Venezuela Crisis Oil Trading Strategy I: Event & Scenarios

Part 1: The Event, The Scenarios, and Why This Isn’t About “Oil Up”

This is PART 1 of a standalone series on the Venezuela Crisis Oil Trading Strategy

On January 3rd, 2026, the United States military captured Venezuelan President Nicolás Maduro in a nighttime operation — the most significant U.S. intervention in Latin America since Panama in 1989. President Trump announced the U.S. would “run” Venezuela temporarily and tap its vast oil reserves.

The obvious trade is “long oil.” My view is that the obvious trade is probably wrong.

This is the first in a four-part series laying out a systematic, scenario-based framework for trading the Venezuela shock over a 6–18 month horizon.

The thesis: the highest-edge trades are not directional oil bets, but volatility, relative value, and sector rotation plays that work across multiple scenarios.

What Actually Happened

The operation unfolded under cover of darkness. U.S. forces struck targets in Caracas, extracted Maduro and his wife from a fortified military compound, and flew them to New York to face narco-terrorism charges. The whole thing took less than 30 minutes.

Key facts:

Maduro is in U.S. custody, facing a newly unsealed indictment

Vice President Delcy Rodríguez was sworn in as interim leader by Venezuela’s supreme court

Trump stated the U.S. will “run the country” until a “safe, proper, and judicious transition”

No congressional authorization was obtained; Democrats are forcing a war powers vote

China and Russia have condemned the action; UN Security Council meets Monday

The immediate market reaction? Muted. Brent closed Friday at $60.75, and analysts expect only a $1-2 bump when futures open Sunday night.

So why are the markets so calm? Because Venezuela barely matters to current oil supply and the markets know it.

Baseline: Venezuela’s Irrelevance (For Now)

Here’s the disconnect that makes this situation interesting:

VENEZUELA BASELINE METRICS

═══════════════════════════════════════════════════════════════

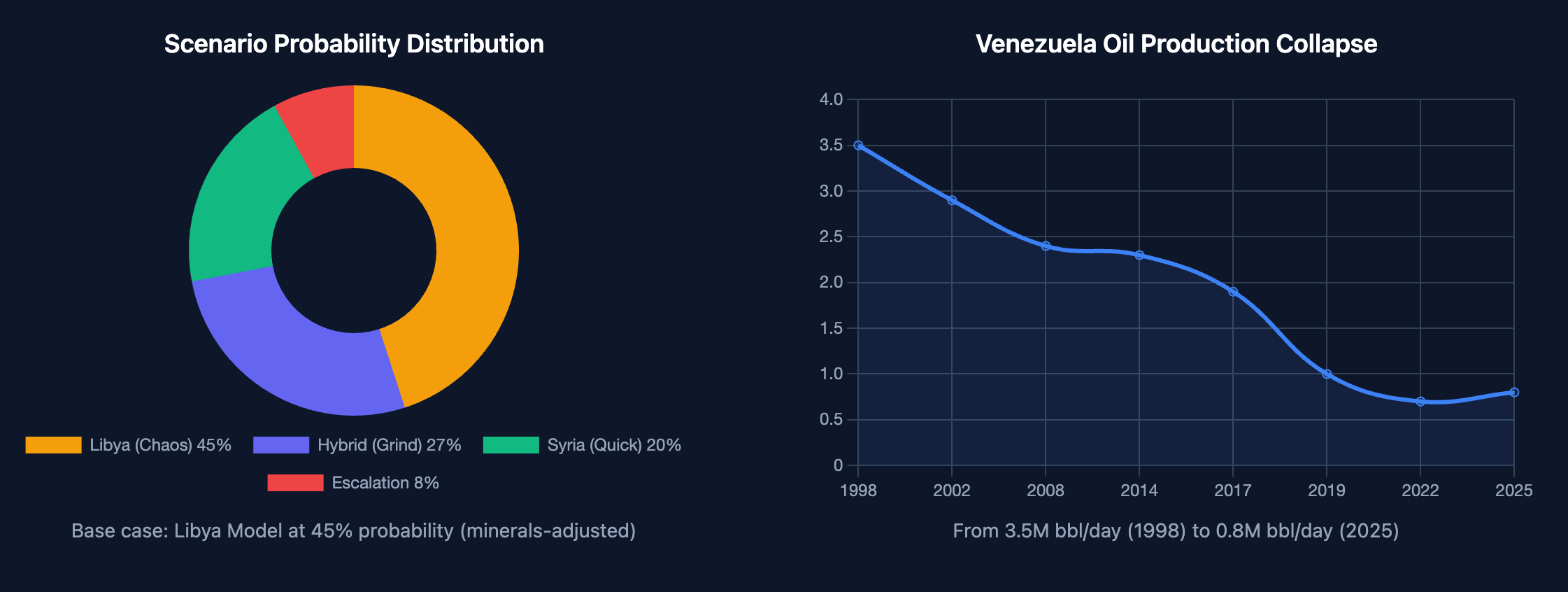

Current Production ~800K bbl/day Down from 3.5M peak (1990s)

Share of Global <1% Noise, not signal

Exports ~500K bbl/day 80% goes to China

Proven Reserves 303B barrels LARGEST IN WORLD (17% global)

Infrastructure Cost $8B minimum $100B+ for full potential

Timeline 5-10+ years Per Rice University experts

═══════════════════════════════════════════════════════════════

Venezuela is sitting on more oil than Saudi Arabia—and producing less than 1% of global supply. The reserves are real. The production capacity is destroyed.

PDVSA’s pipelines are 50+ years old. The technical expertise left when Chávez nationalized the industry. Chevron is the only major U.S. company still operating there, producing about 25% of current Venezuelan output.

First principle: Reserves ≠ supply. The market may price optionality quickly, but physical flow impact takes quarters or years.

The Hidden Story: Critical Minerals and Rare Earths

Here’s what the oil-focused headlines are missing: Venezuela isn’t just an oil story.

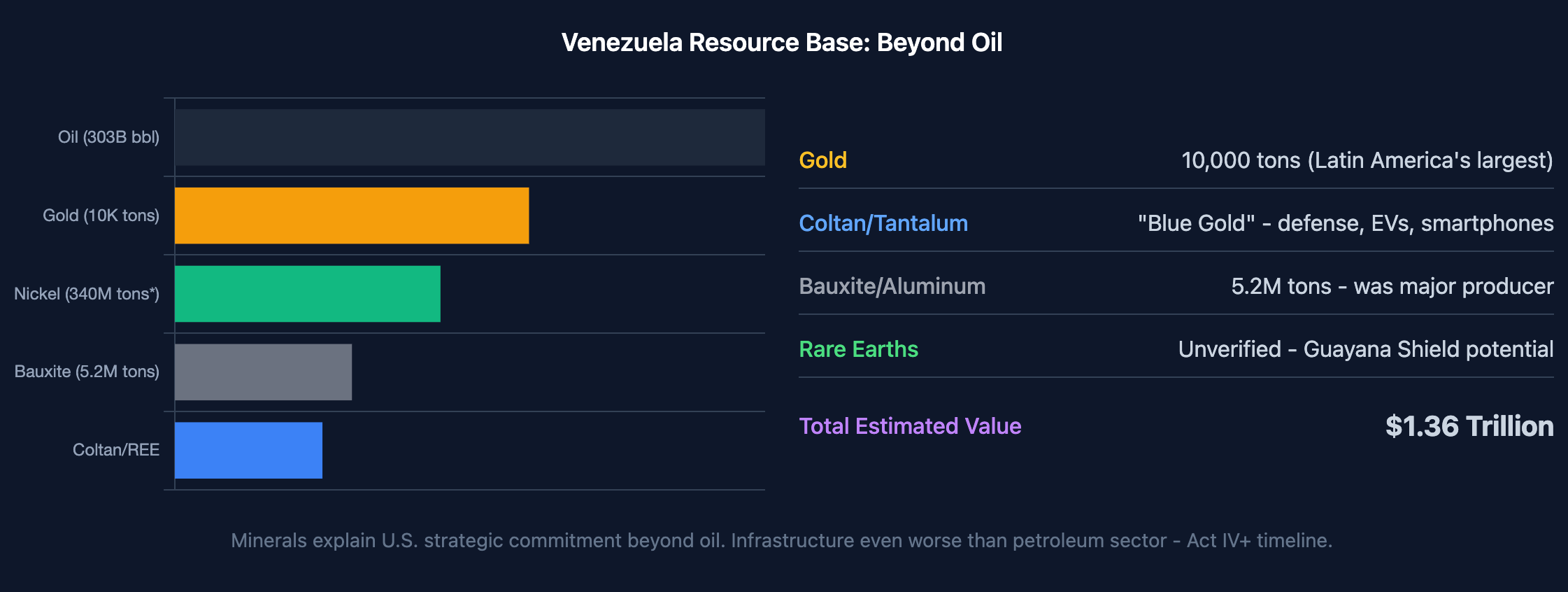

VENEZUELA MINERAL ENDOWMENT (Beyond Oil)

═══════════════════════════════════════════════════════════════════

Mineral Status Strategic Importance

───────────────────────────────────────────────────────────────────

Gold 10,000 tons Latin America's largest

exploitable reserves

Coltan (Nb-Ta) "Blue gold" — Capacitors, electronics,

major deposits defense systems, EVs

in Guayana Shield

Bauxite/Aluminum 5.2M tons, Structural, electronics

was major producer manufacturing

Iron Ore World-class Steel production

Guayana Shield

Nickel 340M tons claimed Battery metals for EVs

(unverified)

Rare Earths Reported in Magnets, defense,

Guayana Shield clean energy

(not commercially

proven)

───────────────────────────────────────────────────────────────────

Total estimated value: $1.36 trillion (per Maduro government)

═══════════════════════════════════════════════════════════════════

Chávez called coltan Venezuela’s “blue gold” back in 2009. It’s a critical input for capacitors used in smartphones, EVs, and missile guidance systems. The Orinoco Mining Arc—a 112,000 km² zone in southern Venezuela—contains most of these deposits.

The problem: Like oil, the mining sector has collapsed. Most extraction is informal or outright illegal, controlled by criminal networks and guerrillas (including Colombia’s ELN). China has been the primary buyer through shadow supply chains.

Why this matters for the thesis:

U.S. strategic interest is broader than oil. Critical minerals are a bipartisan national security priority. This increases political will for sustained engagement.

China has more at stake. They’re not just losing oil imports—they’re losing access to coltan, bauxite, and gold that flow through informal networks. This raises escalation risk.

Timeline is even longer than oil. Mineral deposits are less developed, infrastructure is worse, and environmental/governance issues are severe. This is Act IV+ territory.

Additional trade expressions exist. Gold miners, aluminum producers, and critical minerals plays enter the picture.

The minerals angle arguably increases both the “Syria” scenario probability (more U.S. commitment to stability) AND the escalation risk (more Chinese strategic interest). Net effect: slightly higher variance, similar expected value.

The Macro Backdrop: Oversupply and OPEC+ Hesitation

This crisis arrives into a bearish oil market:

2025 was the worst year for oil in five years (Brent -19%, WTI -20%)

OPEC+ has been unwinding cuts, adding supply through year-end

U.S. production hit a record 13.8M bbl/day

Demand is soft (EVs, work-from-home, weak global economy)

The global market is oversupplied. That’s the structural headwind facing any bullish Venezuela thesis.

OPEC+ meets Sunday in their regular monthly session, expected to confirm a pause on production changes through Q1 2026. Their decision framework will determine whether geopolitical risk becomes a volatility event or a directional trend.

The Scenario Framework

Rather than predict headlines, I’m assigning probabilities to four distinct scenarios and calculating expected values across each. This is how we avoid anchoring on any single narrative.

Scenario 1: “Syria Model” — Quick Stabilization

Probability: 20% (up from 15% for oil-only view due to minerals strategic interest)

María Corina Machado (the opposition leader who won the 2025 Nobel Peace Prize) or another opposition coalition takes power quickly. The U.S. recognizes the new government, sanctions lift within 60-90 days, Chevron expands immediately, other majors signal return, and colectivos/paramilitaries stand down.

Oil Impact:

Short-term: Flat to slightly bearish (market prices future supply)

Medium-term: Bearish (production ramps to 1.5-2M bbl/day)

Long-term: Structurally bearish (potential 3M+ bbl/day)

Historical analogue: Syria post-Assad, where a fragmented opposition consolidated faster than expected.

Scenario 2: “Libya Model” — Prolonged Instability

Probability: 45% (down from 50% for oil-only view —minerals interest may increase U.S. commitment)

This is the base case. Multiple factions vie for power—Machado’s movement, Chavista remnants, military elements, the colectivos (armed pro-government gangs), and potentially the ELN (Colombian guerrillas operating in western Venezuela). PDVSA operations get disrupted, some wells shut in, foreign investment stays on the sidelines for years.

Oil Impact:

Short-term: Modestly bullish (+$2-5 risk premium)

Medium-term: Bullish support (production falls to 500-700K bbl/day)

Long-term: Neutral (production frozen at low levels)

Historical analogue: Libya post-Gaddafi, where a decade later the country still hasn’t stabilized and production remains a fraction of potential.

Scenario 3: “Hybrid Model” — Slow Grind

Probability: 27% (slight adjustment for rebalancing)

Chevron’s operations stay protected but expansion is slow. Sanctions partially lift but legal/commercial uncertainty persists. Production stays flat at ~1M bbl/day for 2-3 years, with gradual stabilization eventually enabling investment.

Oil Impact:

Short-term: Minimal (status quo preserved)

Medium-term: Neutral to slightly bearish

Long-term: Bearish as production eventually grows

Historical analogue: Iraq in the 2000s—slow, grinding progress with constant setbacks.

Scenario 4: “Escalation Model” — Regional Conflict

Probability: 8% (up from 5% for oil-only view — China has more at stake than just oil)

Russia or China provides material support to Chavista loyalists. A proxy conflict develops. The U.S. commits more military resources. Regional refugee crisis destabilizes Colombia and Brazil. Cuba—which relies on Venezuelan oil—faces acute shortages and potential political crisis.

Oil Impact:

Short-term: Sharply bullish (+$10-20 risk premium spike)

Medium-term: Highly volatile, elevated baseline

Long-term: Structurally higher if conflict spreads

Historical analogue: No clean precedent. Closest might be the Cold War proxy conflicts in Latin America, but with modern great-power resource competition layered on top.

A Note on Probabilities

My above probabilities are subjective estimates based on pattern-matching, not a rigorous quantitative model. I should be transparent about that.

Back when I was in consulting, we’d call it “Independent <Firm> Analysis” 😒

What informed the estimates:

Libya at 45-50% — Historical base rate. Post-regime-change instability is the modal outcome in oil states (Libya, Iraq, Syria). My preliminary research showed analysts like Jorge León at Rystad explicitly saying Venezuela is “likely to look more like post-Gaddafi Libya” due to remaining Chavismo support and multiple opposition claimants. I adjusted this down given mineral and mining interests.

Hybrid at 27-30% — The “muddle through” scenario. Chevron’s protected status suggests some baseline continuity is possible. This is essentially “Libya but less bad.” Lowered this slightly based on other scenarios.

Syria at 15-20% — The optimistic case. Quick stabilization is rare but not impossible (Syria post-Assad moved faster than expected). Machado has 72% approval per polling cited in search results, but Trump explicitly said she “doesn’t have the support” — mixed signals reduce probability. Minerals and mining change this to 20%.

Escalation at 5-8% — Tail risk. China/Russia condemned the action but their response was muted. Beijing didn’t press the issue in December meetings. Low probability but non-zero given the precedent-setting nature of the operation. I increased the probability slightly given China’s mineral interests.

So to be transparent, these are educated guesses, not derived probabilities.

A few ways to make them more rigorous:

Prediction market calibration — Check Polymarket/Metaculus if they have Venezuela outcomes

Base rate analysis — Systematic study of post-intervention outcomes (N is small though)

Expert elicitation — Survey Latin America specialists, weight by track record

Indicator-based updating — Define specific observables that shift probabilities (I did this in the triggers section, but the starting points are still subjective)

Expected Value Calculation

Here’s the math (updated for minerals-adjusted probabilities):

EXPECTED VALUE BY SCENARIO (6-Month Horizon)

═══════════════════════════════════════════════════════════════

Scenario Prob Brent Move EV Contribution

───────────────────────────────────────────────────────────────

Syria (Quick) 20% -$5 -$1.00

Libya (Chaos) 45% +$6 +$2.70

Hybrid (Grind) 27% +$1 +$0.27

Escalation 8% +$20 +$1.60

───────────────────────────────────────────────────────────────

WEIGHTED EV +$3.57

═══════════════════════════════════════════════════════════════

A $3.57 expected move on a $60.75 base is about 6% upside. That sounds tradeable—until you look at the variance.

Variance Analysis:

Standard deviation of outcomes: ~$5.43

Sharpe-like ratio: 0.65

That’s not a high-conviction directional trade. The dispersion across scenarios is too wide. You’re not getting paid enough for the uncertainty.

This is the key insight: The edge isn’t in predicting oil direction. It’s in:

Owning volatility when it’s underpriced

Positioning in sectors that win across multiple scenarios

Avoiding the “oil goes up” trap that ignores the oversupply backdrop

The Heavy Crude Wrinkle

Venezuela produces Merey—a heavy, sour crude that’s critical for specific refining applications:

Diesel production

Jet fuel

Asphalt

Industrial fuels

This crude type is not easily substituted. Light, sweet crude (what the U.S. produces) makes gasoline, but you can’t just swap it in for heavy crude applications. If Venezuelan supply tightens, heavy sour crude commands a premium—and that premium flows directly to Gulf Coast refiners configured to process it.

Expected heavy crude spread widening: +$2.40/bbl (probability-weighted)

This is a more targeted opportunity than the broad oil direction bet.

What’s Next

In Part 2, I’ll map specific companies and sectors to these scenarios — Chevron’s first-mover advantage, the oil services rehabilitation trade (SLB/BKR), the refiner arbitrage, and claims optionality (ConocoPhillips, ExxonMobil). We’ll build a winners/losers matrix across all four scenarios.

In Part 3, we get into implementation: specific option structures, position sizing, and how to express these views with defined risk.

In Part 4, the decision framework — what triggers cause us to update probabilities, how OPEC+ decisions shift the regime, and an operational playbook for the next 6-18 months.

Key Takeaways (Part 1)

Venezuela is irrelevant to current oil supply but sits on transformational reserves

The minerals story is underappreciated — $1.36T in gold, coltan, bauxite, rare earths

The market is oversupplied — bullish oil spikes tend to fade without physical disruption

Libya scenario (prolonged chaos) is the base case at 45% probability

Expected oil move is +$3.57 but variance is high (Sharpe ~0.65)

The edge isn’t directional oil — it’s volatility, relative value, and heavy crude spreads

Minerals increase both U.S. commitment AND China’s stakes — net effect is higher variance

Policy clues can guide opportunity — Closely monitoring Trump’s advisors and inner circle for directional trades could prove helpful

Ultimately, the chess trade isn’t predicting the next headline. It’s identifying which phase we’re in and holding the correct exposures.

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

These posts are about methodology, not recommendations. Some of the approaches discussed here involve commodities (like oil) and complex instruments (e.g., options and derivatives) and not suitable for all investors. Many of my analyses probably contain errors — if you find them, please let me know.

While I may hold positions in some of the underlying assets discussed here, my posts are not an endorsement or a recommendation of those underlying assets. This is a quickly emerging and fast-changing situation, so please be wary of information staleness.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.