The First Cross-Asset Indicators I’m Prototyping (and How They’ll Fit Into the Allocator)

Part 11 below talks about operationalizing the initial cross-asset indicators

This is part 11 of my series — Building & Scaling Algorithmic Trading Strategies

In the last post I wrote about the longer-term goal: turning the allocator into a multi-dimensional system that actually understands the world beyond equities. But before I start wiring in full volatility surfaces, credit curves, and Bayesian regime engines, I need to keep things tight and manageable.

So this post is about the first batch of cross-asset indicators I actually plan to try in the near term — nothing crazy, nothing requiring a research team of 12 quants. Just the highest-leverage signals that big allocators care about, but in a version I can run daily without melting my CPU.

The goal isn’t to nail every macro nuance but rather to give the allocator a better sense of when to chill out and when the coast is clear.

So let’s get into it!

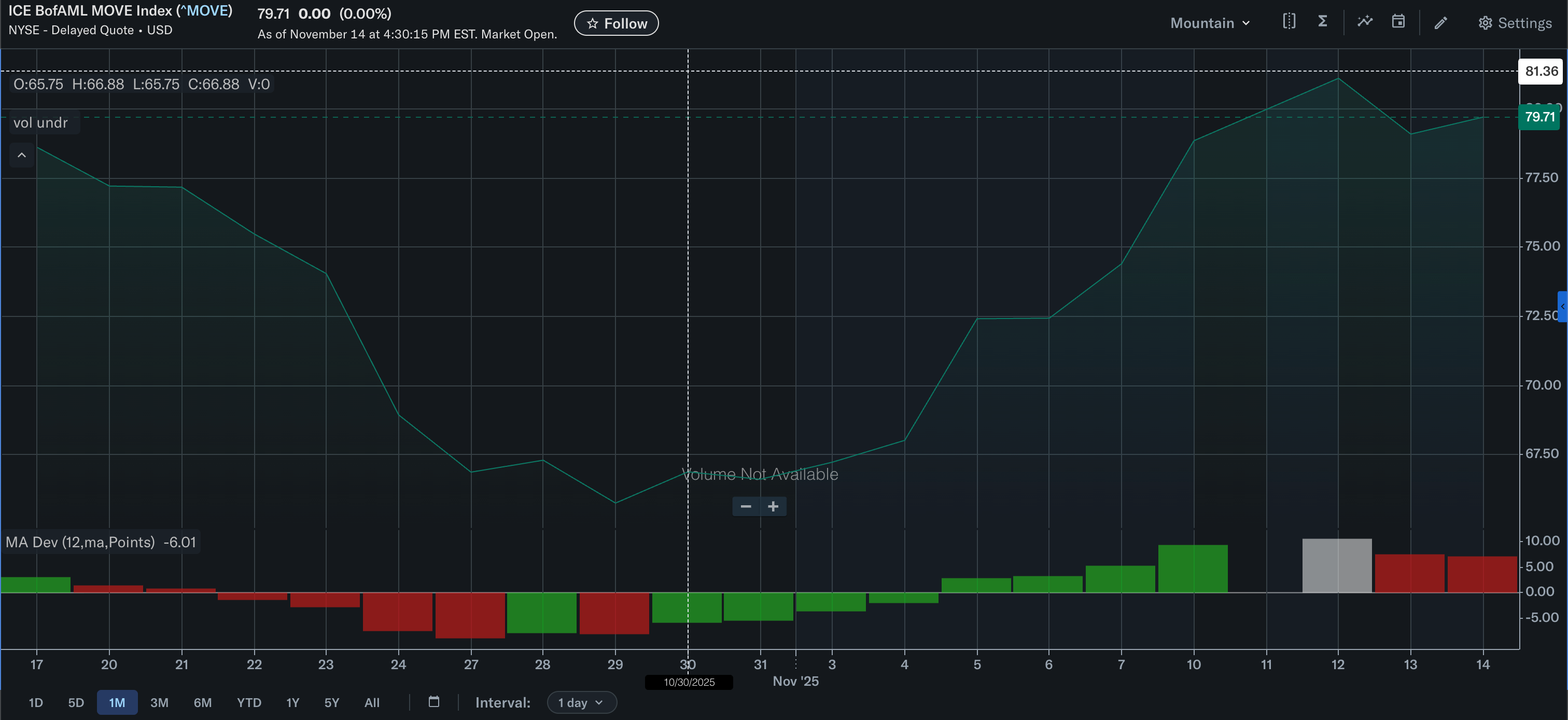

1. MOVE (Bond Volatility) – The “Global Risk Thermometer”

If I had to pick one cross-asset input to start with, it’s MOVE, the bond-market’s equivalent of VIX.

Why it matters:

Rates volatility leads equity volatility most of the time.

Big equity drawdowns often start with bond-market stress.

Trend signals behave badly when MOVE is rising sharply.

What I’ll do with it:

Track MOVE’s rate of change (ROC).

Create a simple “MOVE danger zone” that reduces allocator size.

Use it to override long exposure during false breakouts.

This is the cleanest signal that something is “off” in the plumbing.

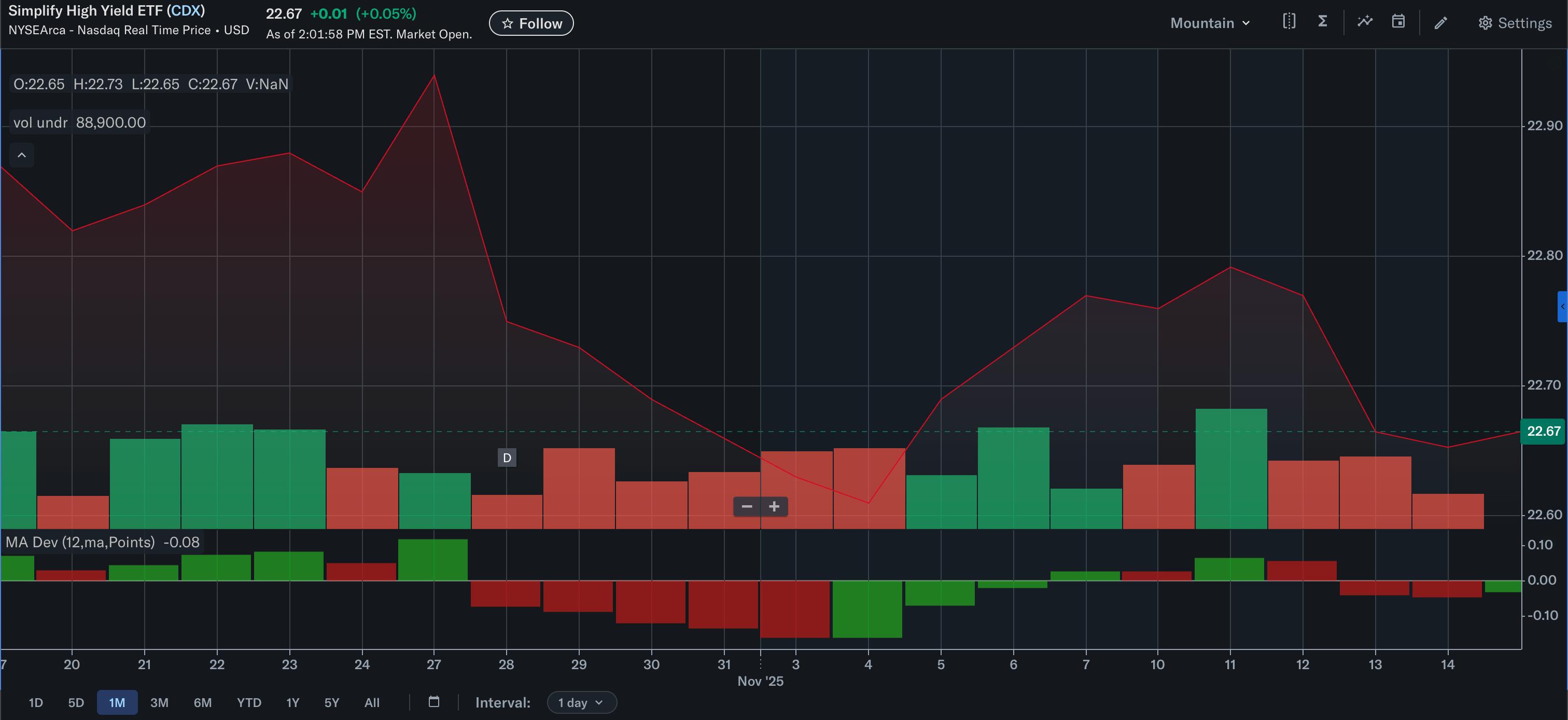

2. Credit Spreads (CDX IG / HY) – The “Risk Appetite” Meter

In my experience, credit is where real risk shows up first. If credit cracks, equities follow — sometimes days, sometimes weeks, and sometimes months later.

Why it matters:

Credit spread widening = risk premium expanding.

Credit is a better predictor of equity drawdowns than equities themselves.

Stable/tight spreads = allocator can trust trend signals.

What I’ll do with it:

Track daily changes in IG and HY spreads.

Add a “credit stress” flag: rising spreads shrink allocator leverage.

Possibly blend IG/HY ROC into a single macro-stress index later.

This won’t be a timing model — just a sanity check on the allocator.

3. FX Volatility (JPY, EUR, GBP, EM) – The “Global Funding Pulse”

FX volatility spikes often precede global deleveraging. The yen, in particular, is like a seismograph for stress.

Why it matters:

FX vol tends to spike before equities.

JPY crosses are tightly linked to carry, funding, and global liquidity.

FX turmoil has a habit of leaking into everything else.

What I’ll do with it:

Track a simple FX-vol composite (JPY + EUR + GB + EM).

If FX vol spikes while equity trend looks fine → allocator sizes down.

If FX vol is quiet → trend signals get more trust.

It’s a low-cost way to detect “macro weirdness” early.

4. Commodity Volatility (OVX + GVZ) – The “Shock Detector”

Energy and gold volatility spikes are usually telling you something about either supply shocks or flight-to-safety.

Why it matters:

OVX spikes often precede broader risk aversion.

Gold volatility reacts when real yields or macro confidence shifts.

Commodity vol is structurally independent from equity vol.

What I’ll do with it:

Combine OVX + GVZ into a commodity-vol meter.

Use only the rate of change — I don’t care about absolute levels.

Add it as a low-weight input into the allocator’s sizing logic.

It’s not a “core” input, but a nice canary in the coal mine.

5. A Simple Macro Stress Score (the lightweight version)

Once all the above are in place, I’ll create a macro stress score:

1 if MOVE > threshold

1 if credit spreads up > threshold

1 if FX vol spikes

1 if commodity vol spikes

Score = 0 → allocator behaves normally

Score = 1–2 → allocator dials back leverage

Score = 3–4 → allocator enters “defensive mode”

My goal is to keep it super simple — no fancy weighting, no optimization.

It’s just a “don’t be stupid” guardrail.

6. How This Will Fit Into the Allocator (Without Breaking It)

This is an important consideration as I explore this — I’m not rebuilding the allocator around macro. Rather, I’m adding these signals as context, not commands.

The allocator still trades based on:

trend

velocity

acceleration

volatility regime

alpha sleeve behavior

The macro inputs act like:

sanity checks

sizing modifiers

drawdown preventers

confirmation/doubt mechanisms

They won’t flip signals, they won’t replace trend, and they won’t create new trading rules. They’ll just help the allocator avoid sizing up at the wrong time.

7. Why I’m Starting with These (and Not the Fancy Stuff Yet)

If you can’t tell, I am a math nerd and I am really tempted to jump straight into some really cool, sexy stuff like:

Heston vol surfaces

high-frequency realized vol

hidden Markov models

flow-of-funds inference

correlation matrices

Bayesian regime engines

…but that would be like bolting an F1 engine onto a skateboard.

So before I start adding complexity for its own sake, I need:

stable live behavior

predictable allocator sizing

consistent logs

more data on how the vol sleeve behaves across regimes

clean testing infrastructure

This first set of indicators is deliberately simple.

They won’t overwhelm the system, and they’ll probably catch ~60-70% of the major macro landmines (I hope!).

8. The Roadmap (Short-Term → Long-Term)

Short-term (next few weeks):

Add MOVE, credit, FX vol, commodity vol

Create macro stress score

Wire into allocator sizing logic

Validate against live runs

Medium-term:

Add liquidity indicators

Start clustering cross-asset vol behavior

Build first prototype of multi-dimensional risk dashboard

Long-term:

Bayesian regime probability engine

Flow-based volatility signaling

Cross-asset risk decomposition

Adaptive multi-sleeve weighting

This is how the system evolves from “equity trend + vol sleeve” into a genuine, multi-dimensional allocator.

Closing

This next phase isn’t about turning my setup into a hedge fund. It’s about giving the allocator just enough awareness of the outside world so it doesn’t walk into obvious macro buzzsaws.

Small, simple, high-impact inputs but nothing fancy (yet). Just the highest-leverage cross-asset signals I can realistically integrate today.

Once those are stable, then I can get into the Bayesian stuff — which is the direction I eventually want to take the whole system — as of today anyway.

The information presented in Math & Markets is not investment or financial advice and should not be construed as such.