Testing the Hybrid Ensemble as an Overlay (w/ Dual & Volatility Strategies)

Post 20 outlines my attempts at using the hybrid ensemble to improve my two core strategies

This is part 20 of my series — Building & Scaling Algorithmic Trading Strategies

I wanted to see whether the new hybrid ML ensemble could act as a risk overlay on top of my existing strategies — both the dual allocator and the VIX volatility sleeve. I ran ROI, CAGR, Sharpe, and max-drawdown comparisons for:

the original strategies, and

the hybrid-gated versions (dual + hybrid, vol sleeve + hybrid)

Here’s what happened.

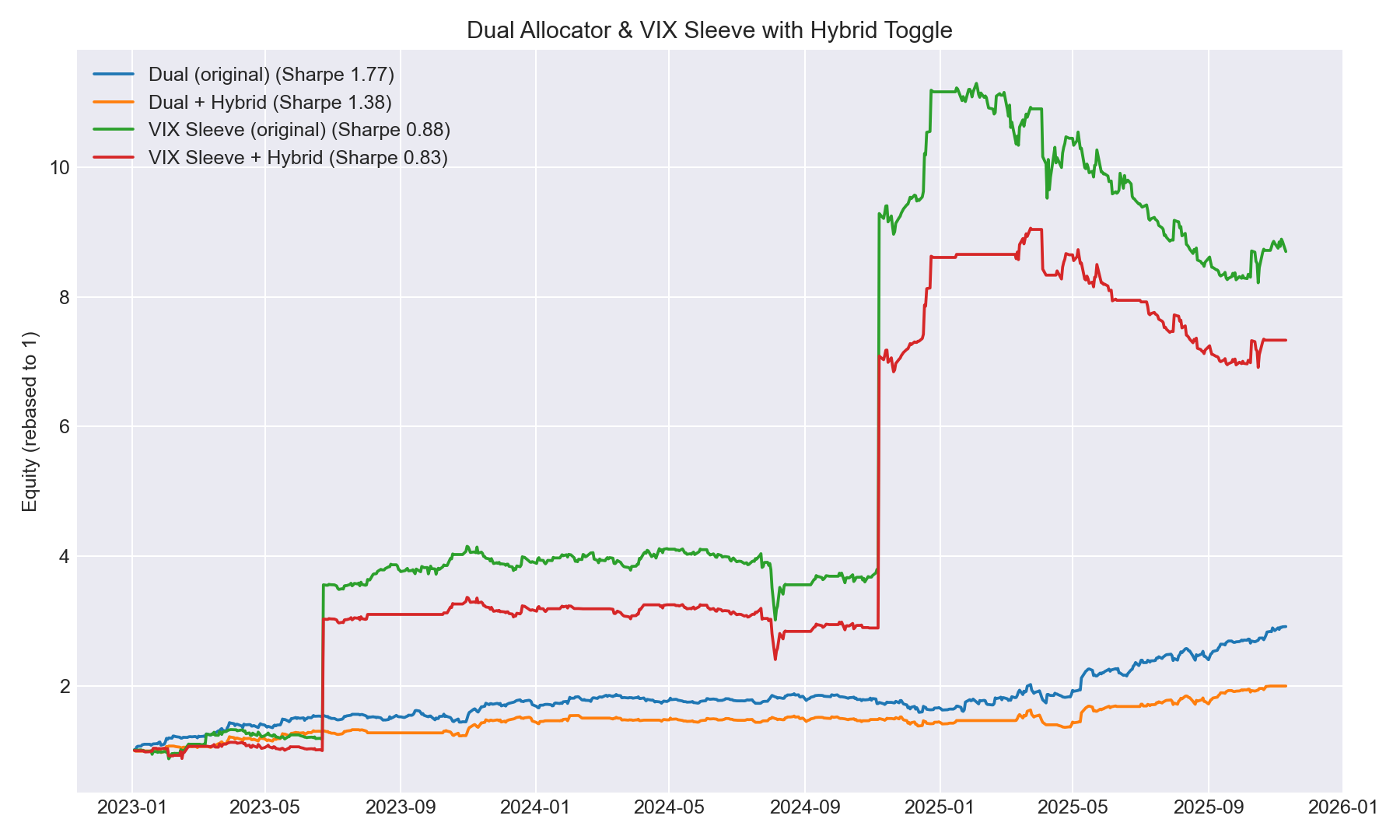

Toggle Impact

Dual Allocator (2023–present)

ROI: 191% → 100%

CAGR: 43.8% → 26.5%

Sharpe: 1.77 → 1.38

Max DD: –15.3% → –16.5%

The toggle sat out many of the allocator’s best runs but still participated in the larger drawdowns. It essentially muted upside without meaningfully improving the path.

Volatility Sleeve

ROI: 770% → 633%

CAGR: 113.9% → 101.4%

Sharpe: 0.88 → 0.83

Max DD: –27.4% → –28.5%

The VIX sleeve earns its edge during stress regimes — exactly when the hybrid ensemble flips to cash. The overlay acted more like a brake than a hedge.

Observations

The hybrid model tends to flag “risk” after macro/vol shocks are already realized. That timing is too slow relative to the dual allocator’s internal controls.

For the VIX sleeve, the toggle shuts risk precisely when the strategy is supposed to shine.

This test only covers the 2023+ window where the hybrid model exists, so sample size is limited.

Could explore partial exposure (0.5 instead of 0), lagged thresholds, or retraining the ensemble using sleeve-specific features.

Conclusion

It’s an interesting overlay — but for now, I’m leaving both the dual allocator and volatility sleeve untouched. The toggle needs more calibration before it becomes additive.

The information presented in Math & Markets is not financial advice and should not be construed as such.