Revisiting the Dual Allocator Strategy with Claude: Better Returns, Lower Risk

Part 27 is redesigning an improved leveraged dual allocator strategy from scratch

This is part 27 of my series — Building & Scaling Algorithmic Trading Strategies

Background

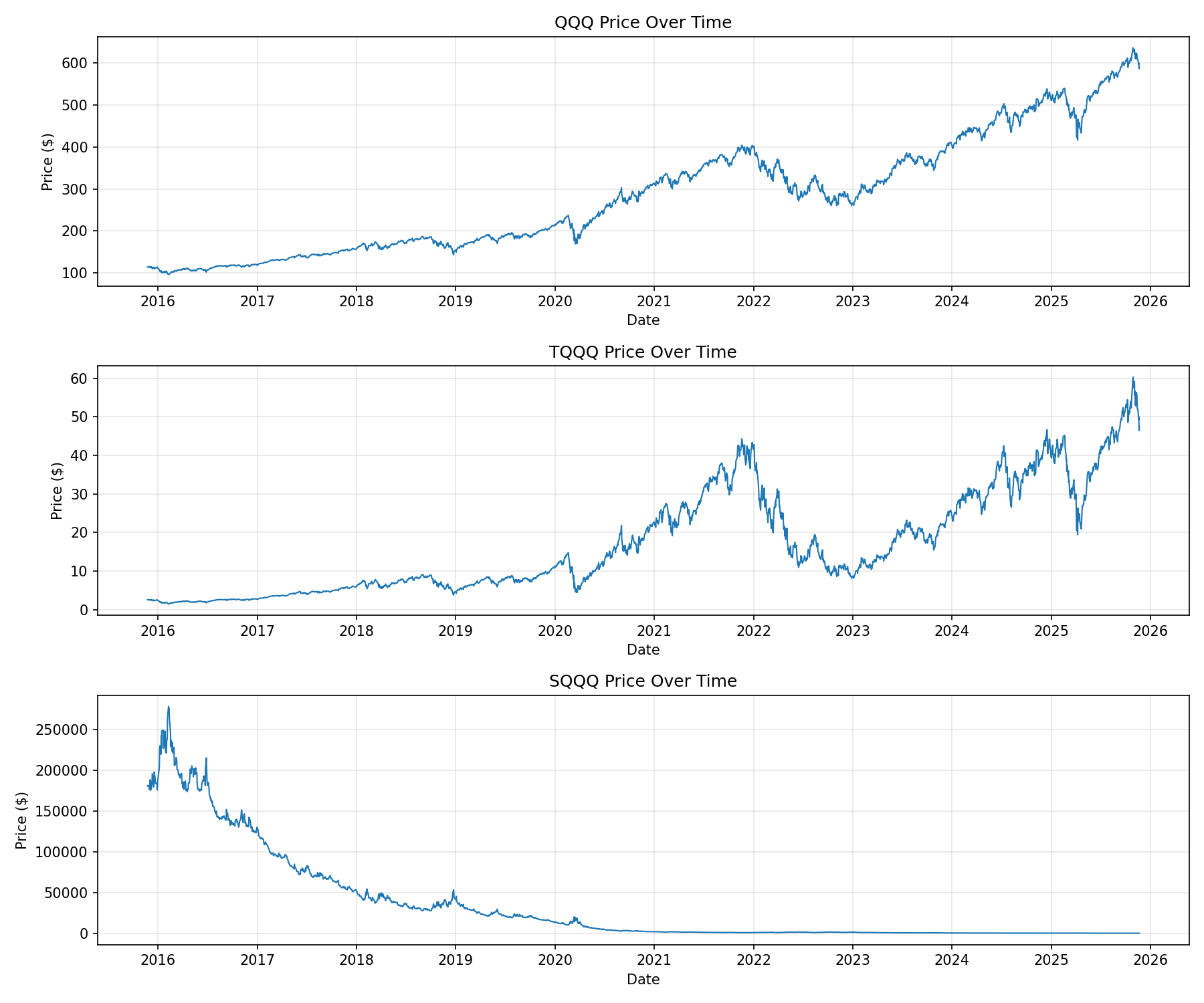

When I first embarked on this project, I started with a tactical long/short dual allocation strategy with leveraged ETFs—specifically TQQQ (3x leveraged QQQ) and its inverse counterpart SQQQ. The goal was simple: capture the explosive upside of leveraged tech exposure while avoiding the soul-crushing drawdowns that come with it.

When I pruned the strategies for production deployment, this was the one that was in the “maybe” bucket. So today, I wanted to revisit this strategy with a fresh perspective and some help from Claude.

Without much further ado, here’s V2 of the long/short Dual Allocator.

The Core Concept

The QQQ Dual Allocator Strategy dynamically shifts between four positions based on trend strength and momentum:

TQQQ (3x long): Maximum bullish exposure when trends are strong

QQQ (1x long): Moderate bullish exposure during neutral conditions

CASH: Capital preservation when signals are unclear

SQQQ (3x short): Hedging or profiting during downtrends

Rather than riding the TQQQ roller coaster all the way down during market crashes, the strategy aims to step aside or even profit from the decline.

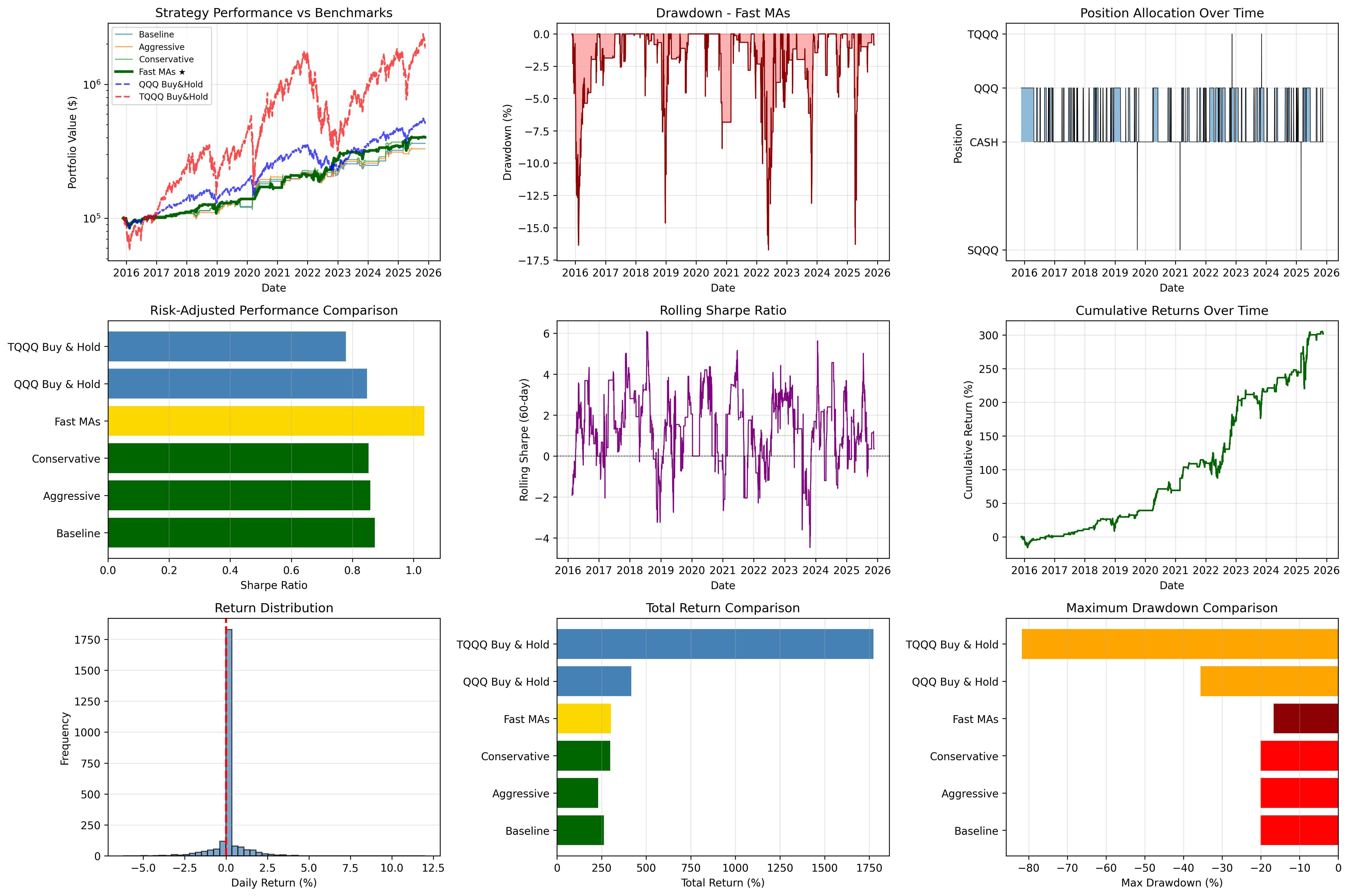

The Results: Fast MAs Configuration Wins

After testing multiple parameter sets, the Fast Moving Averages configuration emerged as the clear winner:

Performance Highlights

Total Return: 301.92% (quadrupling your money over 10 years)

CAGR: 14.93%

Sharpe Ratio: 1.035 ⭐ (the highest among all tested strategies)

Max Drawdown: -16.72% (dramatically better than the -81.75% TQQQ buy-and-hold drawdown)

Head-to-Head Comparison

What the Numbers Tell Us

1. Superior Risk-Adjusted Returns

While TQQQ buy-and-hold delivered astronomical raw returns (1,773%), its Sharpe ratio of 0.779 reveals the hidden cost: extreme volatility and stress. The Fast MAs strategy achieved a Sharpe ratio of 1.035—meaning you’re getting significantly more return per unit of risk taken.

Even compared to vanilla QQQ (which had strong absolute returns), the Fast MAs strategy wins on a risk-adjusted basis.

2. Drawdown Protection That Actually Works

The -81.75% drawdown on TQQQ isn’t just a number—it represents a portfolio value drop from $100,000 to $18,250. Most investors would have capitulated long before the recovery.

By contrast, the Fast MAs strategy’s worst drawdown was just -16.72%. That’s the difference between losing sleep and sleeping soundly during market turmoil.

3. The Sweet Spot Between Aggression and Defense

The beauty of this strategy is that it doesn’t sacrifice too much upside for the downside protection. With a 301.92% total return, you’re still capturing the majority of the bull market gains while avoiding the devastating losses.

Why This Matters

Leveraged ETFs like TQQQ are often dismissed as trading instruments unsuitable for longer-term strategies due to volatility decay and massive drawdowns. And they’re right—if you buy and hold blindly.

But this analysis demonstrates that with intelligent trend-following and dynamic position sizing, you can harness the power of leverage while keeping risk in check. The Fast MAs configuration proves that tactical allocation isn’t just about avoiding losses—it’s about optimizing the risk-return tradeoff.

Technical Notes

One interesting challenge in this analysis was handling SQQQ’s reverse splits. Rather than trying to adjust for corporate actions, I switched to a returns-based backtesting approach, which provides a cleaner and more accurate picture of what an investor would have actually experienced.

The Bottom Line

The QQQ Dual Allocator Strategy, particularly with Fast Moving Averages, represents a viable strategy.

Is it perfect? No. Does it require active monitoring and rebalancing? Yes. But it does provide better risk-adjusted returns over the long term.

Leveraged ETFs carry significant risks and may not be suitable for all investors. The information presented in Math & Markets is not investment or financial advice and should not be construed as such.