Testing a Macro Sleeve Strategy: Take Two

Part 35 talks about my attempts at combining macros with equities and volatility

This is part 35 of my series — Building & Scaling Algorithmic Trading Strategies

I had previously written about the first cross-asset indicators I was prototyping.

Following up on that, I built a standalone macro-alpha package that combines macro filters with an equity sleeve (SPY + optional TLT hedge) and a VIX term-structure sleeve. The idea was straightforward: use economic indicators to filter, trade trend signals on equities, and harvest VIX contango when the setup looks good.

The grid search was small, used t+1 execution, and applied simple costs. No VIX borrow modeling yet—that would come later, unfortunately for the initial results.

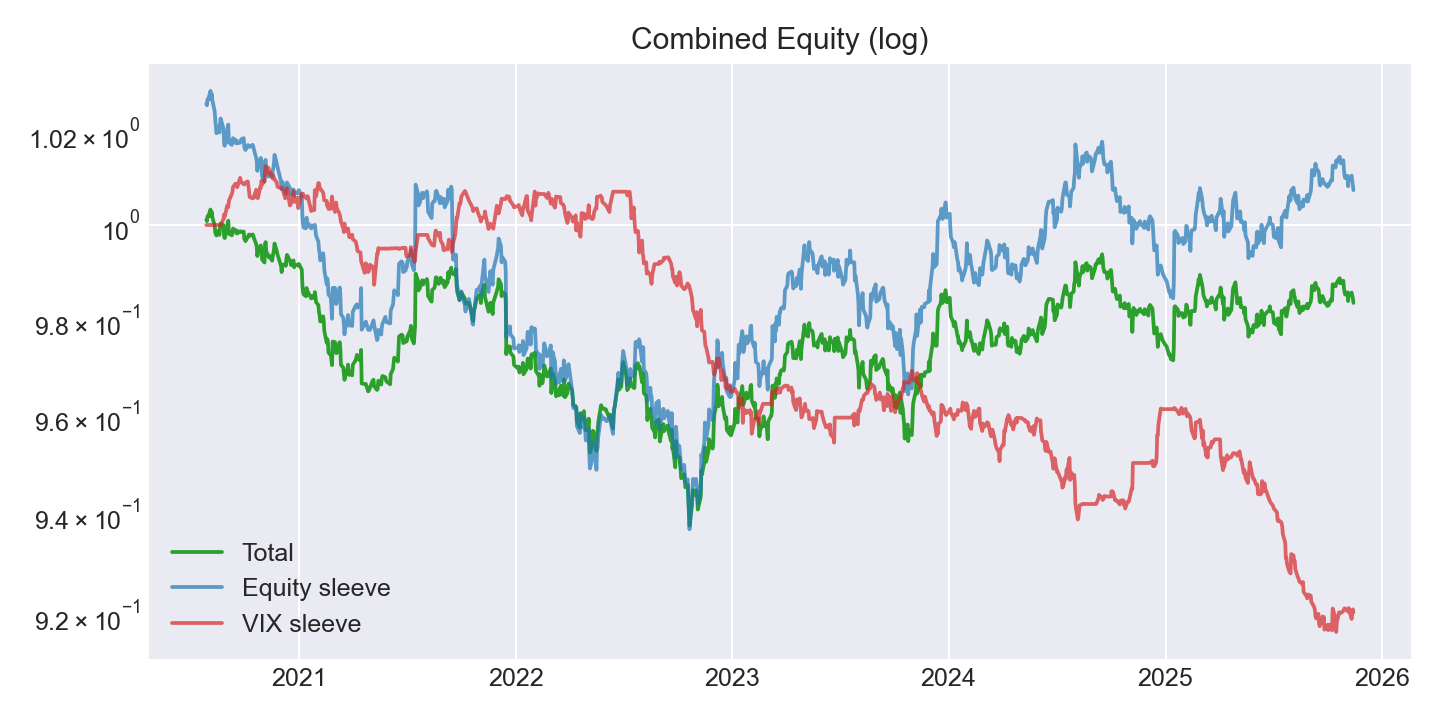

The Initial Backtest

First pass with split-adjusted VIX data and fresh FRED series:

Total return: +2,789.98% over 5.31 years

CAGR: 88.51%

Sharpe: 0.630

Max drawdown: -12.74%

Best parameters found: 10/40 EMAs, 0.2 TLT hedge ratio, VIX entry at 1.0σ / exit at 0.3σ, 20% VIX scaling, 80/20 equity/VIX weights.

The sleeve breakdown: equity Sharpe -0.169, VIX sleeve Sharpe 0.632.

This looked exceptional. It also looked suspicious.

Data Hygiene Check

Before celebrating, I verified the basics:

SPY/TLT/VIXY/VIXM CSVs: split-adjusted, sorted, deduplicated, ISO dates

Date ranges: SPY from 2016, TLT from late 2015, VIXY/VIXM from mid-2020

Macro data: T10Y2Y daily, PAYEMS/CPI monthly

No duplicate dates found

The data was clean. The problem wasn’t there.

Decomposition

Breaking it apart:

Equity sleeve alone (macro filters + SPY/EMA): Sharpe 0.44, CAGR ~0.57%, total return ~5.8% over 9.9 years

VIX sleeve alone: Sharpe 0.63, total return ~+834x over 5.3 years

Combined result: almost entirely driven by VIX

The equity sleeve was doing very little. The VIX sleeve was doing everything. That’s already a red flag — 834x returns from short-vol carry should not survive contact with reality.

Sanity Checks

I added a 15% annual borrow cost to the VIX sleeve. Total return dropped to +25.2x, Sharpe stayed around 0.62.

Still too high. Borrow alone wasn’t the issue.

Why ROI Was Inflated

Five problems:

VIX sleeve dominated and used 2020–2025 only. Short-vol contango in that window drove massive compounded returns. No stress periods from 2018 or 2015 in the data.

No release-lag modeling for macro series. The signals joined on observation dates, not release dates. This created potential look-ahead bias—using information before it would be tradable in real time.

Minimal costs. No realistic ETN borrow (20–30% annually), no meaningful slippage (5–10 bps one-way), no term-structure decay haircut on long VIX exposure.

Limited history. VIXY/VIXM only go back to mid-2020. Missing critical regime changes and drawdown periods.

Unbounded VIX exposure. No vol targeting, no leverage cap, no position limits.

The backtest had inflated returns because it was trading in a dream world.

Fixing the Model

I updated the code to add realism:

Publication lags for macro data: PAYEMS/CPI shifted by 15 days, slope by 1 day, forward-filled to daily frequency

Price-based EMAs: Computed on price rather than return cumprod to avoid indicator drift

Vol-targeted VIX sleeve: Annual vol target (10%), maximum leverage cap (1.0x), borrow cost (30%/year), slippage (20 bps round-trip)

New grid parameters: same EMA ranges, added vol targeting and cost parameters.

The Critical Test

After adding lags, costs, and vol targeting:

Total return: -1.65%

CAGR: -0.31% per year

Sharpe: -0.138

Max drawdown: -6.54%

Sleeve Sharpes: equity 0.018, VIX -1.166

The previously huge ROI was almost entirely from an unconstrained VIX sleeve operating in a favorable window with unrealistic assumptions. After adding proper constraints, the VIX alpha turned negative and the combined strategy lost money.

From +2,789% to -1.65%. That’s what realism costs.

Attempting Recovery

I tried three mitigations:

Softer costs but still realistic: 20% borrow, 10 bps slippage, 15% vol target

Wider VIX entry/exit bands: Higher thresholds, tighter max exposure (0.5x)

Vol-targeted equity sleeve: 10–12% annual vol target, 1.1–1.2x max leverage

Ran a grid of conservative configs.

Best result:

20/60 EMAs, 10% equity vol target, 1.1x max leverage, 0.25 TLT hedge

VIX: 1.3σ entry / 0.5σ exit, 12% vol target, 0.5x max leverage, 15% borrow, 10 bps slippage

Weights: 92% equity, 8% VIX

Total return: +0.08%, CAGR +0.02%/year, Sharpe 0.024

Max drawdown: -7.84%

Sleeves: equity Sharpe 0.047, VIX Sharpe -0.668

Still not good. The VIX sleeve remained negative Sharpe even with lighter costs.

Equity-Only Config

I tried turning VIX off entirely.

Best equity-only result:

10/40 EMAs, 12% vol target, 1.2x max leverage, 0.1 TLT hedge, no VIX

Total return: +0.53%, CAGR +0.10%/year, Sharpe 0.076

Max drawdown: -3.74% over 5.30 years

Adding a tiny VIX sleeve (5% weight, high thresholds, capped leverage) didn’t beat this.

Conclusion

With realistic publication lags and transaction costs, this macro + SPY/TLT sleeve produces low returns and low Sharpe. The VIX sleeve adds no value—it’s either massively inflated under dream assumptions or negative Sharpe under realistic ones.

The initial 88% CAGR was a measurement artifact, not alpha.

To pursue higher Sharpe or meaningful ROI, I’d need a different alpha source: stronger trend/momentum signals, broader asset mixes (QQQ/TLT rotation, cross-asset carry), or alternative risk overlays beyond the current macro filters. The macro term-structure idea doesn’t survive contact with realistic costs and proper data handling.

Sometimes the answer is “this doesn’t work.” That’s still a result.

The information presented in Math & Markets is not investment or financial advice and should not be construed as such.