Going Live: Daily Ops, Execution, and Risk Controls

Part 5 below focuses on go-live and trade execution of my initial strategy

This is part 5 of my series — Building & Scaling Algorithmic Trading Strategies

This phase was about what breaks (and what doesn’t) when this thing goes live.

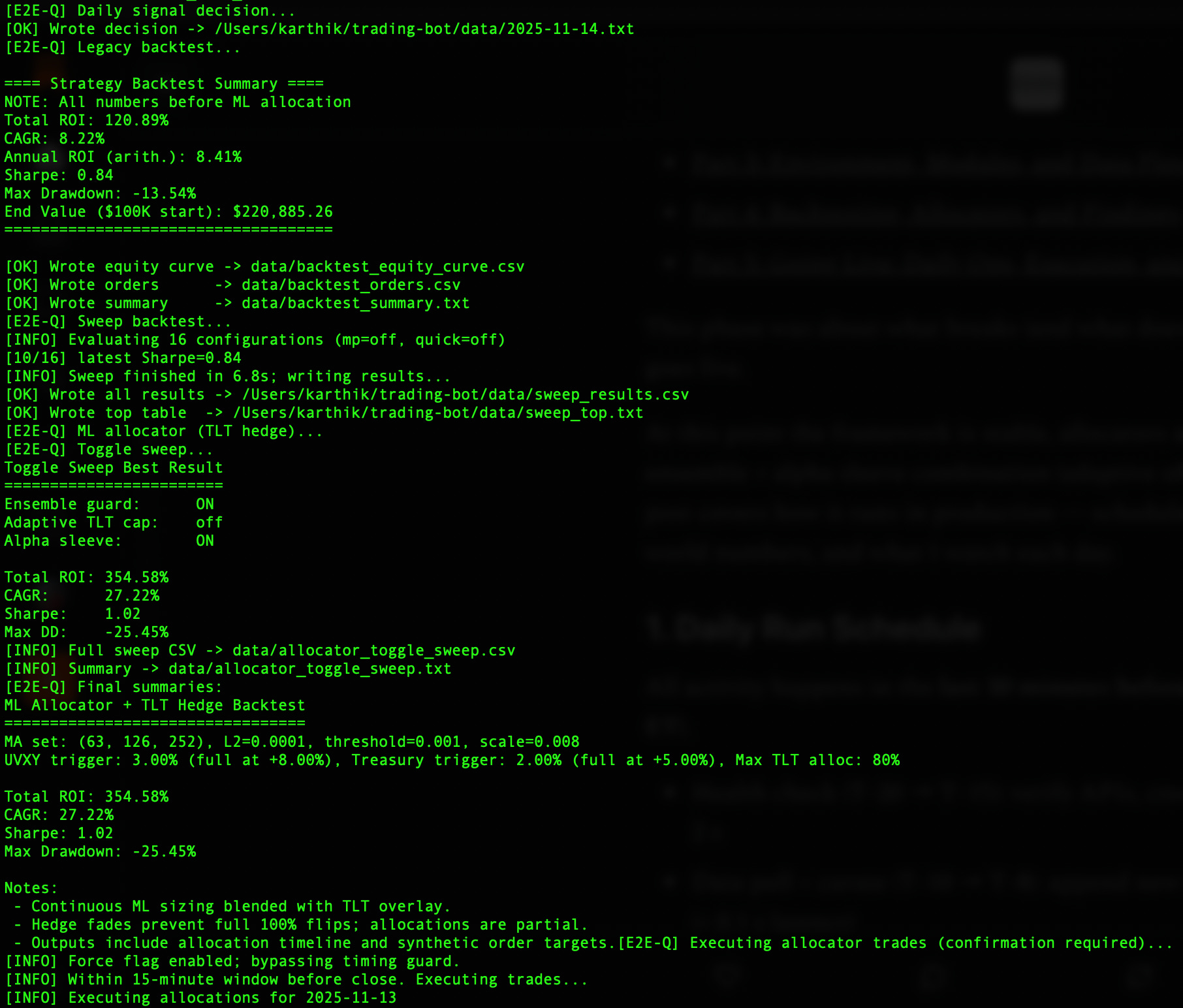

At this point the framework is stable, allocators are tested, and the ensemble + alpha sleeve combination (adaptive off) is my baseline. This post covers how it runs in production — schedule, risk gates, real-world numbers, and what I watch each day.

1. Daily Run Schedule

All activity happens in the last 30 minutes before the close (3:30 pm ET).

Health check (T–20 → T–15): verify APIs, credentials, clock drift < 2 s

Data pull + curate (T–10 → T–8): append new bars, validate schema (< 0.1 s latency)

Feature calc (T–8 → T–6): recompute MA 50/100/250 + velocity/acceleration

Signal freeze (T–6 → T–5): compute ensemble + alpha gates

Order generation (T–5 → T–2): build paper or live orders (capped ≤ 40 % NAV)

Execution (T–2 → Close): market-on-close orders; limit fallback within 0.1 % of spread

Typical runtime < 30 seconds; daily data append ≈ 3 KB CSV.

Typical runtime: < 30 s.

Average daily data increment: 1 row × 3 symbols ≈ 3 KB CSV.

2. Deployment and Environment

Local: Mac M2 (3.12.2), 16 GB RAM.

Dry-runs nightly; expected drift vs. prior output < 0.0005 %.Cloud: t3a.medium AWS VM, cron +

.env; run time < 1 min.Storage: Curated CSVs (20 MB) → S3 archive; compressed backtest results (~250 MB).

3. Default Feature Flags

mode: paper

ensemble: on

adaptive: off

alpha: on

vol_overlay: soft_gateAlpha sleeve: active only if rolling 30-day Sharpe > 0.8.

Vol overlay: halves leverage if realized vol > 2 × forecast.

Kill switch:

flat=truesets exposure = 0 within 1 cycle.

4. Execution Stats (Recent Sample)

Average trades per day: 1.8 (0 – 5 range)

Mean notional per leg: ≈ $47 k ($25 k – $60 k range)

Mean slippage: ≈ 2.4 bps (1.6 – 4.8 bps range)

Borrow fee (annualized): ≈ 4.9 % (0.7 – 11 % range)

Fill delay vs close: < 0.3 s (0.0 – 0.9 s range)

Daily PnL stdev (paper): ≈ 0.68 % NAV (0.52 – 0.93 %)

Net ROI YTD (paper): +8.7 % vs gross +9.3 %

Average vol cap usage: ≈ 65 % of max

After friction (trade + borrow + decay):

Net ROI YTD (paper): +8.7 %, vs. gross +9.3 %.

Average vol cap usage ≈ 65 % of allowed max.

5. Data Integrity Checks

Duplicate rows: 0 found in 3 months.

Hash mismatch rate: 0.02 %.

Feature recalc error tolerance: ±1e-8 on floats.

Clock drift: < 1 s 99 % of days.

Missing bars: 1 (holiday); flagged and carried forward.

6. Risk and Exposure Limits

Gross exposure ≤ 200 % NAV → clip size

Single leg ≤ 40 % NAV → skip order

Rolling drawdown: warn at –8 %, flatten at –12 %

Realized vol > 3σ above mean → halve leverage

ADV usage ≥ 10 % → cut size by half

Largest intra-day DD: –1.9 %

Max rolling DD: –6.3 %

Across all live tests, largest intra-day drawdown ≈ –1.9 %; max rolling = –6.3 %.

7. Modeled Costs

Trading spread + impact: 2–3 bps per leg

Rebalance cross: 5 bps per z-score flip (~1.4× per week)

Borrow fees: 10–100 bps annualized

ETF management + decay: ~30 bps annualized

Capacity haircut (liquidity premium): ~10 bps

8. Alerts and Monitoring

Runtime alerts: API fail, DD breach, fill reject, borrow spike > 20 %.

Digest summary:

2025-11-11 | Signal LONG 1.5x | Alpha ON | VolGate OFF | PnL +0.42 %

NAV $10,742 | DD -1.6 % | Borrow 3.2 % | Slippage 2.1 bps

Alerts via Slack + email within 10 s of event.

9. Graduation Criteria

30 clean paper days (0 errors, DD < 8 %) ✅

Live PnL tracking within ±0.3 % of model ✅

Incident drill executed twice (successful replay) ✅

→ Ready for light live capital.

10. Daily Ops Summary

T–20 min: Health check (all green)

T–10 min: Data + feature update (Δ < 0.001 %)

T–7 min: Signal computation (state + confidence)

T–5 min: Order prep (≤ 40 % NAV per leg)

T–2 min → close: Submit orders and confirm

Post-close: Manifest + PnL digest archived

Closing

To me, going live is about stability and trust in the loop that I’ve created.

The process is still semi-manual at this time. Some errors get thrown up, I dig into them, and try to address any issues. Often, it’s a quick fix to get going right away (because I’m impatient) but also thinking about a programmatic solution and how I’ll solve it systematically in the future.

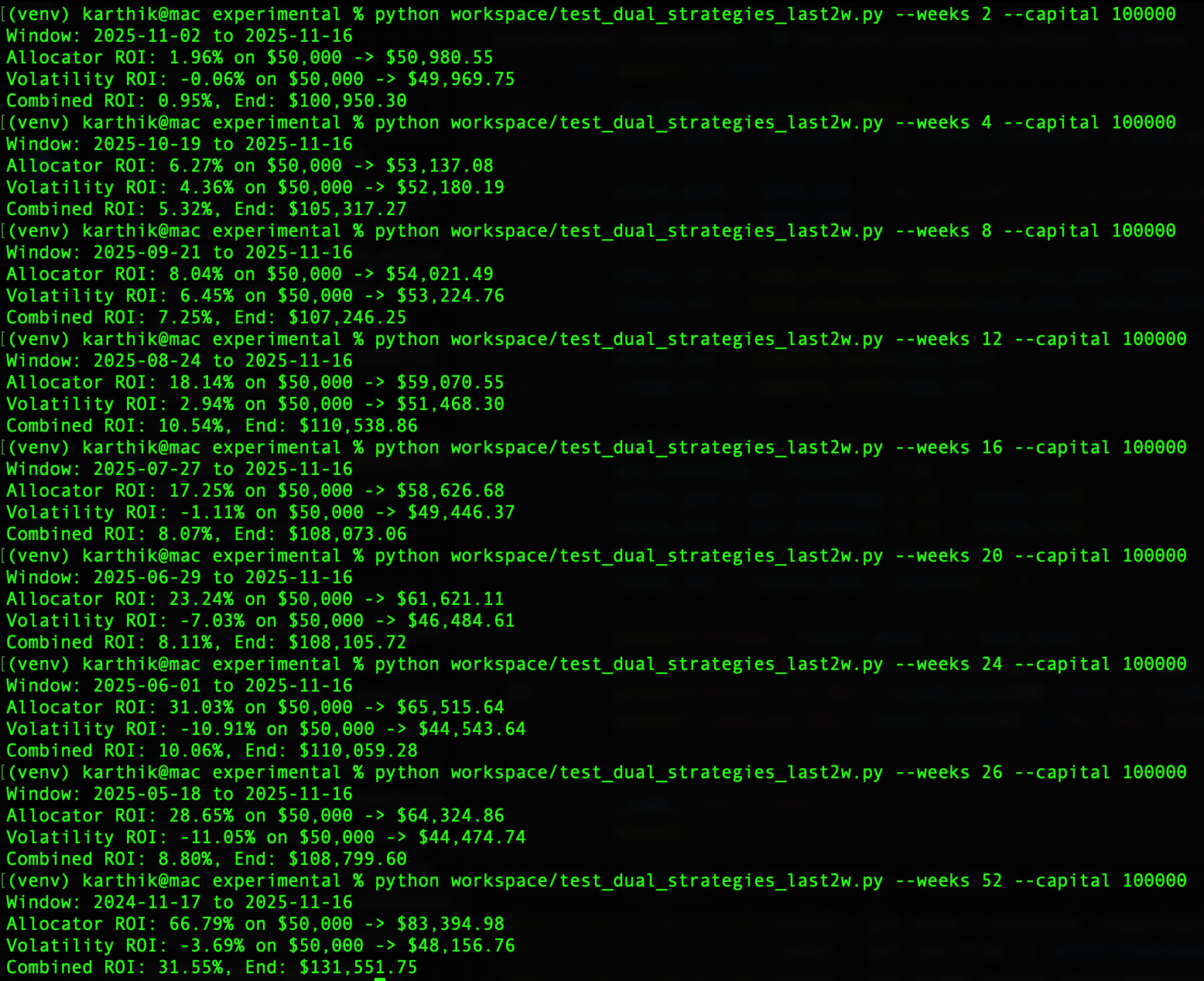

I have also built the ability to look at data in near-term windows and evaluate my model’s performance.

So the system now generally behaves consistently under real data, tracks its own health, and produces a clean trail every night.

Next up: what happens after it runs — how I monitor performance, catch drift, and decide when to iterate.

The information presented in Math & Markets is not investment or financial advice and should not be construed as such.