The SaaSpocalypse: Anatomy of a Sector Re-Rating

Part 75 — SaaS Series Part 1 of 4

This is part 75 of my series — Building & Scaling Algorithmic Trading Strategies

This week, approximately $300 billion in market capitalization evaporated from software stocks in 48 hours. Jefferies traders coined it the “SaaSpocalypse.” The iShares Expanded Tech-Software Sector ETF (IGV) has fallen ~28% from its 52-week high and is down roughly 20% year-to-date. Thomson Reuters dropped 16% in a single session. LegalZoom plummeted 20%.

The catalyst was a confluence of events: Anthropic released Claude for Work (a productivity tool for in-house lawyers), Palantir’s Q4 earnings included a thesis that AI isn’t augmenting enterprise software — it’s replacing it — and Microsoft reported slowing cloud growth amid surging AI capex. The market, already nervous, reached for the exits.

As a Palantir customer put it on their earnings call: “We’ve gone all-in so much so that every other software must justify its existence, and so far they haven’t been able to.”

That single sentence encapsulates the fear now priced into every SaaS stock — so let’s unpack that.

This is the first of a four-part series on SaaS that I have been working on. I’ll attempt to dissect what’s actually happening in the SaaS sector, build a quantitative framework for identifying value in the wreckage, propose a few testable hypotheses, and ultimately construct a multi-decision trading strategy that we can test.

So let’s start with what the data actually shows.

The Structural Picture: Growth Deceleration Was Already Here

The AI disruption narrative is dramatic, but it’s layered on top of a trend that’s been compounding for three years: SaaS revenue growth has been in secular decline.

By Q4 2025, median revenue growth for public SaaS companies fell to 12.2%, down from 17% in Q1 2024, and well below the 25-30% rates that defined the sector pre-COVID. Aventis Advisors forecasts further deceleration through at least Q2 2026.

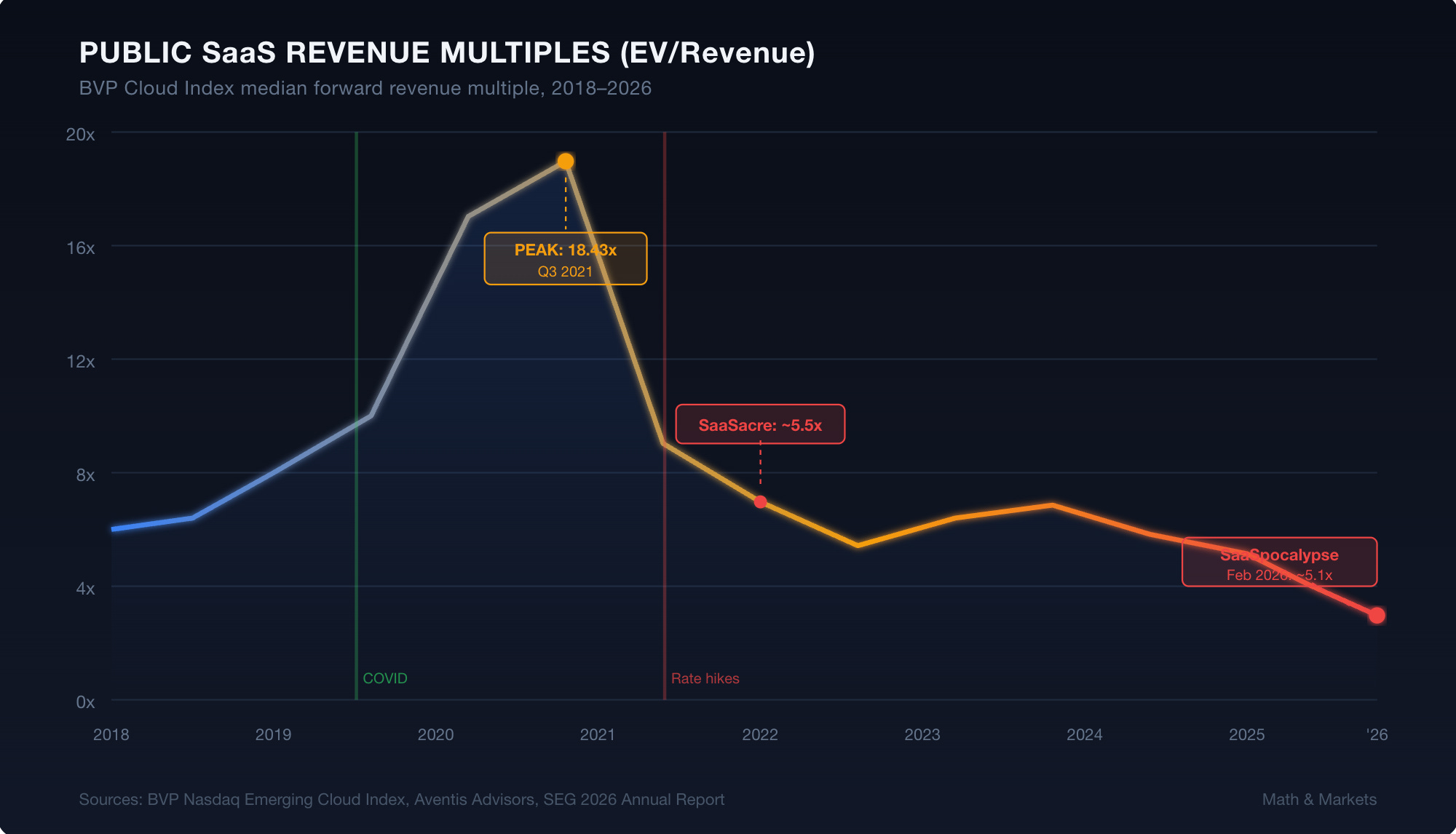

Meanwhile, the BVP Nasdaq Emerging Cloud Index (EMCLOUD) — the purest proxy for SaaS public equity performance — ended Q1 2025 at a forward revenue multiple of 6.26x. This is down from 6.86x at year-end 2024, and remains dramatically below the 2021 peak of 18.43x. Since Q2 2022, public SaaS valuations have been stuck in a single-digit range. They never recovered.

The math here matters. If you decompose SaaS stock returns into three drivers — revenue growth, margin expansion, and multiple expansion — the story becomes clear:

Revenue growth: Decelerating toward 12%, heading lower

Margin expansion: Real, but largely captured (median EBITDA margins improved significantly post-2022)

Multiple expansion: Dead. Multiples have compressed 65%+ from peak and show no signs of reverting

Now, some of this is driven by other factors — e.g., move away from seat-based pricing to consumption-based pricing. Even so, the numbers are the numbers — revenue is taking a hit and churn is increasing.

When your sector’s primary return driver (growth → multiple expansion) is structurally impaired, you need a different playbook. In my view, that’s what the AI disruption narrative just made explicit.

The Two-Tier Market: Dispersion Is the Story

The aggregate numbers mask a critical detail. The SEG 2026 Annual SaaS Report found that while the broader SaaS index declined in 2025, the top quartile of companies delivered approximately 6% YoY gains. The winners were tied to mission-critical workflows, data infrastructure, and AI enablement. Analytics & Data Management was the only product category to expand its EV/TTM revenue multiple, up 11%.

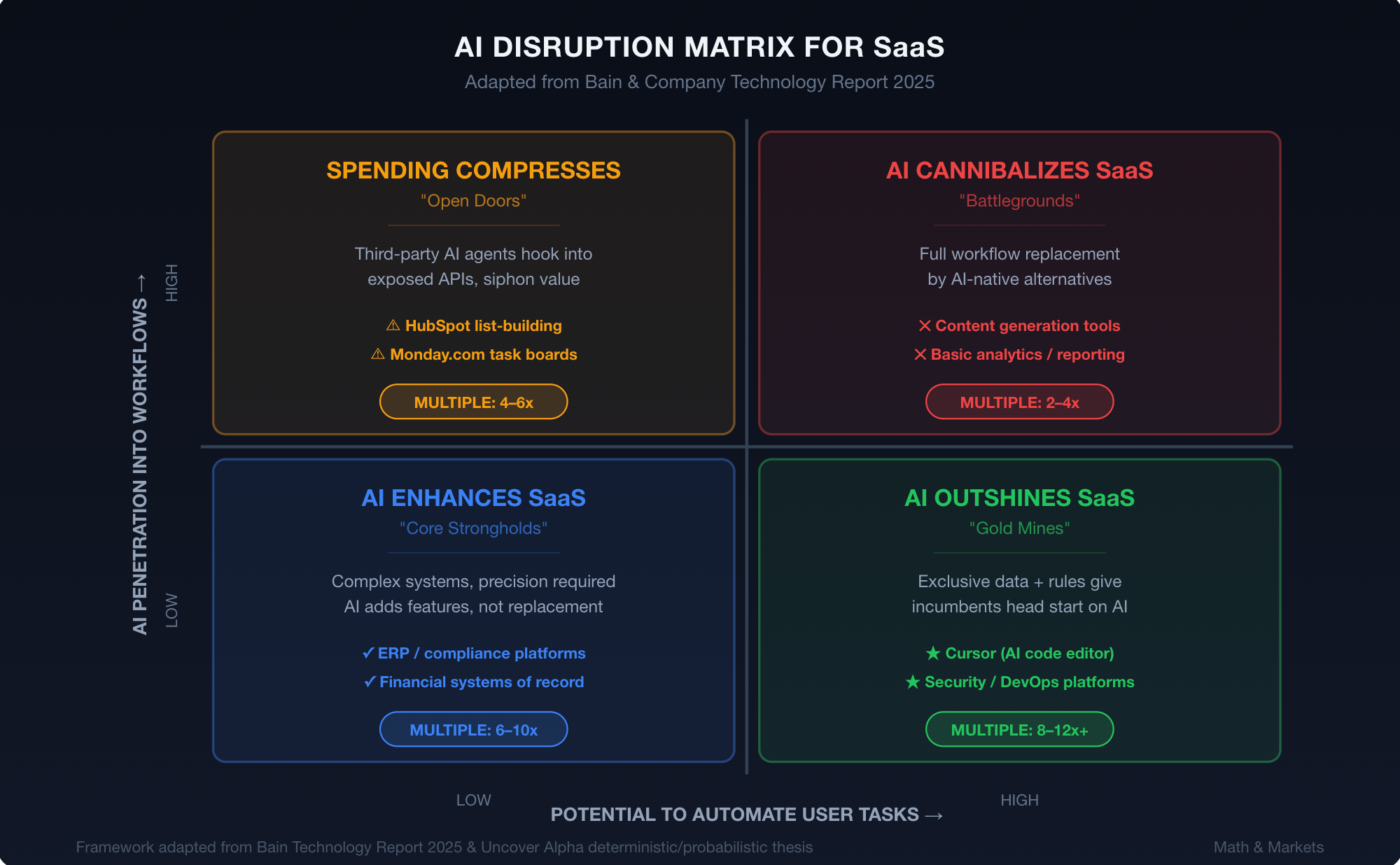

This dispersion is not random. It follows a pattern that Bain & Company discusses in their publication, Will Agentic AI Disrupt SaaS? They present this as a 2×2 matrix of AI disruption risk, mapped along two axes: (1) potential for AI to automate SaaS user tasks, and (2) potential for AI to penetrate SaaS workflows. The four quadrants produce very different outcomes:

AI enhances SaaS (low automation, low penetration): The status quo holds. Think complex ERP systems, compliance platforms. These are “core strongholds.”

Spending compresses (low automation, high penetration): Third-party AI agents hook into exposed APIs and siphon value. HubSpot’s list building, Monday.com’s task boards. These are “open doors.”

AI outshines SaaS (high automation, low penetration): Incumbents hold exclusive data and rules, giving them a head start on full automation. Cursor’s code editor, Guidewire’s claims processing. These are “gold mines.”

AI cannibalizes SaaS (high automation, high penetration): The nightmare scenario. Content generation, basic analytics, template-driven workflows. These are “battlegrounds.”

The Substack blog Uncover Alpha proposed a complementary framework that I find useful: the distinction between deterministic and probabilistic systems.

Deterministic systems — where precision is critical, state management is complex, and errors cascade — are defensible. ERP, financial reconciliation, compliance audit trails. Probabilistic systems — content generation, summarization, lead scoring — are existentially exposed.

As of December 2025, the median EV/Revenue multiple for public SaaS stands at 5.1x. But this is a bimodal distribution masquerading as a single number. Deterministic-system SaaS is still trading at 8-12x. Probabilistic-system SaaS has collapsed to 2-4x. The market hasn’t fully priced in this distinction yet, which creates opportunity.

The AI Disruption Paradox

Bank of America published a note this week calling the selloff “an indiscriminate selloff” that resembles the DeepSeek panic of January 2025. Their argument was elegant: the SaaS selloff relies on two mutually exclusive scenarios occurring simultaneously — (1) AI capex deteriorating to the point of weak ROI and unsustainable growth, while (2) AI adoption being so pervasive that it obsoletes long-standing software workflows.

Both cannot be true at the same time. If AI is powerful enough to disrupt established industries, the infrastructure spending supporting it cannot collapse.

This is a genuinely important logical observation, but I think it misses the nuance. The market isn’t pricing a single coherent scenario — it’s pricing uncertainty across a distribution of outcomes. When you can’t bound the downside, you de-risk first and ask questions later. That’s rational behavior under Knightian uncertainty, and it’s exactly what “get me out” selling looks like.

The counter-argument from bears is more empirical: several enterprise CIOs have publicly stated they’re redirecting IT budgets from traditional software licenses toward AI-native solutions. Publicis Sapient reports reducing traditional SaaS licenses by approximately 50%, including major platforms like Adobe, by substituting generative AI tools. Apollo cut its direct lending funds’ software exposure nearly in half during 2025.

These are data points, not conclusions. But they’re data points that point in one direction.

What the M&A Market Tells Us

Private markets provide a useful reality check. SaaS M&A activity reached a record high of 2,698 transactions in 2025, a 28% YoY increase. AI-referenced targets accounted for approximately 72% of all SaaS M&A transactions. Private equity buyers were involved in 58% of deals.

This tells us something important: strategic and financial buyers — people spending real money on real diligence — are not abandoning SaaS. They’re selectively buying at what they perceive to be attractive prices. Record M&A volume in a sector that public markets are treating as structurally impaired is a divergence worth paying attention to.

Private SaaS revenue multiples stabilized around 16.11x in Q1 2025, which actually aligns more closely with the top quartile of public SaaS companies (13.80x) than with the overall public median (~6x). This suggests private buyers are paying up for quality, while public markets are applying a blanket discount.

Median private M&A multiples over the 2015-2025 period ran at 4.5x EV/Revenue, with the top quartile above 8.1x. We’re now entering a period where some high-quality public SaaS names are trading at or below long-run private M&A medians. That’s unusual.

The Macro Overlay

And now let’s not ignore the macro. Gartner’s Q3 2025 forecast projects global software spending will hit $1.43 trillion in 2026, a 15.2% increase driven by AI-enabled applications. The cloud computing market is projected to reach $905 billion by year-end 2026. The SaaS market specifically is expected to reach $512 billion, with an 18.7% CAGR through 2030.

These are big, growing numbers. The sector isn’t dying. It’s repricing. And the repricing reflects not demand destruction, but margin and pricing power compression — a shift from “growth at any cost” to “justify your existence per dollar of value delivered.”

That shift is permanent. It’s also — for investors with the right framework — an opportunity.

What’s Next

In Part 2, I’ll build a quantitative framework for identifying value in SaaS using factor models adapted for the sector’s unique characteristics. The Fama-French five-factor model breaks down in interesting ways when applied to software: book value is largely meaningless, the profitability factor (RMW) becomes the dominant signal, and traditional value metrics need to be reconstructed around Rule of 40, NRR, and CAC payback.

In Part 3, I’ll propose three specific, testable value hypotheses for the current environment.

In Part 4, I’ll structure a multi-decision trading strategy that accounts for regime uncertainty, the AI disruption distribution, and the behavioral dynamics of capitulation selling.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

I have no current positions in the names discussed. Do your own work.