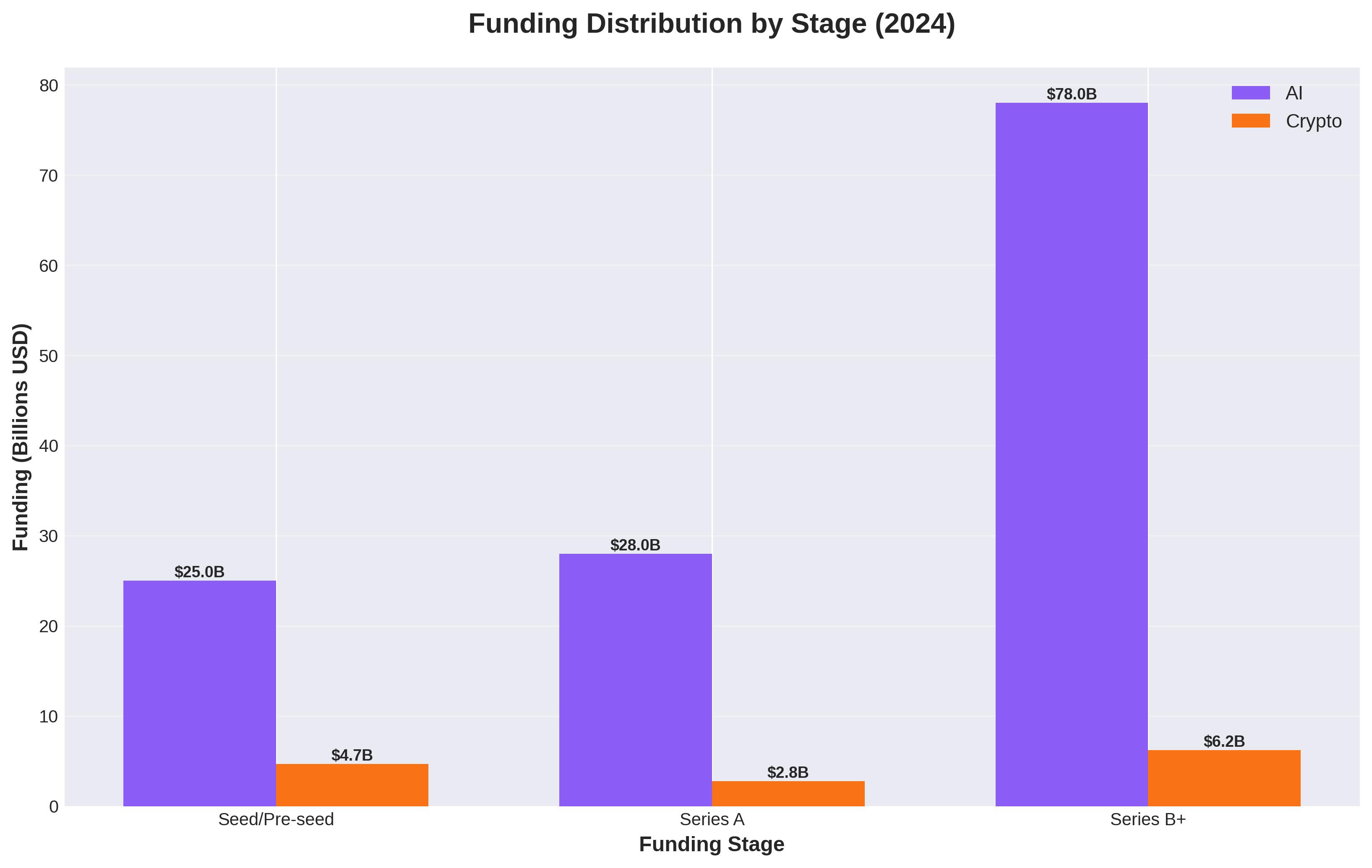

The Convergence — When AI Meets Blockchain in Financial Markets

This is a standalone piece on my perspectives on the convergence of AI & Blockchain technologies.

I’ve spent a sizable portion of my life working with banks all over the world — the United States, Canada, Australia, Western Europe, South Africa, and the Russian Federation. Whether I was consulting for banks, working for GSIBs, or payment fintechs, one truth became undeniable: technology has a huge bearing on how banks evolve and become more robust. I witnessed firsthand how things like risk management can get addressed programmatically, and the opportunities for incredible modernization that emerge when institutions embrace this reality.

The pattern is clear: banks that are tech-first adapters do fantastic. The laggards don’t just fall behind — they become obsolete.

The Institutional Advantage: When Banks Invested in Technology

The most striking examples of technology-driven advantage in finance didn’t just come from startups. They also came from institutions that made massive, early bets on proprietary technology.

Goldman Sachs Marquee represents one of the most successful technology platforms in institutional banking. What started as an internal tool evolved into a client-facing platform that democratized access to Goldman’s pricing, analytics, and risk management capabilities. Marquee isn’t just software — it’s a moat. It locks in client relationships through workflow integration and creates switching costs that competitors struggle to overcome.

BlackRock’s Aladdin might be even more impressive. Aladdin (Asset, Liability, Debt and Derivative Investment Network) powers risk analytics and portfolio management for over $25 trillion in assets. That’s not a typo. BlackRock essentially built the operating system for institutional asset management, and then licensed it to their competitors. The platform combines risk analytics, portfolio management, trading, and operations into a single system. When your competitors pay you to use your technology infrastructure, you’ve won.

These platforms share a common characteristic: they turn quantitative and risk management processes that were once manual, slow, and error-prone into systematic, fast, and scalable operations. They don’t just make existing processes faster — they enable entirely new strategies and risk frameworks that wouldn’t be possible without the technology.

The Market Structure Revolution: Speed and Information

But institutional platforms were just the beginning. The emergence of high-frequency trading (HFT) fundamentally reshaped market microstructure in ways that are still playing out today.

HFT firms didn’t just make trading faster — they systematically ate away at arbitrage opportunities that once sustained traditional market makers and proprietary trading desks. The spread between bid and ask prices compressed. Cross-exchange arbitrage windows closed. Even sophisticated statistical arbitrage strategies saw their half-lives shrink from days to minutes or seconds.

This wasn’t universally negative. Spreads tightened dramatically, benefiting all market participants. Liquidity improved in most major markets. But it created a new reality: you either invested in speed and technology, or you ceded that terrain entirely.

The retail side of this revolution came later but was no less dramatic. Robinhood and the payment-for-order-flow (PFOF) model made “zero-commission” trading economically viable by monetizing order flow in new ways. Love it or hate it, PFOF changed the retail trading landscape by eliminating the explicit friction of commissions, even as it introduced new questions about execution quality and conflicts of interest.

Private Markets: The Liquidity Frontier

Meanwhile, another transformation was happening in private markets. Companies staying private longer created a new challenge: how do you provide liquidity for firms that aren’t ready for public markets but still need mechanisms for price discovery and capital access?

Platforms like Forge Global, EquityZen, and Nasdaq Private Market emerged to address this gap. They’re creating semi-liquid markets for private company shares, allowing employees to monetize equity and investors to access pre-IPO opportunities. The technology stack required to make this work — cap table management, accreditation verification, fractional ownership, secondary trading — is sophisticated and represents a genuine innovation in market structure.

These private market platforms are essentially building parallel financial infrastructure for assets that don’t fit traditional exchange models. They’re proto-exchanges for a new asset class.

Crypto Infrastructure: Not Just Currencies

Which brings us to crypto — but not in the way most people think about it.

The real story isn’t Bitcoin’s price or Ethereum’s roadmap. It’s the infrastructure being built to make digital assets viable for institutional participants. Companies like Fireblocks are building the pipes and plumbing that make crypto operationally possible at scale.

Consider Fireblocks’ work with Solana: they’re providing institutional-grade custody, transaction signing, and risk management for blockchain networks that process hundreds of transactions per second. This isn’t about speculation — it’s about operational reliability for 24/7 markets with instant settlement.

The technology stack Fireblocks and similar providers offer — multi-party computation (MPC) for key management, policy engines for transaction approval, real-time risk monitoring — represents the maturation of crypto infrastructure. It’s the difference between a science experiment and production-ready financial infrastructure.

This matters because blockchain rails offer something traditional financial infrastructure can’t easily replicate: programmable money, composable financial primitives, and 24/7 global settlement with minimal intermediaries.

The Tale of Two Foundational Technologies

Before we dive into how AI is changing the game, it’s worth understanding the scale and dynamics of the two foundational technologies that will define this convergence: AI and blockchain.

The Investment Reality

The numbers tell a stark story:

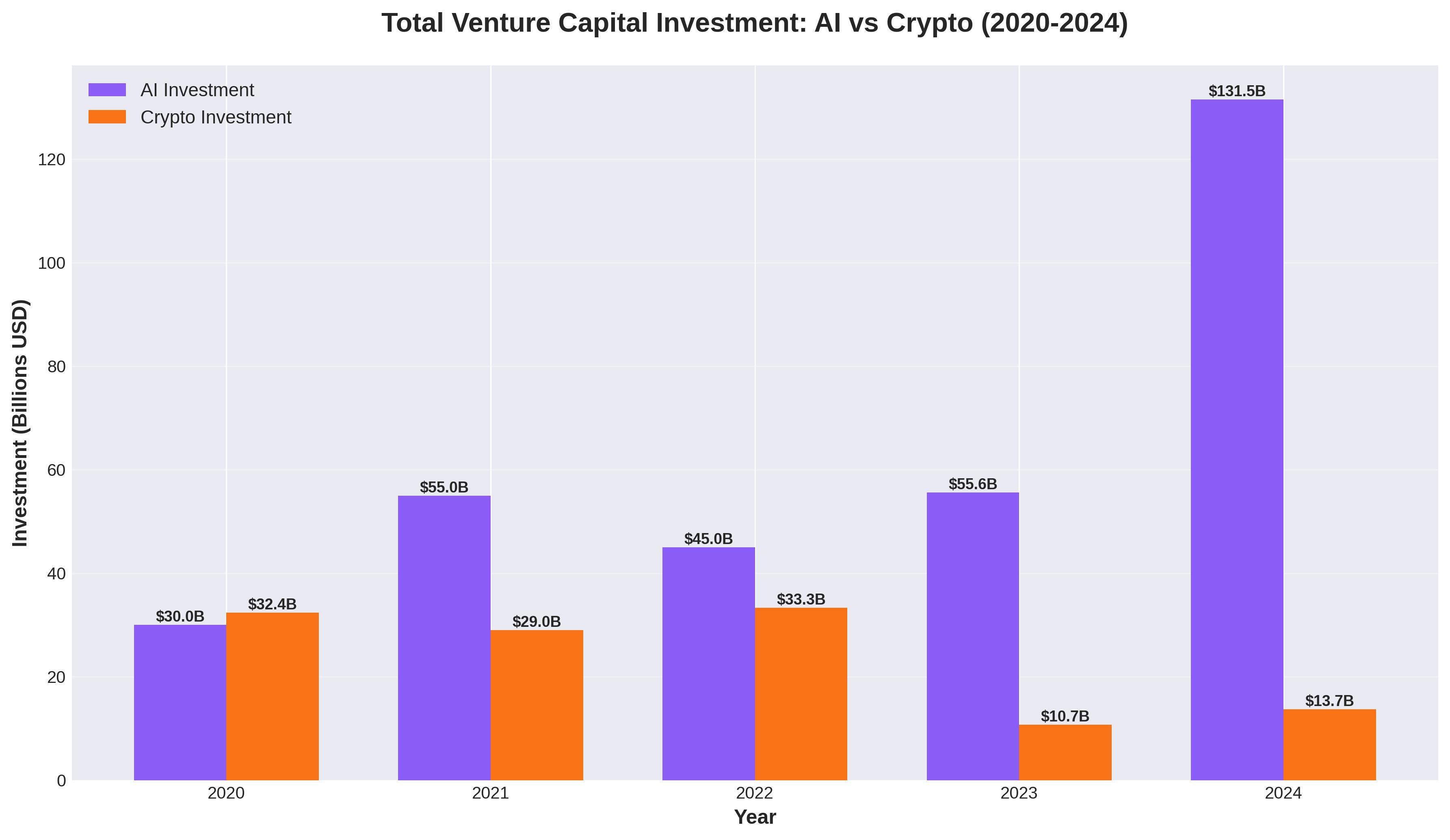

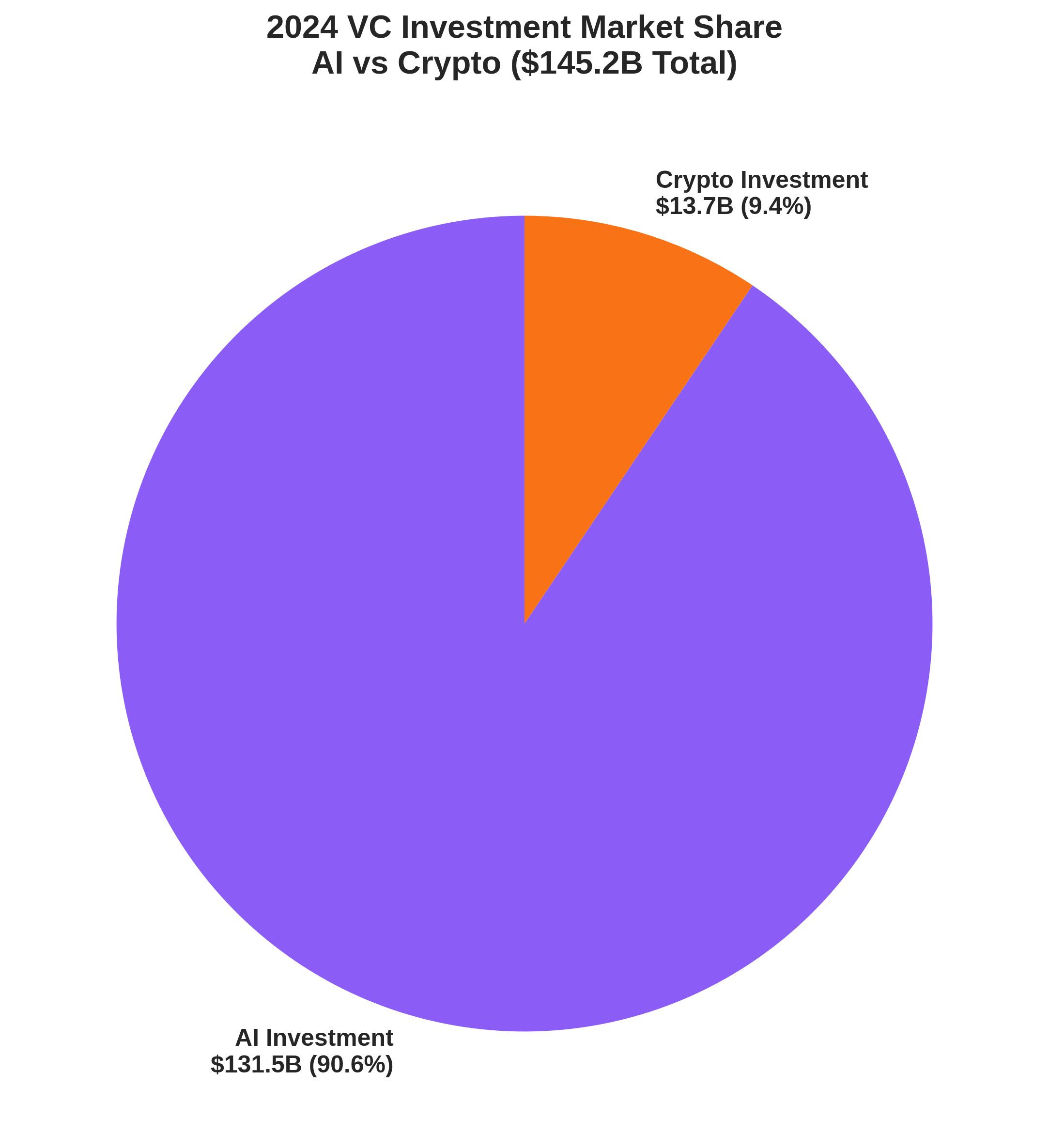

2024 Venture Capital Investment:

AI: $131.5 billion (+136% year-over-year)

Crypto: $13.7 billion (+28% year-over-year)

AI attracted 9.6x more capital than crypto in 2024. Even more striking: AI captured 33% of ALL global venture capital funding — unprecedented for any single technology sector. Crypto, despite its recovery, represents just 4.9% of global VC funding.

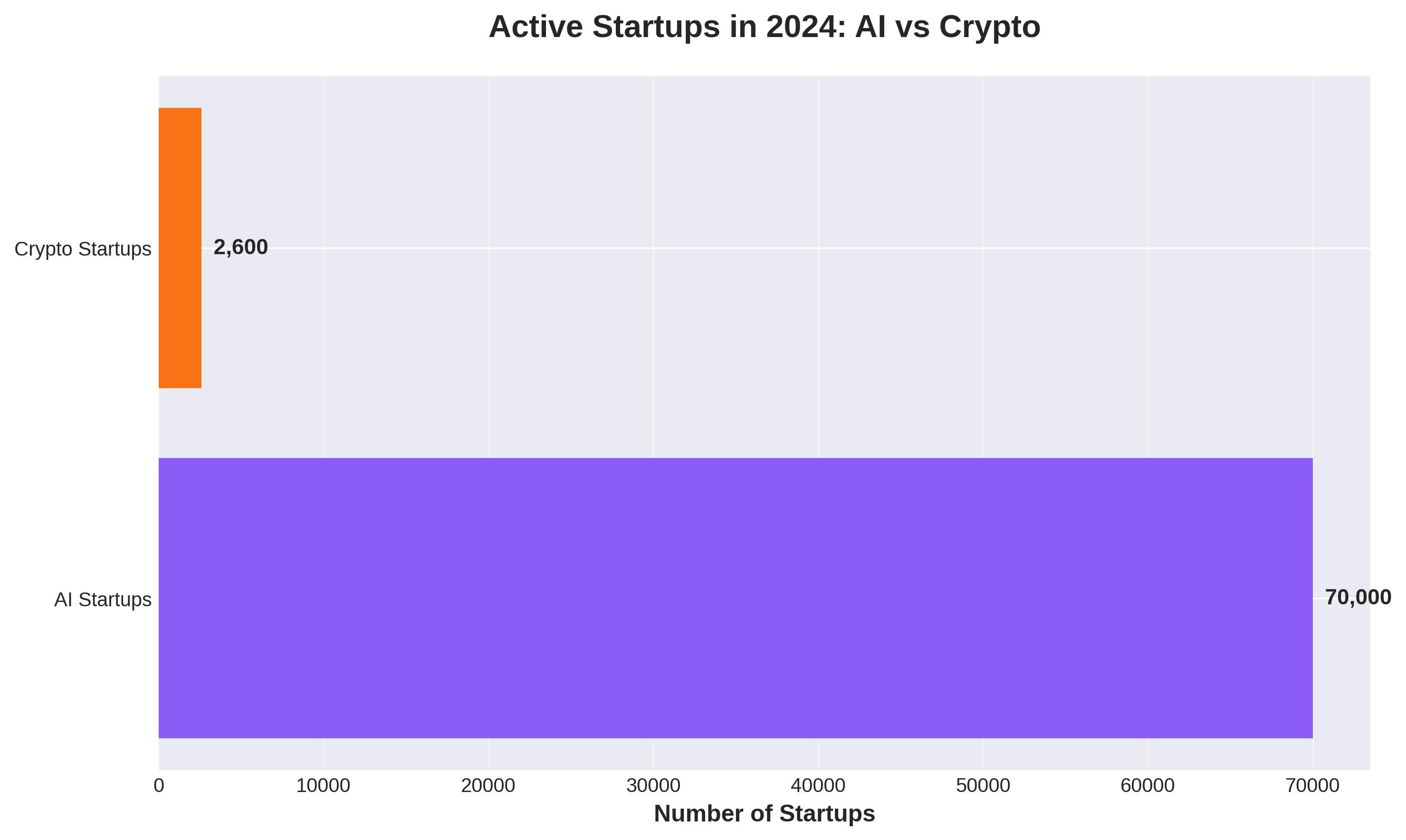

The Startup Ecosystem:

AI: ~70,000 startups globally

Crypto: ~2,600 funded startups

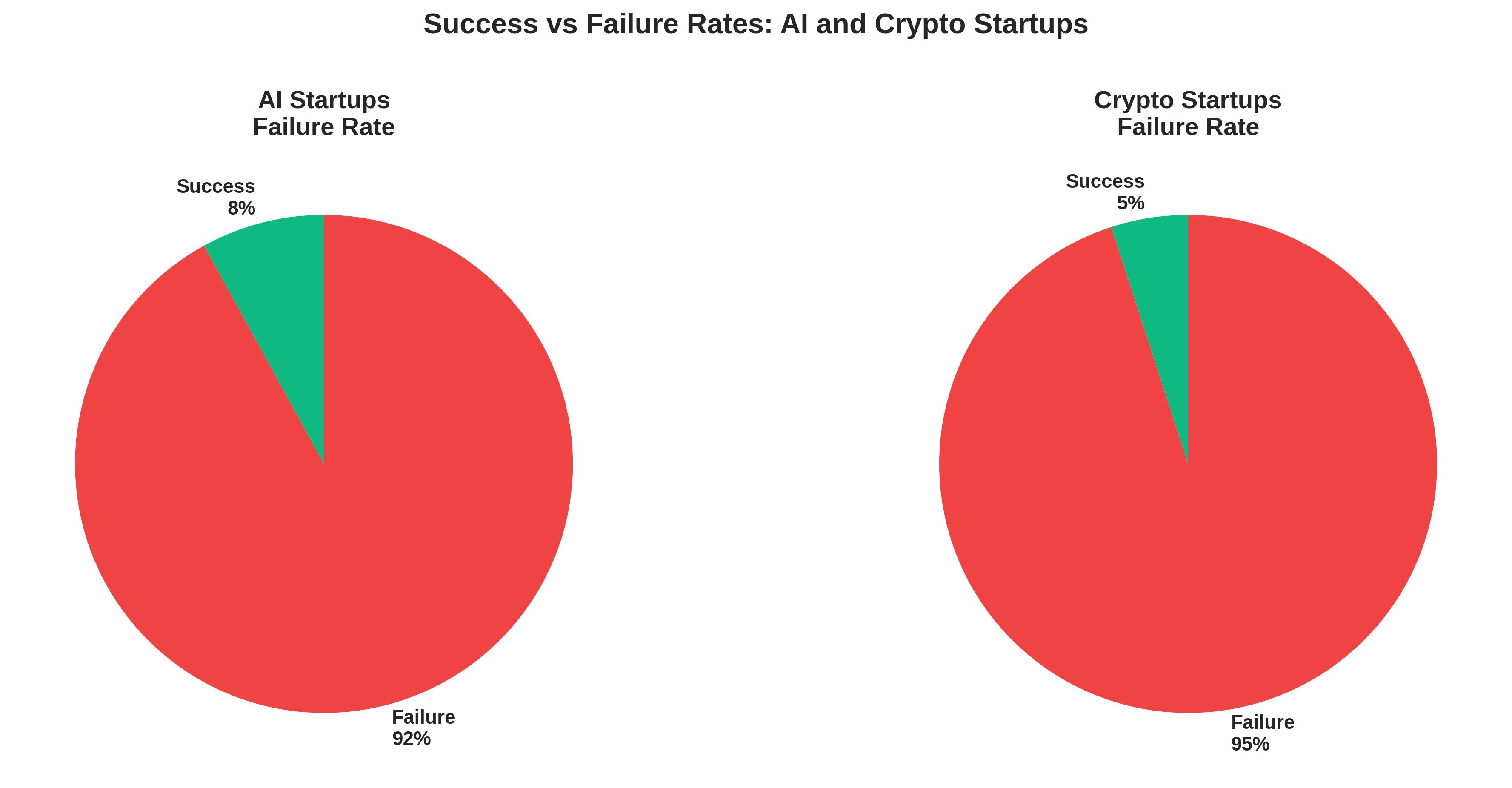

The AI ecosystem is 27 times larger by startup count. Yet both face similar survival challenges: 90%+ failure rates within the first three years. AI startups see an 85-92% failure rate; crypto startups face 90-95% failure rates.

Who Survives?

AI: 214 unicorns valued at $1B+ (0.31% of all AI startups)

Crypto: ~25 unicorns (0.96% of funded crypto startups)

Despite the disparity in funding and scale, the survival patterns are remarkably similar. The vast majority fail. A tiny percentage achieves unicorn status. And when you look at who wins, a pattern emerges.

Both Are Building Foundational Infrastructure — But for Different Purposes

Here’s the crucial insight: AI and blockchain are both foundational technologies playing the same game — building foundational infrastructure that enables entire ecosystems.

AI: The Intelligence Layer

AI companies aren’t building end applications. They’re selling the tools to automate intelligence — foundational models, infrastructure, and APIs that let everyone else build intelligent applications.

The infrastructure providers:

OpenAI, Anthropic: Selling access to language models ($157B and $40B valuations)

Databricks: Selling data infrastructure for AI training ($62B valuation)

Nvidia: Providing the essential compute hardware — GPUs for compute

Hugging Face: Selling the marketplace for AI models and tools

Scale AI: Selling data labeling and training infrastructure ($14B valuation)

Crypto: The Infrastructure Layer

Crypto companies aren’t building financial applications. They’re selling the rails for programmable value transfer — blockchain infrastructure, custody solutions, and developer tools that enable everyone else to build decentralized applications.

The infrastructure providers:

Coinbase: Selling institutional-grade custody and exchange infrastructure ($50B+ valuation)

Fireblocks: Selling enterprise custody and transaction infrastructure ($8B valuation)

Alchemy: Selling node infrastructure and blockchain APIs ($10.2B valuation)

Ripple: Selling cross-border payment infrastructure ($11B+ valuation)

Chainalysis: Selling blockchain analytics and compliance tools ($8.6B valuation)

Look at those top-valued companies in each sector. They’re not building trading algorithms or DeFi applications. They’re building the foundational infrastructure that enables thousands of others to build them.

The Pattern: In both AI and crypto, the consistent winners are infrastructure providers. Individual applications may succeed or fail, but the infrastructure providers generate revenue regardless of which specific use cases win.

And most importantly — unlike AI, there are only a handful of successful, scalable infrastructure providers — which to me represents tremendous opportunity.

The AI Multiplier: Democratizing Quantitative Finance

Now we get to the really interesting part — the part I’m living through in real-time.

Large language models like Codex, Claude, and GPT-5.1 are making it trivially easy for anyone to set up and test sophisticated trading strategies.

This isn’t about AI generating alpha — though that might come eventually. This is about AI making the tools for generating alpha accessible to anyone. The barrier to entry for quantitative trading has collapsed.

Look at what this means in practical terms:

Strategy prototyping that once required teams of quantitative developers can now be done by individuals in hours

Research papers that were opaque to non-specialists can be implemented and tested by anyone willing to learn

Backtesting frameworks that took months to build can be scaffolded and refined iteratively with AI assistance

Risk management systems can be constructed and customized without enterprise software budgets

This puts incredible technologies at the fingertips of retail traders — limited only by data access, execution speed, and processing power. The intellectual barriers have largely fallen. The knowledge gap between retail and institutional traders is narrowing rapidly.

The Institutional Implications: If Retail Can Do This...

If a single person with AI assistance can build, test, and deploy sophisticated trading strategies, what can larger trading houses do?

The answer is both obvious and profound: much, much more.

Institutional players have advantages retail traders can’t replicate:

Data access: Bloomberg terminals, alternative data feeds, proprietary datasets

Execution: Direct market access, co-location, smart order routing

Capital: The ability to run thousands of strategies simultaneously and absorb drawdowns

Infrastructure: Dedicated engineering teams, risk management systems, compliance frameworks

Add AI to this mix, and you get a multiplicative effect. AI doesn’t just make these institutions slightly better — it could fundamentally transform what’s possible at institutional scale.

A former boss of mine would say: “There’s no compression algorithm for experience.” That still remains true — however, we are now capable of providing incredible leverage for those with the right experience and know-how.

But here’s the constraint: all of this runs on traditional financial infrastructure with T+2 settlement, intermediated clearing, and operational overhead that hasn’t fundamentally changed in decades.

To fully realize the potential of AI-driven trading at institutional scale, you need blockchain infrastructure.

Why? Because AI-generated strategies can iterate and adapt faster than traditional settlement rails can process. Because global, 24/7 markets require always-on infrastructure. Because the composability of DeFi protocols allows for strategy complexity that traditional markets can’t support. Because smart contracts can encode risk management and compliance programmatically rather than through manual oversight.

Blockchain isn’t just about decentralization or trustlessness. It’s about programmable financial infrastructure that can keep pace with AI-driven strategy generation and execution.

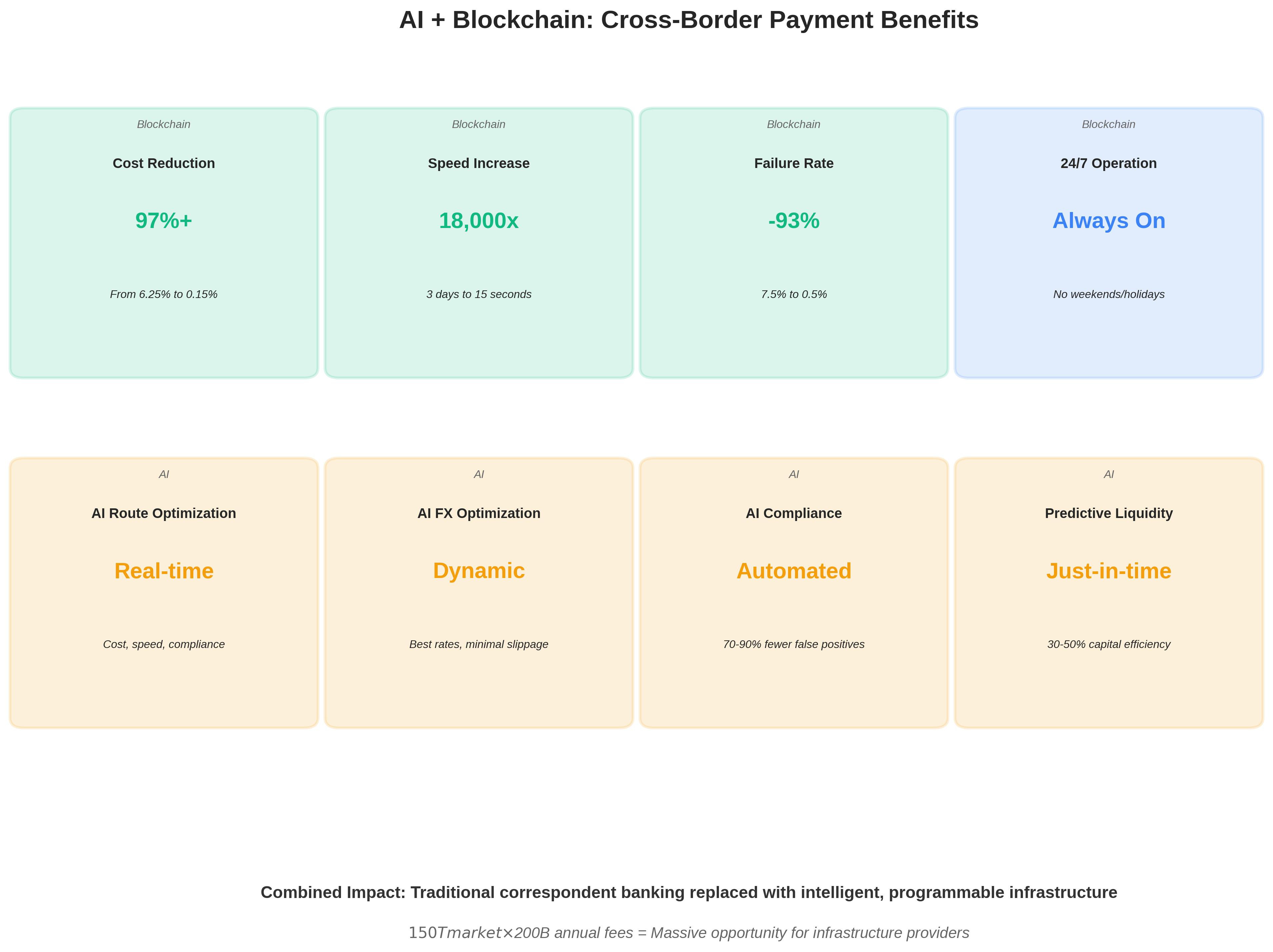

Cross-Border Payments: Where the Convergence Is Already Happening

If you want to see AI + blockchain convergence in action today — not in some speculative future — look at foreign exchange and cross-border payments. This is where the rubber meets the road, where billions of dollars move daily, and where the infrastructure is already being rebuilt from the ground up.

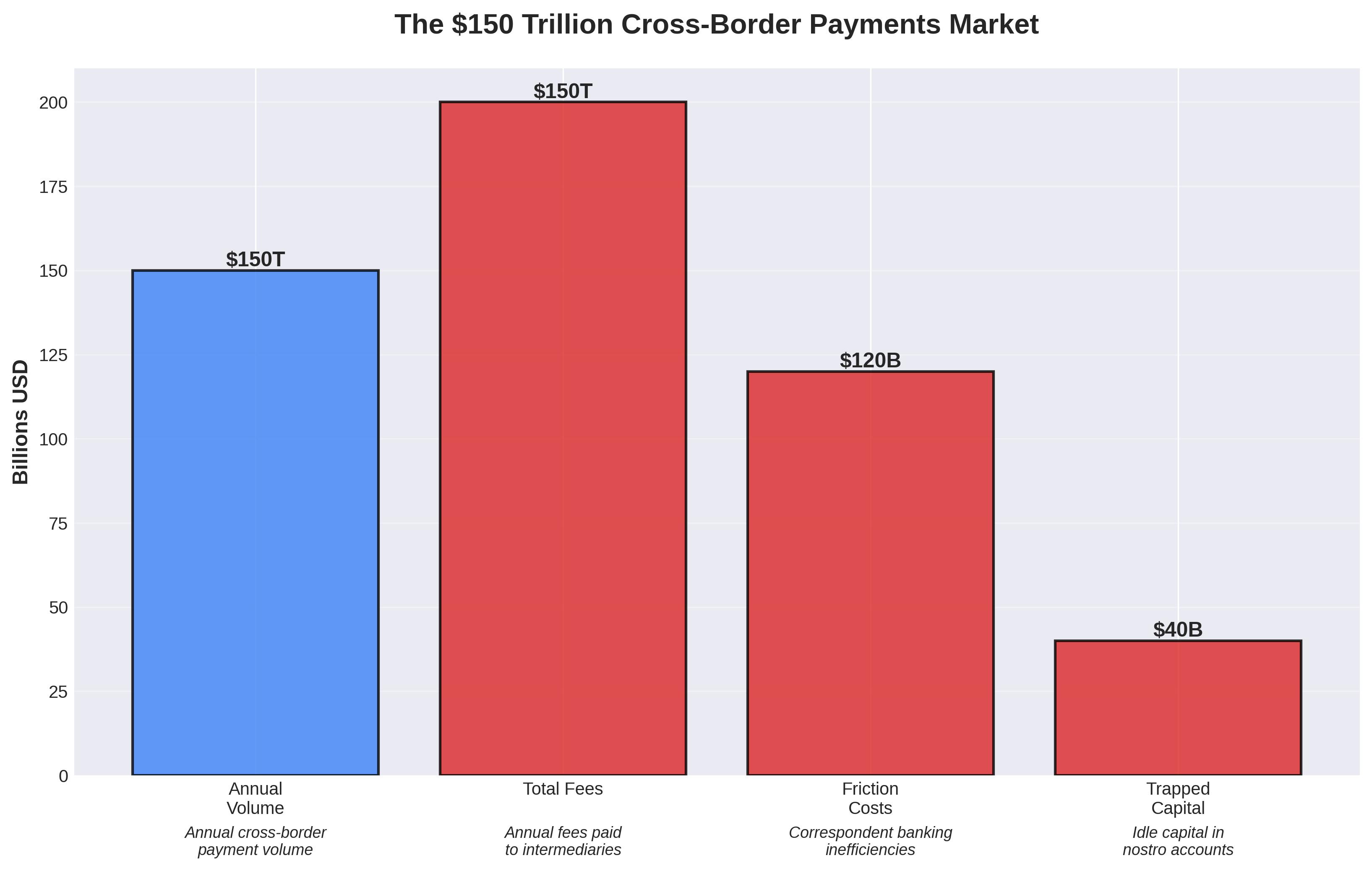

The $150 Trillion Problem

The global cross-border payments market processes over $150 trillion annually. That’s not a typo. Every day, trillions of dollars need to move between countries, currencies, and financial systems. And the infrastructure powering it is Byzantine.

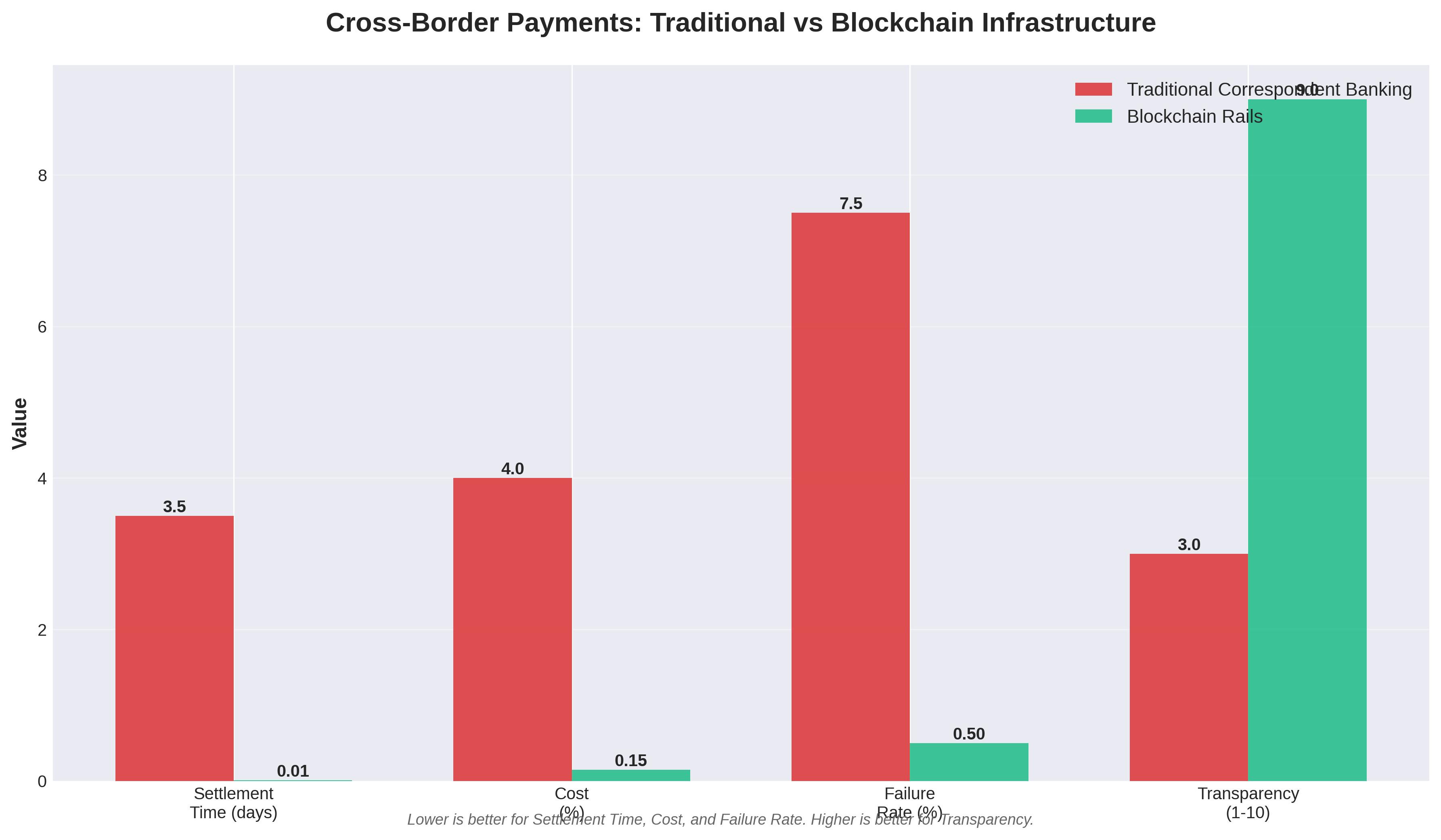

Traditional cross-border payments run through correspondent banking networks — chains of intermediary banks that hold accounts with each other to facilitate transfers. A payment from the US to Indonesia might touch 5-7 intermediary banks, each taking a cut and adding time. The result:

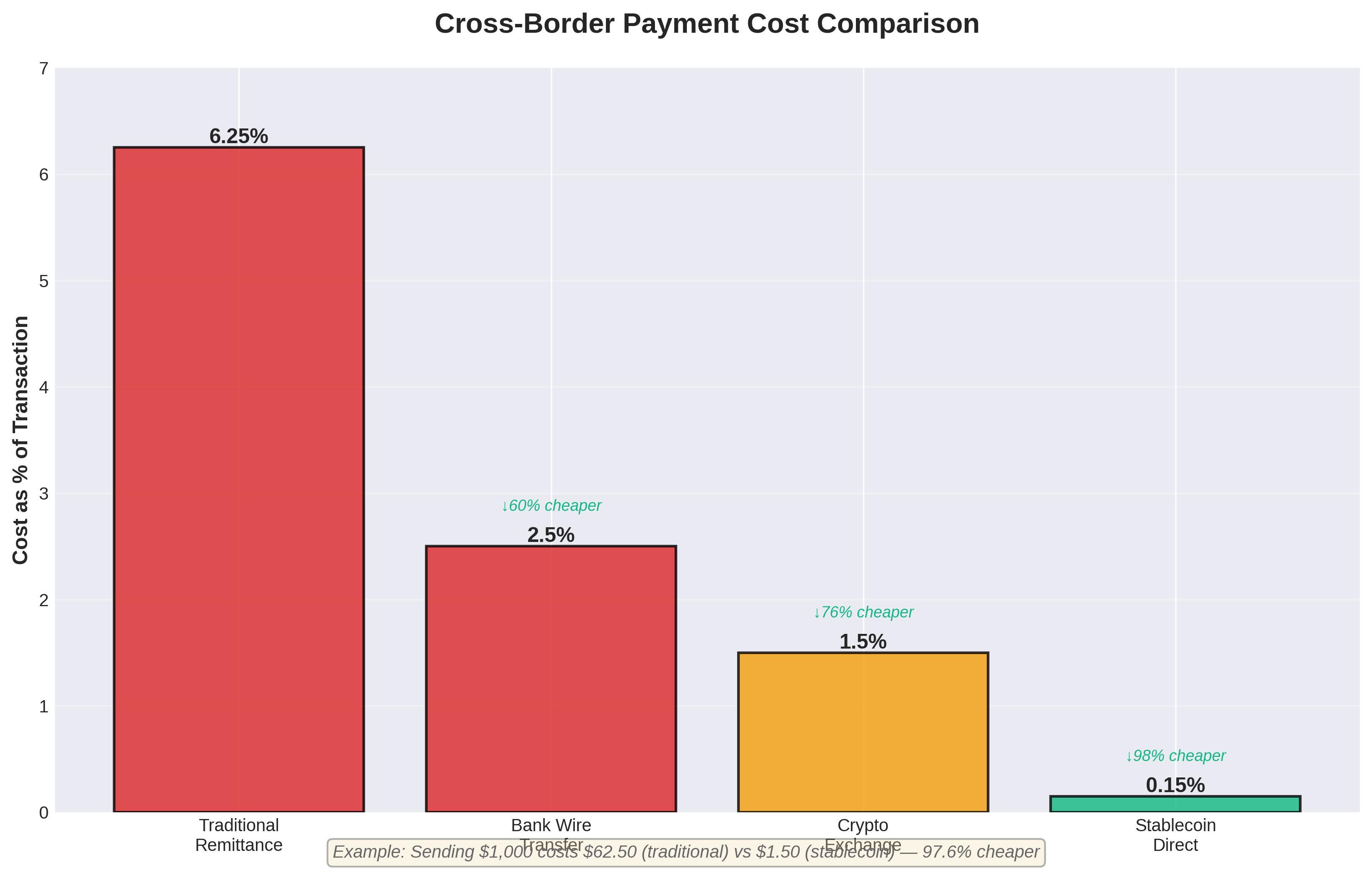

Settlement times: 3-5 business days (sometimes longer)

Costs: Average 6.25% for remittances, 1-3% for corporate transfers

Opacity: Impossible to track where your money is in the chain

Failure rates: 5-10% of cross-border payments fail and need manual intervention

FX spreads: Hidden markups in currency conversion ranging from 1-4%

For a market processing $150 trillion annually, these inefficiencies represent hundreds of billions in friction costs. More importantly, they create structural barriers that limit global commerce and financial inclusion.

Crypto Infrastructure: Building the Rails

Blockchain-based payment rails are already changing this landscape — not through speculation or price appreciation, but through infrastructure that works.

Stablecoins as Payment Rails:

Stablecoins have emerged as the most practical crypto use case for payments. They combine the speed and programmability of blockchain with the stability of fiat currencies:

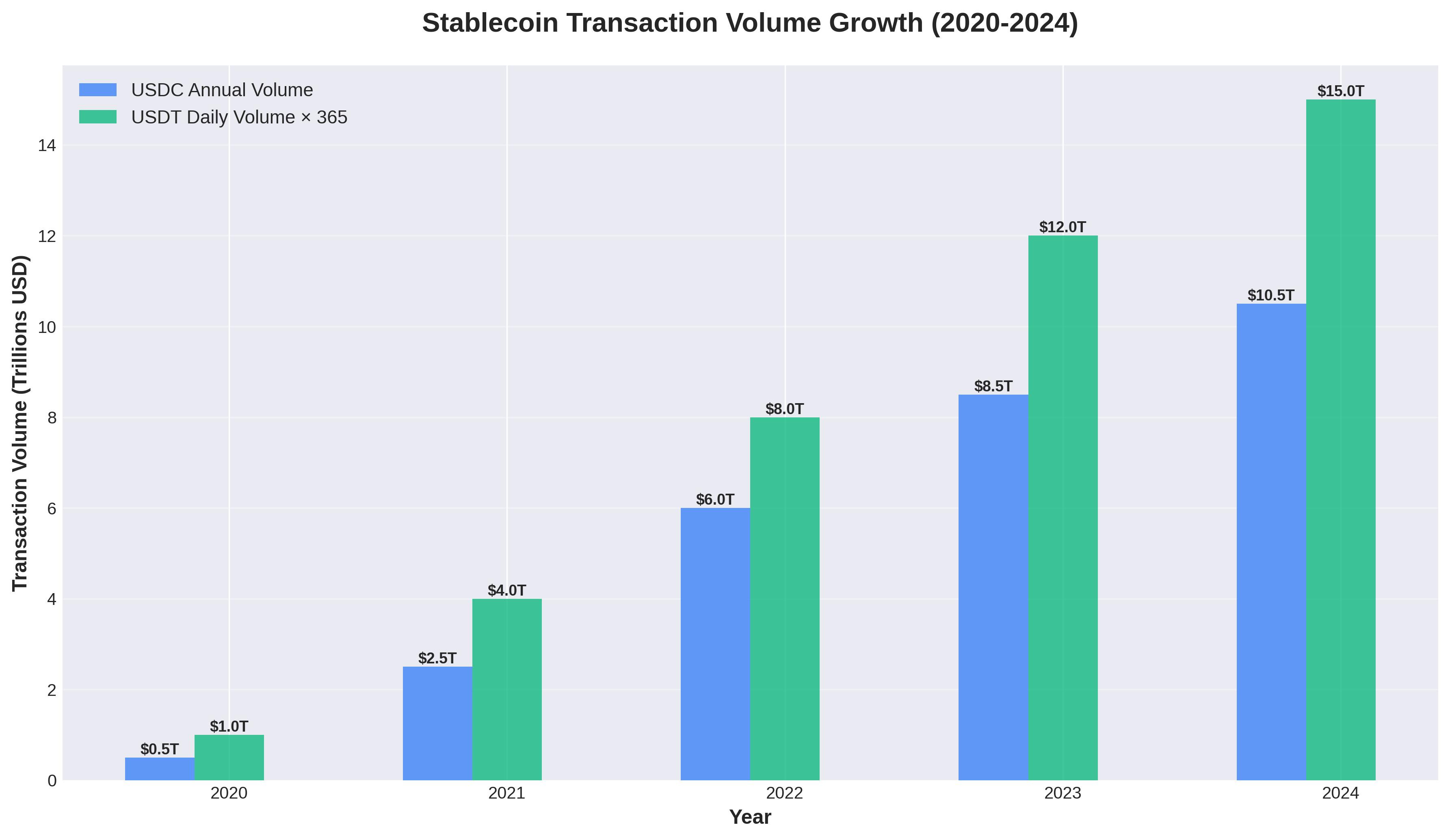

USDC (Circle): Processing $10+ trillion in annual transaction volume

USDT (Tether): Over $50 billion in daily trading volume, widely used for settlements

Purpose-built rails: Stellar, Ripple’s XRP Ledger designed specifically for cross-border transfers

The value proposition is compelling:

Settlement: Near-instant (seconds to minutes vs. days)

Cost: $0.01-$1.00 per transaction vs. percentage-based fees

Transparency: Every hop visible on-chain

Programmability: Smart contracts can automate compliance, escrow, and conditional payments

24/7 operation: No weekends, no holidays, no “business hours”

Real-World Adoption:

This isn’t theoretical. Major institutions are already using blockchain rails:

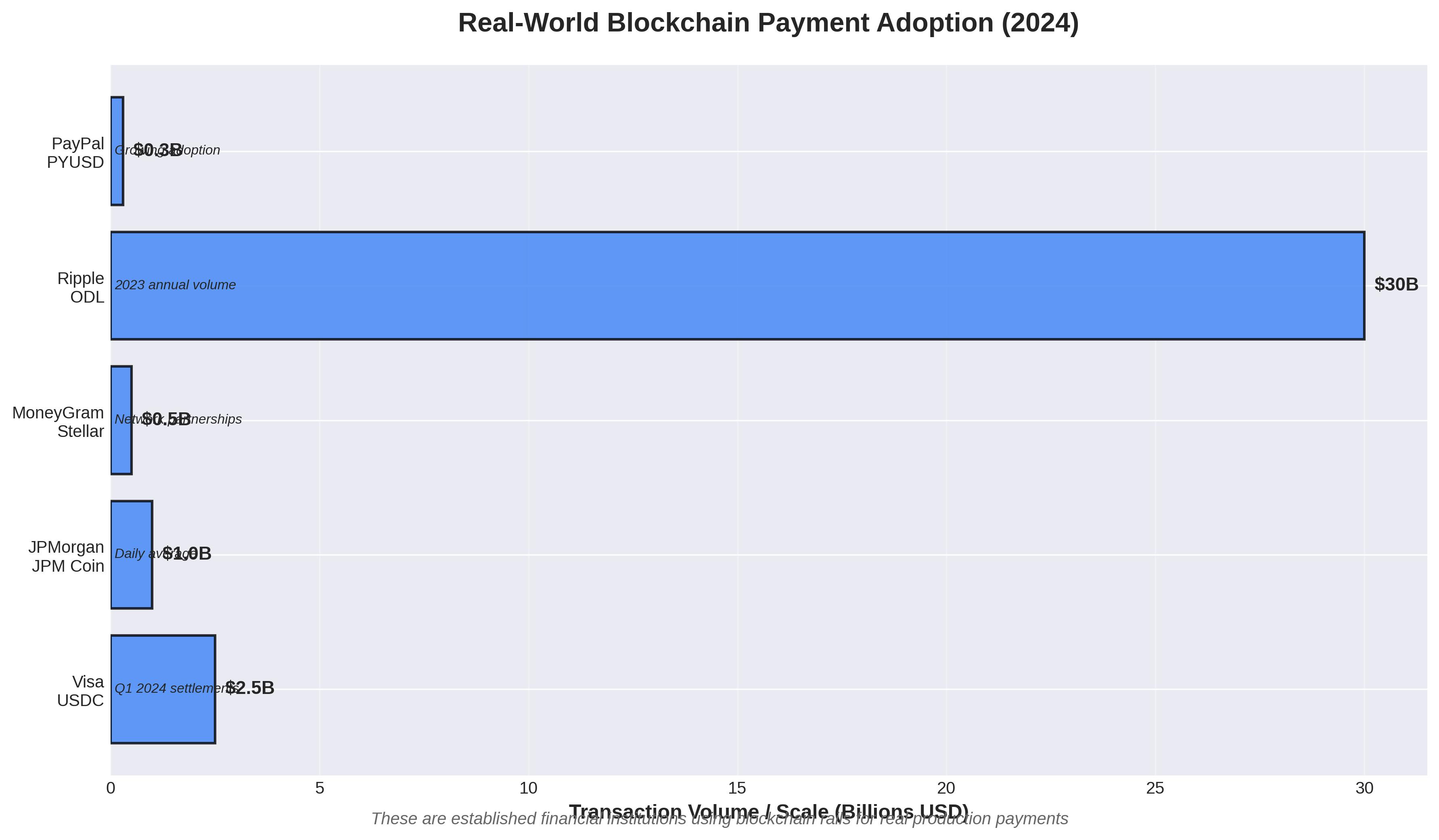

Visa: Settled over $2.5 billion in USDC transactions in Q1 2024 alone

PayPal: Launched PYUSD stablecoin for merchant settlements

JPMorgan: JPM Coin processes $1 billion+ in daily transactions for corporate clients

MoneyGram: Partnered with Stellar to enable blockchain-based remittances to 180+ countries

SWIFT: Piloting blockchain integration for cross-border payments

The infrastructure providers building these rails — Circle, Tether, Ripple, Stellar, Fireblocks — are the foundational layer of this ecosystem. They don’t care if you’re sending a $10 remittance or a $10 million trade settlement. They provide the essential rails that enable all transaction types.

Where AI Amplifies the Infrastructure

Blockchain solves the settlement problem. AI solves the optimization, routing, and risk management problems. Together, they create something far more powerful than either alone.

1. Intelligent Route Optimization

Cross-border payments often have multiple possible routes — different blockchain networks, different liquidity pools, different on/off-ramps. AI can optimize routing in real-time:

Cost minimization: Select the cheapest path considering gas fees, FX spreads, and liquidity

Speed optimization: Route based on network congestion and settlement times

Compliance routing: Automatically select compliant paths based on sender/receiver jurisdictions

Liquidity optimization: Route through pools with sufficient depth to minimize slippage

Think of it as Google Maps for money. You tell the system where money needs to go, and AI finds the optimal route considering cost, speed, and constraints. The blockchain provides the roads; AI provides the navigation.

2. Real-Time FX Optimization

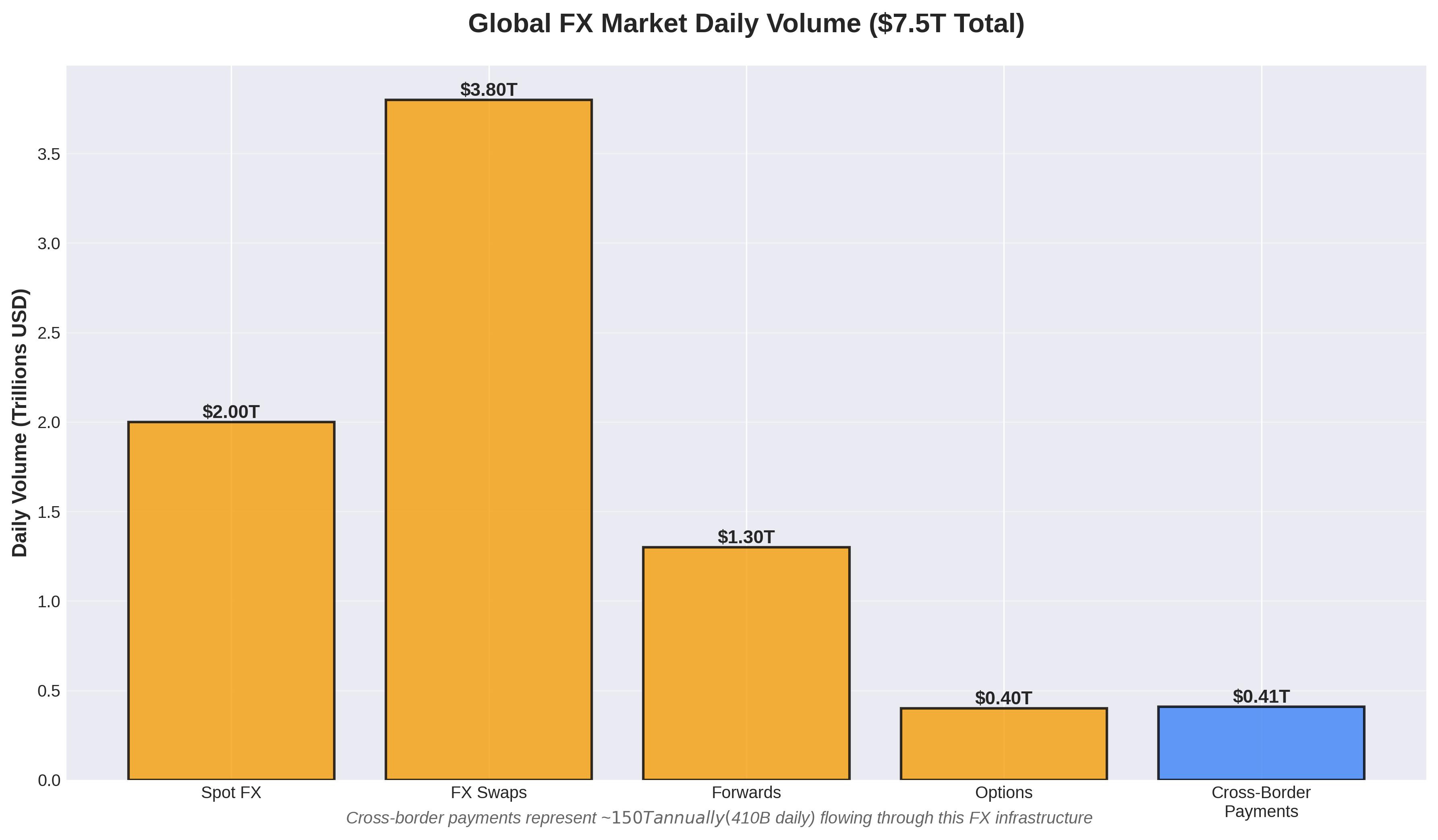

Foreign exchange is a $7.5 trillion daily market. Traditional FX for cross-border payments involves:

Wide bid-ask spreads (banks profit from the markup)

Delayed execution (sometimes hours after quote)

Opaque pricing (you never know the true rate you’re getting)

AI + blockchain changes this:

AI-powered FX optimization:

Real-time pricing: AI models predict optimal execution times based on market microstructure

Smart order routing: Break large FX conversions into smaller orders to minimize market impact

Spread arbitrage: Identify and execute trades across multiple venues to get best rates

Liquidity aggregation: AI pools liquidity from DEXs, CEXs, and OTC desks to reduce slippage

Blockchain settlement:

Execute the FX swap on-chain with transparent pricing

Settle instantly rather than T+2

No counterparty risk (atomic swaps)

Programmable escrow and conditional execution

Companies like 1inch, Uniswap, and Curve are building the DEX infrastructure. Companies like Chainlink provide price oracles. AI layers on top can optimize across all of them simultaneously.

Example: A company needs to convert $10 million USD to Indonesian Rupiah and settle in Jakarta. Traditional route: 3-5 days, 2-3% in fees and spreads, counterparty risk. AI + blockchain route: AI determines optimal conversion path (USD → USDC → Rupiah stablecoin → bank account), executes across multiple liquidity pools to minimize slippage, settles in 15 minutes, total cost 0.15%. The infrastructure enabling this exists today.

3. AI-Powered Compliance and Risk Management

Cross-border payments are heavily regulated. Banks spend billions on compliance — AML (anti-money laundering), KYC (know your customer), sanctions screening, transaction monitoring. This is a major cost center and slows down payments.

AI can automate and improve compliance:

Transaction Monitoring:

Pattern recognition to identify suspicious transactions in real-time

Behavioral analysis to detect structuring, layering, or other money laundering techniques

Network analysis to identify links between entities across chains

Anomaly detection to flag unusual patterns requiring review

Sanctions Screening:

Real-time screening against OFAC, UN, and EU sanctions lists

Entity resolution to identify sanctioned parties using obfuscated identities

Predictive models to assess sanctions risk before payment execution

Risk Scoring:

AI assigns risk scores to transactions based on sender, receiver, amount, destination, and historical patterns

High-risk transactions routed for manual review; low-risk auto-approved

Reduces false positives by 70-90% compared to rule-based systems

Companies like Chainalysis ($8.6B valuation), Elliptic, and TRM Labs are building this compliance infrastructure. They’re infrastructure providers — providing the tools that enable legitimate blockchain payments while screening out illicit activity.

The blockchain advantage: Every transaction is recorded on-chain. AI can analyze the entire transaction history of an address instantly. Compare this to traditional banking where transaction history is siloed across banks and jurisdictions. Blockchain creates a global, transparent audit trail that AI can analyze.

4. Predictive Liquidity Management

Cross-border payments require liquidity in multiple currencies across multiple geographies. Banks maintain “nostro” accounts (foreign currency accounts held abroad) to facilitate payments. These accounts tie up billions in idle capital.

AI + blockchain enable just-in-time liquidity:

AI predictions:

Forecast payment flows by currency pair, region, and time of day

Predict liquidity needs 24-48 hours ahead based on historical patterns

Optimize capital allocation across currencies and geographies

Blockchain execution:

Provision liquidity only when needed via DeFi lending protocols

Execute instant FX swaps to rebalance currency positions

Use flash loans for temporary liquidity during peak demand

Automate liquidity rebalancing across global accounts

Result: Banks can reduce trapped capital in nostro accounts by 30-50%, freeing up billions for productive use. The AI predicts needs; blockchain executes the rebalancing instantly.

Ripple’s On-Demand Liquidity (ODL) service is an early version of this — using XRP as a bridge currency to eliminate the need for pre-funded nostro accounts. ODL processed over $30 billion in 2023. The next generation adds AI-powered prediction and optimization on top of the blockchain settlement.

The Infrastructure Providers in Cross-Border Payments

Look at who’s building the infrastructure and winning:

Blockchain Infrastructure:

Fireblocks: $8B valuation, providing custody and settlement infrastructure

Circle (USDC): $5B+ valuation, processing $10T+ annually in stablecoin transfers

Ripple: $11B+ valuation, 300+ financial institution partnerships

Stellar: Non-profit, but powering MoneyGram and other major remittance players

AI/Compliance Infrastructure:

Chainalysis: $8.6B valuation, blockchain analytics and compliance

Elliptic: ~$1B valuation, crypto transaction monitoring

TRM Labs: $500M+ valuation, blockchain intelligence

Hybrid Infrastructure:

Wise (formerly TransferWise): $11B+ valuation, using AI for FX optimization (moving toward blockchain rails)

Revolut: $33B valuation, multi-currency accounts with crypto integration

Stripe: $106B+ valuation, building stablecoin payment infrastructure

Notice the pattern: None of these companies are making money from FX trading or currency speculation. They provide essential infrastructure — the custody, the compliance, the analytics, the settlement rails. They’re the infrastructure providers.

The Market Opportunity

The numbers are staggering:

Traditional Market:

$150 trillion in annual cross-border payment volume

$200+ billion in annual fees (at ~0.15% average take rate)

$7.5 trillion daily FX market

Friction Costs:

$120 billion annually in correspondent banking fees

$40 billion in trapped nostro account capital (opportunity cost)

$30 billion in failed payment remediation

Countless billions in delayed business due to settlement times

Crypto Infrastructure Already Capturing:

Stablecoins: $10+ trillion in annual transaction volume (Circle alone)

Growing at 100%+ year-over-year

Still <10% of traditional cross-border payment volume

The Wedge:

Crypto infrastructure enters through high-friction use cases:

Remittances: 6.25% average cost → perfect first market

Emerging markets: Where traditional banking is expensive or unavailable

Crypto-native businesses: Already operating on blockchain rails

Treasury operations: Companies managing multi-currency positions

Expanding outward: As infrastructure matures, capturing traditional wholesale payments

AI accelerates this by making blockchain rails enterprise-ready:

Compliance automation → passes regulatory muster

Intelligent routing → better performance than traditional rails

Risk management → acceptable to institutional treasurers

Predictive analytics → integrates into existing treasury systems

Why This Matters for the Convergence Thesis

Cross-border payments is the canary in the coal mine for AI + blockchain convergence:

It’s happening now: Not speculative, not experimental — live production systems processing billions.

It’s infrastructure-driven: The winners are building enabling infrastructure, not competing in the applications layer.

It demonstrates the multiplier effect: Neither AI nor blockchain alone could disrupt correspondent banking. Together, they provide a complete alternative stack.

It’s massive: $150 trillion market with $200B+ in annual fees. Even capturing 10% is a $20B+ annual revenue pool.

It’s expanding: Started with remittances and crypto-native use cases; moving upmarket to corporate treasury, trade finance, and wholesale payments.

If you want to understand how AI + blockchain will transform financial markets broadly, watch cross-border payments. The infrastructure being built here — the custody solutions, the compliance tools, the intelligent routing systems, the settlement rails — will be repurposed for trading, lending, asset management, and every other financial use case.

The infrastructure providers in cross-border payments are building the foundational infrastructure for autonomous, intelligent financial markets. They’re not building payment apps or FX trading platforms. They’re building the pipes, the rails, the compliance layers, and the optimization engines that everyone else will use. This is where players like Fireblocks can thrive and grow.

And they’re profitable today — not someday, not in theory — today. That’s how you know the convergence is real.

The Convergence: AI + Blockchain

The combination of AI and blockchain could genuinely radicalize financial markets infrastructure.

Here’s why this convergence is different from previous waves of financial technology innovation:

AI provides the intelligence layer — the ability to generate, test, optimize, and deploy trading strategies at scale. It democratizes quantitative finance and makes sophisticated approaches accessible to both retail and institutional participants. It turns trading from a manual craft into a programmatic discipline.

The infrastructure winners in AI aren’t building trading strategies. They’re building the intelligence infrastructure:

Foundation models that can understand and generate code

Computing infrastructure that can train and run models at scale

Data platforms that can organize and analyze massive datasets

API layers that make intelligence accessible to any application

Blockchain provides the execution layer — the infrastructure for 24/7 settlement, programmable compliance, composable financial primitives, and transparent audit trails. It removes intermediaries and operational overhead while maintaining security and integrity.

The infrastructure winners in crypto aren’t building DeFi protocols. They’re building the value transfer infrastructure:

Blockchain networks that can settle transactions instantly

Custody solutions that can secure assets at institutional scale

Node infrastructure that can handle millions of transactions

Stablecoin rails that can move value without friction

Together, they create a flywheel:

AI makes it easier to develop sophisticated strategies

Blockchain makes it cheaper and faster to execute them

Lower barriers attract more participants

More participants create more data and activity

More data makes AI models more effective

The cycle continues

We’re already seeing early versions of this:

Trading bots on decentralized exchanges that use machine learning for market making

Automated liquidity provision strategies that adjust parameters based on market conditions

Cross-chain arbitrage bots that execute faster than human traders can monitor

Yield optimization strategies that programmatically shift capital across DeFi protocols

These are crude implementations compared to what’s coming. They’re like the first websites in 1995 — functional but primitive compared to what the infrastructure will enable once it matures.

The real opportunity emerges when institutional-grade AI meets institutional-grade blockchain infrastructure. When BlackRock-level risk analytics can be applied to crypto-native strategies. When Goldman-level execution quality becomes available on blockchain rails. When the speed of HFT meets the programmability of smart contracts.

That’s not speculative. That’s inevitable.

The Infrastructure Provider Advantage at the Convergence

Here’s what makes this convergence particularly powerful: the winners won’t be building trading strategies or financial applications directly.

Just as OpenAI doesn’t care what you build with GPT-5.1, and Ethereum doesn’t care what smart contracts you deploy, the convergence winners will be infrastructure providers selling the bridges between AI intelligence and blockchain execution.

They’ll be selling:

APIs that connect AI models to blockchain networks

Execution engines that translate AI-generated strategies into smart contracts

Risk management frameworks that operate programmatically across both layers

Data pipelines that feed blockchain activity into AI training sets

Compliance solutions that encode regulatory requirements in code

The infrastructure providers in this convergence will profit regardless of whether individual trading strategies succeed or fail. They’ll get paid when retail traders use their infrastructure. They’ll get paid when institutions use their infrastructure. They’ll get paid when the next generation of financial applications gets built on their infrastructure.

In a major market transformation, the infrastructure providers are the ones who generate consistent returns — and we’re watching one of the most significant infrastructure buildouts in financial markets history.

The Opportunity: Scale, Speed, and Structure

The potential here is genuinely difficult to overstate.

Traditional financial markets represent roughly $300 trillion in global equity and bond markets, plus hundreds of trillions more in derivatives. Crypto markets are currently around $2-3 trillion — still a rounding error.

But the size of existing markets isn’t the right way to think about this opportunity. The question is: what becomes possible when the friction of traditional markets is removed?

Consider three themes that will likely define the next decade of financial market infrastructure:

1. Democratization of Sophisticated Finance

AI makes quantitative strategies accessible to retail traders. Blockchain makes 24/7 global markets with instant settlement available to everyone. Together, they eliminate the moats that protected traditional finance — information asymmetry, operational complexity, and capital requirements.

This doesn’t mean retail traders will suddenly outperform institutions. It means the playing field flattens. The advantages that remain are data, capital, and execution speed — not access to tools or knowledge. That’s a fundamentally different market structure.

When you look at the investment numbers — $131.5B flowing into AI infrastructure and $13.7B into blockchain infrastructure in 2024 alone — you’re watching the capital markets vote on this thesis with real money. These aren’t speculative bets. This is infrastructure being built right now.

The growth potential here isn’t measured in percentages — it’s measured in orders of magnitude. When billions of people have access to institutional-quality tools, market participation explodes.

2. Institutional Transformation

Traditional financial institutions are built around intermediation, manual processes, and settlement delays. AI + blockchain infrastructure makes much of this obsolete.

We’ll see institutions either rebuild their infrastructure on these new rails or get outcompeted by AI-native and crypto-native firms that never had legacy systems to maintain. The transition won’t be instant — regulatory frameworks and risk management requirements will slow adoption — but the direction is clear.

The institutions that figure out how to combine their advantages (capital, data, relationships) with new infrastructure will dominate the next era of finance. Look at the winners in both sectors:

AI infrastructure: OpenAI ($157B), Databricks ($62B), Anthropic ($40B)

Crypto infrastructure: Coinbase ($50B+), Fireblocks ($8B), Alchemy ($10.2B)

These aren’t retail-focused companies. They’re infrastructure providers serving institutions. The ones that don’t adapt will become obsolete.

3. New Market Structures

Perhaps most interestingly, AI + blockchain enables entirely new market designs that weren’t possible before.

Imagine prediction markets with AI-powered liquidity provision. Imagine derivatives markets where risk management is encoded in smart contracts and automatically enforced. Imagine cross-asset strategies that execute simultaneously across traditional and crypto markets with AI coordinating the trades and blockchain settling them instantly.

We’re not just making existing markets more efficient — we’re creating entirely new market structures. The growth potential here is uncapped because we’re inventing new categories of financial products and services.

The infrastructure for this is being built now. The $145 billion invested in AI and blockchain infrastructure in 2024 is building the pipes, the rails, the custody solutions, the execution engines, and the intelligence layers that will power these new markets.

Looking Forward

I started this piece talking about my experience watching banks around the world grapple with technology adoption. The ones that embraced technology early didn’t just survive — they thrived. The ones that waited became cautionary tales.

We’re at a similar inflection point now, but the stakes are higher and the timeline is compressed.

The numbers don’t lie:

70,000+ AI startups competing to build intelligence infrastructure

2,600+ crypto startups building value transfer infrastructure

$145 billion invested in both sectors in 2024 alone

90%+ will fail, but the infrastructure they’re building will remain

The startups might fail. Most will. That’s the nature of innovation — lots of experiments, few survivors. But the infrastructure persists. The APIs remain. The protocols continue running. The models get better with more data.

AI is making quantitative finance accessible to everyone. Blockchain is providing infrastructure that can execute at the speed of AI-generated strategies. The combination will reshape financial markets more dramatically than electronic trading, more fundamentally than high-frequency trading, and more completely than the internet itself reshaped commerce.

The institutions that recognize this early — that invest in AI capabilities and blockchain infrastructure now — will define the next era of finance. The ones that wait will be left behind, wondering how they lost their competitive advantages so quickly.

For retail traders like me, this is already here. I’m building and testing strategies that would have been impossible without AI, and I’m watching crypto infrastructure mature into something capable of supporting institutional-scale operations.

The future of financial markets isn’t traditional markets enhanced by technology. It’s entirely new markets built on AI and blockchain infrastructure from the ground up.

The infrastructure providers are already profitable. OpenAI, Anthropic, and Databricks on the AI side. Coinbase, Fireblocks, and Alchemy on the crypto side. They’re not building trading strategies or financial applications. They’re building the foundational infrastructure — the core infrastructure — that enable everyone else to build them.

And in a major market transformation that’s just beginning, the infrastructure providers are the ones who generate consistent returns — regardless of which specific applications succeed.

The convergence is happening. The infrastructure is being built. The capital is flowing.

And it’s arriving faster than most people realize.

Data sources: Crunchbase, PitchBook, CB Insights, Galaxy Research, The Block, Stanford AI Index Report (2020-2024)

Opinions expressed here are my own and do not represent those of my employer. The information presented in Math & Markets is not investment or financial advice and should not be construed as such.