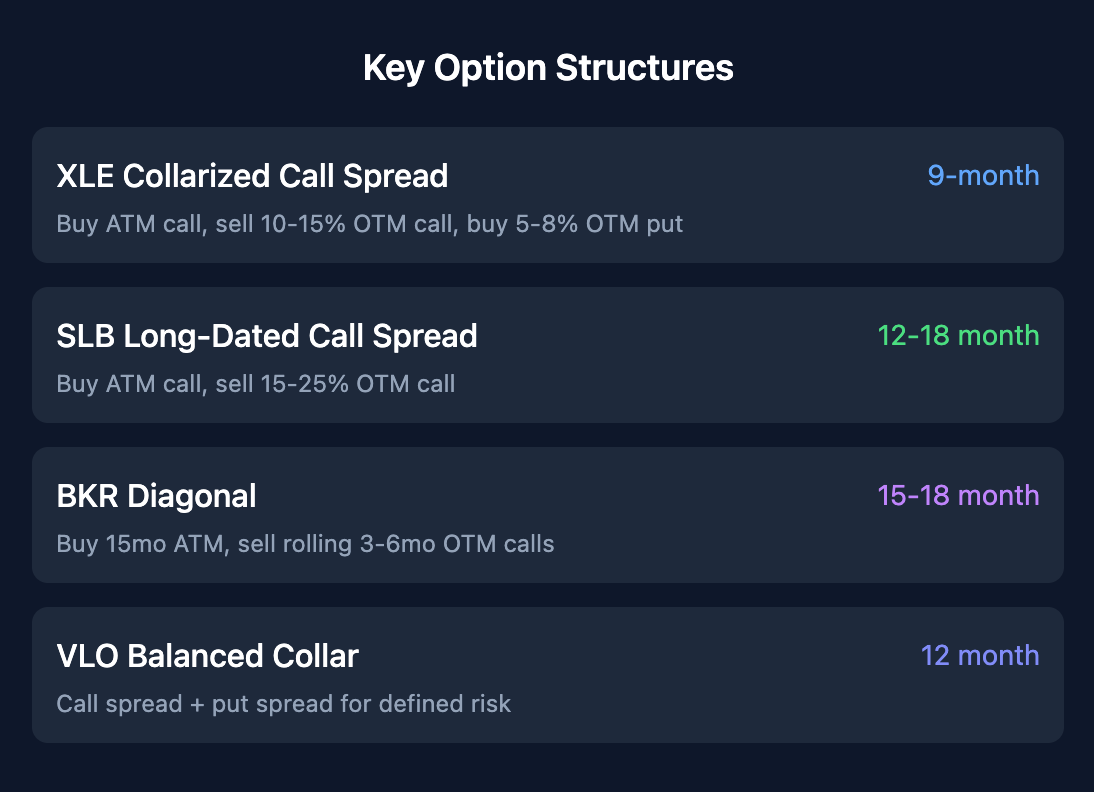

Structure 1: XLE Collarized Call Spread (6–12 months)

This is the primary volatility expression. We’re buying upside participation, defining our downside, and funding part of the structure with premium collection.

Construction:

Buy ATM call (e.g., XLE $92 call if spot = $92)

Sell 10-15% OTM call (e.g., $103 call)

Buy 5-8% OTM put (e.g., $87 put)

Sell 15-20% OTM put (e.g., $78 put)

Payoff Profile:

Max gain: Capped at upper call strike minus entry cost

Max loss: Defined by put spread width

Breakeven: Near ATM

Theta: Significantly reduced vs. naked calls

Tenor: 9 months preferred (balances theta decay vs. time for scenarios to play out)

Roll Plan:

Roll at <4 months to expiry to avoid accelerating theta

If IV spikes: Take partial profits on call side, maintain put hedge

If spot rallies past short call: Roll short call up and out

Why this works: You participate in upside moves (policy clarity, OPEC+ tightening) while the collar structure reduces bleed. The sold put funds part of the hedge.

Structure 2: USO/BNO Put Spread Funded by Small Call (9–12 months)

This structure aligns with the “spike fades” thesis—oil rallies sell off in an oversupplied market.

Construction:

Buy 5% OTM put (e.g., USO $68 put if spot = $72)

Sell 15% OTM put (e.g., $62 put)

Sell 15-20% OTM call (small size, e.g., $84 call) to reduce net debit

Payoff Profile:

Profits if oil fades after spikes

Defined loss on put spread

Short call is a funding mechanism, not a core view

Adjustment Rule: If disruption scenario emerges (sabotage, escalation):

Buy back short call immediately

Convert to call spread or outright long

Why this works: Aligns with base case (oversupply persists), but the adjustment rule protects against being wrong.

B. Satellite: Rebuild/Rehabilitation Trades

Structure 3: SLB Long-Dated Call Spread (12–18 months)

Services are the high-conviction play. This structure gives time for the rehabilitation narrative to develop.

Construction:

Buy ATM or slightly ITM call (e.g., SLB $42 call if spot = $44)

Sell 15-25% OTM call (e.g., $52 call)

Tenor: 12-18 months (Act II/III timeline)

Payoff Profile:

Capped upside, but realistic target range

Reduced cost vs. outright call

Theta manageable at longer tenors

Scaling Plan:

Enter 50% position now

Add second 50% if tenders/contracts announced (Act II confirmation)

Ladder the second tranche 3 months after first

Why this works: Services lead the recovery story. The long tenor gives scenarios time to unfold without forcing a near-term resolution.

Structure 4: BKR Diagonal Call Spread (Multi-Leg, 15–18 months)

A diagonal harvests elevated IV on the short leg while maintaining long convexity.

Construction:

Buy 15-18 month ATM call (e.g., BKR $38 call, 15 months out)

Sell 3-6 month 10-15% OTM call (e.g., $42 call, 4 months out)

Roll the short call 2-3 times as it expires

Management:

Each time short call expires worthless: Collect premium, sell next 3-6 month OTM call

If stock rallies through short strike: Roll up and out, or close

Stop Selling Short Calls If:

IV collapses below historical average

Clear catalyst crystallizes (you want full upside participation)

Why this works: You’re getting paid to wait. The short calls fund your long position while you wait for Act II/III.

Structure 5: Services vs. Majors Pair (Option Expression)

This pairs trade isolates the capex/rehab factor from commodity direction.

Construction:

SLB/BKR side: Call spreads (as above)

XOM/CVX (or XLE) side: Put spreads

Example:

Long SLB 12-month $42/$52 call spread

Long XOM 12-month $100/$90 put spread (profits if XOM underperforms)

Why this works: If the Venezuela story is “rebuild” rather than “oil up,” services outperform majors. This structure profits from that divergence regardless of oil direction.

C. Refiners: Heavy Crude Economics

Structure 6: VLO Balanced Collar (12 months)

Construction:

Buy ATM call (e.g., VLO $135 call if spot = $135)

Sell 15% OTM call (e.g., $155 call)

Buy 10% OTM put (e.g., $122 put)

Sell 20% OTM put (e.g., $110 put)

Sabotage Adjustment: If disruption/sabotage risk rises:

Do NOT sell the downside put

Keep it as tail protection

Accept higher net debit

Why this works: Refiners benefit from normalized heavy crude supply OR from tight crack spreads. The collar manages both upside and downside while maintaining the core thesis.

D. Event Optionality: Claims

Structure 7: COP LEAPS Call Spread (12-18 months)

Construction:

Buy ATM LEAPS call (e.g., COP $98 call, 15 months out)

Sell 20-30% OTM call (e.g., $120 call)

Sizing Rule:

Treat like venture capital - size for total loss acceptable

Maximum 1-2% of portfolio

Scale only if settlement mechanisms become credible (court decisions, new government announcements)

Why this works: Claims are binary. Either they get addressed or they don’t. LEAPS give time for the legal/political process to unfold.

E. Long-Term Optionality: Critical Minerals

Structure 8: Mining/REE LEAPS (18-24 months)

This is an Act IV+ play - only deploy if you believe the Syria or Stabilization scenarios are likely AND have a multi-year horizon.

Construction (choose one or combine):

Gold miners (supply disruption OR entry optionality):

Buy NEM or GDX 18-24 month ATM call

Sell 25-30% OTM call to reduce cost

Thesis: Either Venezuela gold supply gets disrupted (bullish gold) or U.S. miners eventually get access

Critical minerals (rare earth/coltan optionality):

Buy MP Materials (MP) 18-24 month call spread

Strike: ATM / 30% OTM

Thesis: If Venezuela’s rare earth deposits prove commercial and U.S. gains access, MP benefits from validation of Western rare earth thesis

Mining equipment (rehabilitation infrastructure):

Buy CAT 18-24 month call spread

More diversified - captures general infrastructure rebuild, not just Venezuela

Sizing Rule:

Maximum 2-3% of portfolio combined

This is a “lottery ticket” allocation

Only add after clear signals of mineral sector policy (tenders, Orinoco Mining Arc announcements)

Key triggers to watch:

Any mention of mining tenders or Orinoco Mining Arc policy

Chinese company expulsions from mining sector

U.S. critical minerals task force announcements re: Venezuela

Why this works (or doesn’t): Minerals are a longer timeline than oil (infrastructure is worse, regulatory framework non-existent). But the strategic importance of critical minerals means U.S. policy may stay committed longer. This is optionality on U.S. persistence, not near-term production.

Position Sizing Framework

Kelly Criterion Application

From Part 1, our Monte Carlo analysis showed:

Expected 6-month Brent move: +$3.57 (probability-weighted, minerals-adjusted)

Standard deviation: ~$5.50

Sharpe-like ratio: ~0.65

Full Kelly = EV / Variance = $3.57 / ($5.50)^2 = ~12%

Half-Kelly (conservative): 6% of portfolio in aggregate Venezuela thesis

But this is spread across multiple structures, not one position.

Suggested Risk Budget Allocation

Conservative Portfolio (Volatility Hedge + Small Optionality)

CONSERVATIVE ALLOCATION

───────────────────────────────────────────────────────

Position Allocation Structure

───────────────────────────────────────────────────────

XLE collarized call spread 40% Core vol exposure

SLB call spreads 25% Rebuild optionality

VLO structure 15% Heavy crude play

BKR diagonal 10% Additional services

USO put spread 10% Fade spike expression

───────────────────────────────────────────────────────Entry signals: Vol not elevated vs. realized, calm tape before policy resolution Stop conditions: Durable quarantine/blockade with no reopening path

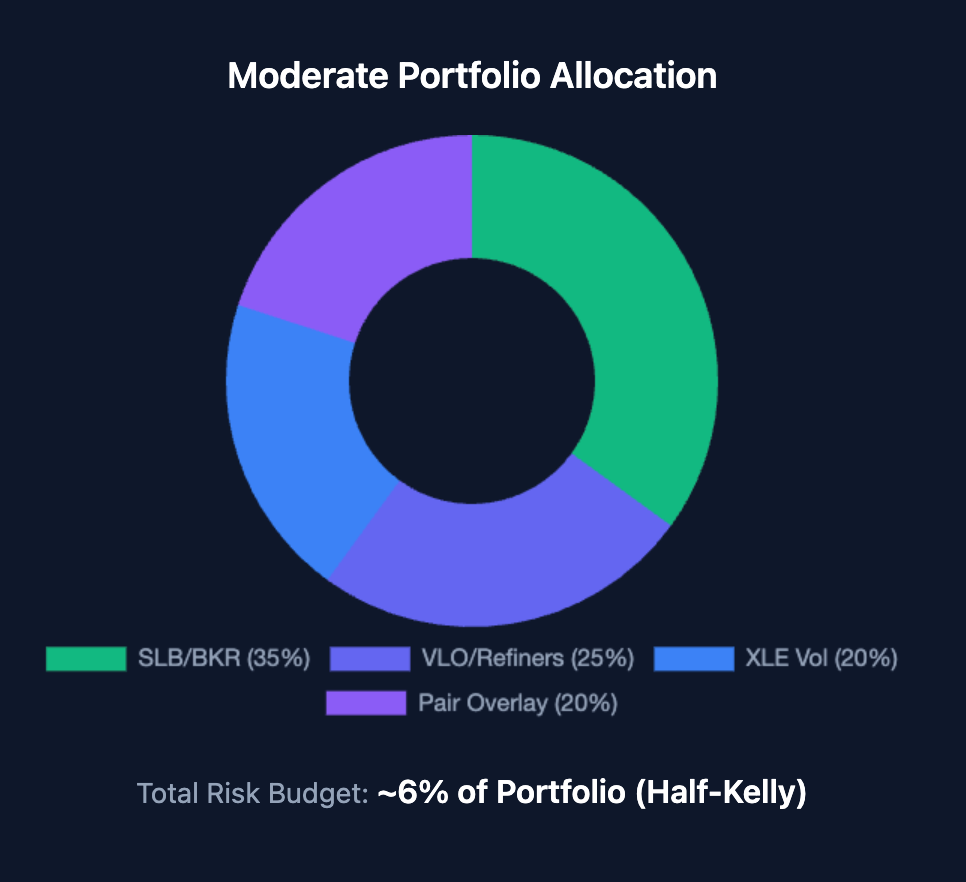

Moderate Portfolio (Relative Value Rebuild)

MODERATE ALLOCATION

───────────────────────────────────────────────────────

Position Allocation Structure

───────────────────────────────────────────────────────

SLB/BKR call spreads 35% Primary thesis

VLO/refiners 25% Heavy crude economics

XLE vol structure 20% Volatility participation

Pair overlay (short upstream) 20% Factor isolation

───────────────────────────────────────────────────────Entry signals: Evidence of reopening—tenders, licensing, transitional authority Stop conditions: OPEC+ deep cuts (rotate to upstream), sustained blockade

Aggressive Portfolio (Tail Risk Barbell)

AGGRESSIVE ALLOCATION

───────────────────────────────────────────────────────

Position Allocation Structure

───────────────────────────────────────────────────────

XLE vol + upside 25% Core expression

Oil upside tail calls 20% Escalation optionality

SLB/BKR convexity 25% Rebuild upside

COP claims optionality 10% Settlement lottery

Mining/REE LEAPS 10% Minerals optionality

EM hedge 10% Downside protection

───────────────────────────────────────────────────────Entry signals for minerals: Mining tender announcements, Orinoco Arc policy shifts

Stop conditions: Clear de-escalation + negotiated transition + no disruption

I can’t stress this enough: please be warned that this is obviously a high-risk, high-reward allocation — you need to have clearly defined exit criteria if you go with this portfolio allocation. Risk management is key!!

Risk Management Rules

Position-Level Rules

Maximum single position: 5% of portfolio at entry

Maximum sector concentration: 15% in any one sector

Total Venezuela thesis: Capped at half-Kelly (~6% of portfolio)

Stop-loss on directional futures: 3% adverse move triggers review

Calendar spread stop: $1 spread contraction triggers exit

Portfolio-Level Rules

Correlation awareness: Services and refiners are both energy—they can move together

Hedge requirement: Aggressive portfolios must include EM/LATAM or macro hedge

Roll discipline: Roll at <4 months to expiry, no exceptions

Profit-taking: Scale out 25% if position hits 50% of max gain

Scenario Revision Rules

Update probabilities weekly. Major triggers that shift the distribution:

SCENARIO REVISION TRIGGERS

───────────────────────────────────────────────────────

Trigger Probability Shift

───────────────────────────────────────────────────────

Machado sworn in Syria: 15% → 40%

Major Caracas violence Libya: 50% → 70%

Russia/China military aid Escalation: 5% → 15%

Exxon announces return Syria: 15% → 35%

Chevron evacuates Libya: 50% → 75%

───────────────────────────────────────────────────────When probabilities shift materially (>15% on any scenario), rebalance positions accordingly.

Implementation Timeline

Week 1 (Now)

Establish core XLE vol position (Structure 1)

Initiate 50% of SLB position (Structure 3)

Set alerts for key trigger events

Week 2-4

Add VLO position after UN Security Council meeting clarity

Consider USO put spread if spike occurs and fades

Month 2-3

Complete SLB/BKR build-out if tender activity begins

Initiate pairs trade (services vs. majors) if rehabilitation narrative strengthens

Month 6+

Reassess entire framework based on which Act we’re in

Add claims optionality only if settlement path becomes credible

What This Doesn’t Cover

To be completely transparent about limitations:

Execution risk: Bid-ask spreads on longer-dated options can be wide

Liquidity risk: SLB/BKR options less liquid than XLE

Correlation assumptions: Scenarios are not mutually exclusive; hybrids occur

The Trump factor: The current administration has shown itself to be a bit of a wild card, so it is important to factor that into any decision-making process

Black swan: None of these structures protect against true left-tail events (nuclear, pandemic, etc.) — that includes policy changes out of the blue

My own uncertainty: These probability estimates are subjective; I could be wrong (and very, very often, I am!)

Key Takeaways (Part 3)

Collarized call spreads are the core volatility expression - reduced bleed, defined risk

Long-dated service calls align with the rehabilitation timeline (12-18 months)

Diagonals let you harvest IV while waiting for catalysts

Pairs trades isolate the “rebuild” factor from oil direction

Half-Kelly sizing suggests ~6% total portfolio allocation to Venezuela thesis

Claims are venture bets - size for total loss acceptable

Minerals are Act IV+ optionality - 18-24 month LEAPS, lottery ticket sizing

Roll at 4 months - no exceptions, theta accelerates after that

What’s Next

In Part 4, the decision framework — what triggers cause us to update probabilities, how OPEC+ decisions shift the regime, and an operational playbook for the next 6-18 months.

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

These posts are about methodology, not recommendations. Some of the approaches discussed here involve commodities (like oil) and complex instruments (e.g., options and derivatives) and not suitable for all investors. Many of my analyses probably contain errors — if you find them, please let me know.

While I may hold positions in some of the underlying assets discussed here, my posts are not an endorsement or a recommendation of those underlying assets. This is a quickly emerging and fast-changing situation, so please be wary of information staleness.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.