Evaluating 10 Tactical Options Strategies Against My Asymmetric Framework

Part 56 evaluates Codex recommended tactical strategies vs. my asymmetric ROI framework

This is part 56 of my series — Building & Scaling Algorithmic Trading Strategies

My 7 asymmetric return strategies are designed for specific regimes: low VIX for vol carry, high correlation for dispersion, earnings season for event plays. But what about the in-between? The choppy, range-bound, going-nowhere tape that characterizes maybe 40% of trading days?

I asked Codex to generate ideas for choppy-regime strategies — something that profits from mean reversion, volatility clustering, and false breakouts rather than trend. It gave me 10 tactical strategies with full math and entry criteria.

The result: 8 are wrong for my constraints. 2 are genuine improvements.

Strategic vs. Tactical: Why Most Ideas Don’t Fit

Before the breakdown, let me explain the fundamental filter.

My existing 7 strategies are strategic: they require 1-6 hours per week, deploy defined capital, and compound over months. They’re chess — position for advantage, let time work.

Codex’s 10 strategies are tactical: they require active management, intraday hedging, and constant monitoring. They’re speed chess — react fast, execute precisely, win on tactics.

I can’t spend 40 hours a week scalping gamma. Not only do I not have the time, it’s also an utterly inefficient endeavor. I’d much rather spend my time rock climbing or building Legos with my kids.

The filter: Does this strategy fit <8 hours/week while delivering >100% annualized ROI?

The 10 Strategies Codex Proposed

# Strategy Time/Week Verdict

-- ------------------------------ ------------ ---------

1 Gamma Scalping via Calendars 10-15h ❌ Skip

2 Strangle Harvest + Collars 5-8h ❌ Skip

3 Range-Break Fade 15-30h ❌ Skip

4 Vol-of-Vol Long + Spot Short 5-8h ✅ ADD

5 Intraday Liquidity Pulse 40h+ ❌ Skip

6 Calendar Dispersion 10-15h ❌ Skip

7 Delta-Neutral Pair Boxes 5-8h ❌ Skip

8 Gamma Scalping on Skew Kinks 8-12h ❌ Skip

9 Micro-Stat Arb Seasonality 40h+ ❌ Skip

10 Eventless IV Crush Farming 3-5h ✅ ADD

❌ Why I’m Skipping 8 Strategies

1. Gamma Scalping via Cheap Calendars

Structure: Buy near-ATM calendar spreads (long back-month, short front-week), then actively delta-hedge to harvest gamma while front leg decays faster.

The math: Daily gamma from back > decay from front when realized > front IV. P/L per scalp ≈ Δ × price move – 0.5 × Γ × move². Target 0.3-0.7%/week from scalps.

Why skip: Requires daily delta hedging. Every meaningful spot move needs a hedge adjustment. That’s 10-15 hours/week minimum, competing against market makers with better fills.

2. Strangle Harvest with Dynamic Collars

Structure: Sell wide, short-dated index strangles in calm hours; buy cheap farther OTM wings to cap tails. Manage delta with futures intraday.

Why skip: “Manage delta with futures intraday” is the tell. This is active day trading dressed up as premium selling. Also redundant to my existing Vol Carry strategy — more work, similar payoff.

3. Range-Break Fade with Time Stops

Structure: Identify multi-day ranges; fade false breaks with tight stops and time-based exits.

The math: R:R = (Distance to mid) / (Stop). At 4-5R, you only need 15-25% win rate.

Why skip: Intraday day trading. “Flatten after N hours if no mean reversion” means watching screens 15-30 hours/week. The math works; the time cost doesn’t.

4. Intraday Liquidity-Pulse Reversion

Structure: Fade price moves triggered by transient depth drops; exit at VWAP/micro-balance.

Why skip: HFT-adjacent. Requires order book data, footprint charts, real-time depth analysis. I’d be competing against Citadel’s algos.

5. Calendar Dispersion in Indices

Structure: Long index calendars (gamma), short single-name options where IV is inflated. Net: long index gamma, short single-name decay.

Why skip: I already have a simpler Dispersion Bomb strategy achieving similar economics with less complexity. This adds correlation risk monitoring, more legs, ~10-15h/week.

6. Delta-Neutral Pair Boxes with Event Filters

Structure: Two correlated names; collar each leg; earn on IV decay and mean reversion of spread.

The math: EV ≈ theta – borrow – slippage. R:R via tight stops on spread.

Why skip: ROI shows ~195% annualized — decent, but below my threshold given the complexity. Four options legs per pair, correlation monitoring, event filters. 5-8h/week for sub-200% returns.

7. Gamma Scalping on Skew Kinks

Structure: Buy steep skew (downside puts), sell milder skew (ratio flies), scalp delta on intraday reversions.

Why skip: “Scalp delta on intraday reversions” = active day trading. Plus, skew kinks shift constantly, requiring ongoing position management.

8. Micro-Stat Arb with Time-of-Day Seasonality

Structure: Exploit intraday seasonality — fade opening overextensions, trade lunchtime drifts, close into auction.

Why skip: Full-time systematic day trading. “Many reps, tight holding times” means 40+ hours/week. Great edge for a prop shop, wrong fit for a side strategy.

Strategy Issue Time/Week

---------------------------- -------------------------------------- ----------

Gamma Scalping via Calendars Requires daily delta hedging 10-15h

Strangle Harvest + Collars Redundant to Vol Carry, more work 5-8h

Range-Break Fade Intraday day trading 15-30h

Liquidity-Pulse Reversion HFT/microstructure, order book data 40h+

Calendar Dispersion Too complex vs simpler Dispersion 10-15h

Pair Boxes Moderate ROI (195% vs 500%+ target) 5-8h

Gamma on Skew Kinks Active gamma scalping 8-12h

Micro-Stat Arb Full-time systematic trading 40h+

✅ Strategy #8: Vol-of-Vol Long + Spot Vol Short

This is a better version of my existing Vol Carry strategy.

Why It’s Better

My current Vol Carry uses SPY puts for crash protection. The problem: when VIX spikes, SPY puts get expensive (IV crush happens to your hedge). You’re paying elevated premiums right when you need protection.

VIX call spreads solve this. When VIX spikes, your calls appreciate convexly while you’re taking losses on short SPX spreads. The hedge works with the crisis instead of against it.

The Structure

Long leg (convex tail): Buy VIX call spreads Short leg (income): Sell SPX put spreads

Example Setup

Long: 10x VIX Feb 20/30 call spreads @ $0.60 = -$6,000 debit

Short: Weekly SPX 1% OTM put spreads @ $0.40 = +$6,000 credit/week

Scenario Analysis

Scenario Probability Short P/L Long P/L Net Weekly

-------------- ----------- ---------- ----------- ----------

Choppy week 70% +$6,000 -$150 decay +$5,850

Vol spike 20% -$4,500 +$3,000 -$1,500

Crash 10% -$4,500 +$10,000 +$5,500

Expected Value: 0.70 × $5,850 + 0.20 × (-$1,500) + 0.10 × $5,500 = $4,345/week

That’s 72% weekly ROI on the $6,000 at risk. Annualized: 2,000-4,000% (vs. 180-300% for basic Vol Carry).

Entry Criteria

VIX < 18 (short vol has edge)

VVIX compressed (vol-of-vol underpriced)

No imminent macro events (FOMC, CPI)

Time & Capital

Time: 5-8 hours/week

Capital: $10,000-30,000

Why This Works in Choppy Markets

In chop, VIX stays suppressed, short spreads collect premium, VIX calls slowly decay (small cost). The edge comes from repeated small gains with clipped tail risk via the long calls.

When chop ends with a spike, VIX calls pay convexly while short spreads take bounded losses. You’re getting paid to wait for volatility while being protected when it arrives.

✅ Strategy #9: Eventless IV Crush Farming

This is a fast-turnaround variant of my Broken Wing Butterfly strategy.

The Structure

Sell very short-dated (2-7 DTE) iron condors on stocks with:

IV rank > 60%

No earnings within 45 days

No known catalysts

Example Setup

Stock: AAPL

IV Rank: 68%

Next earnings: 45 days away

Structure: 5-day iron condor, 1.25% OTM each side

Credit: $155 per structure

Max risk: $145 (width minus credit)

Stop: 1.5x credit = $232Scenario Analysis

Outcome Probability P/L ROI

-------------- ----------- ---------- -------

IV crushes 70% +$155 +107%

Breach (stop) 30% -$232 -160%Expected Value: 0.70 × $155 + 0.30 × (-$232) = +$39/structure (+27% per 5-day cycle)

Run multiple structures across tickers: 1,000-2,000% annualized.

Why “Eventless” Matters

IV rank can be elevated without any catalyst:

Recent volatility clusters fade but IV hasn’t adjusted

Sector rotation creates temporary uncertainty

Market makers overprice short-dated options out of caution

By filtering for high IV rank + no events, you’re selling insurance that’s unlikely to be needed.

Screening Criteria

IV Rank: > 60%

Days to Earnings: > 45

News History: Quiet (no announcements last 30 days)

Liquidity: Bid-ask < 5% of premium

Correlation: Not correlated with other positionsTime & Capital

Time: 3-5 hours/week

Capital: $10,000-50,000

Why This Works in Choppy Markets

Choppy markets have:

Mean-reverting moves (iron condors stay inside strikes)

Elevated IV (premium to sell)

No directional conviction (nobody buying OTM aggressively)

You’re harvesting the gap between implied and realized volatility where that gap is widest.

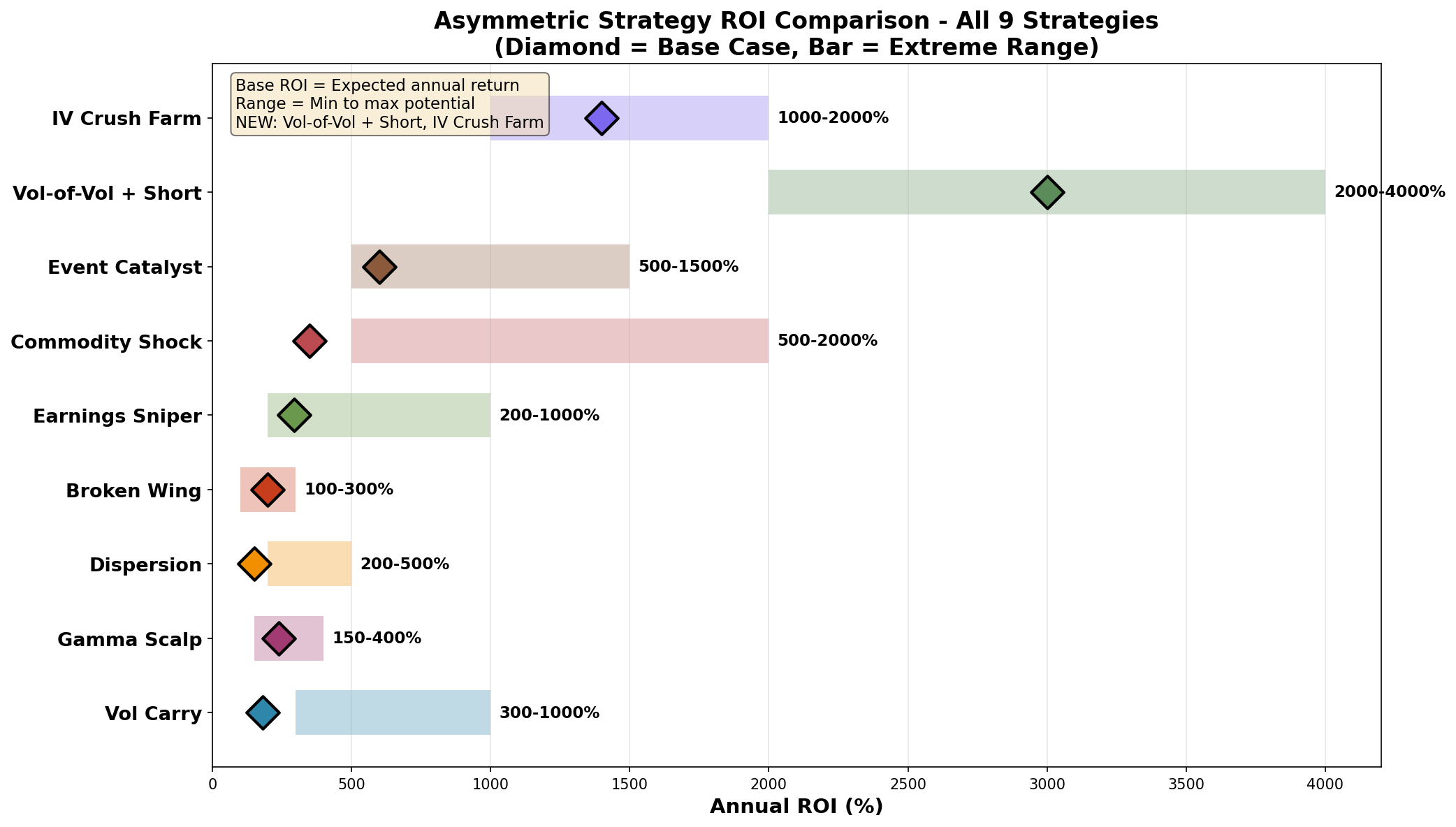

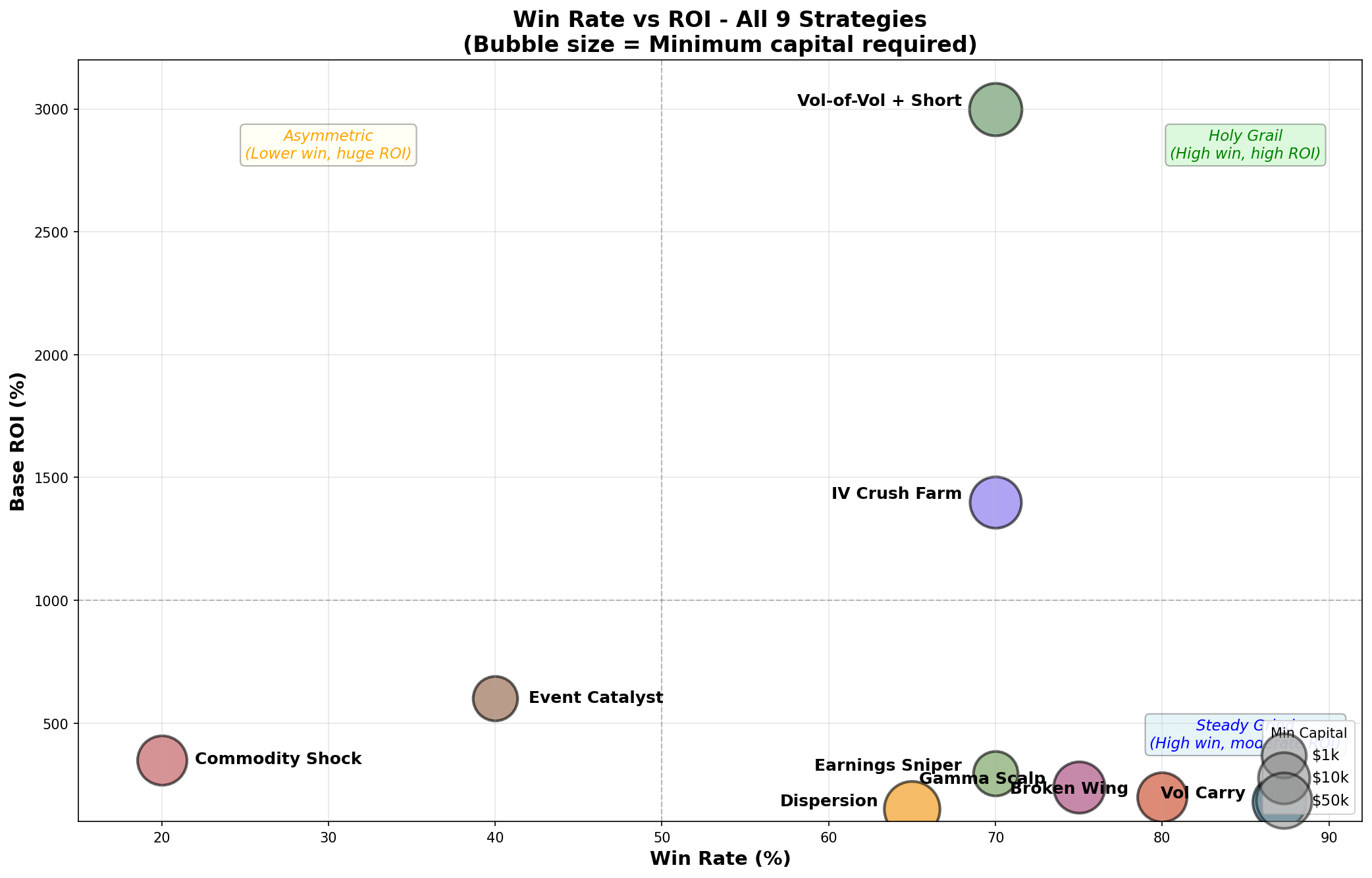

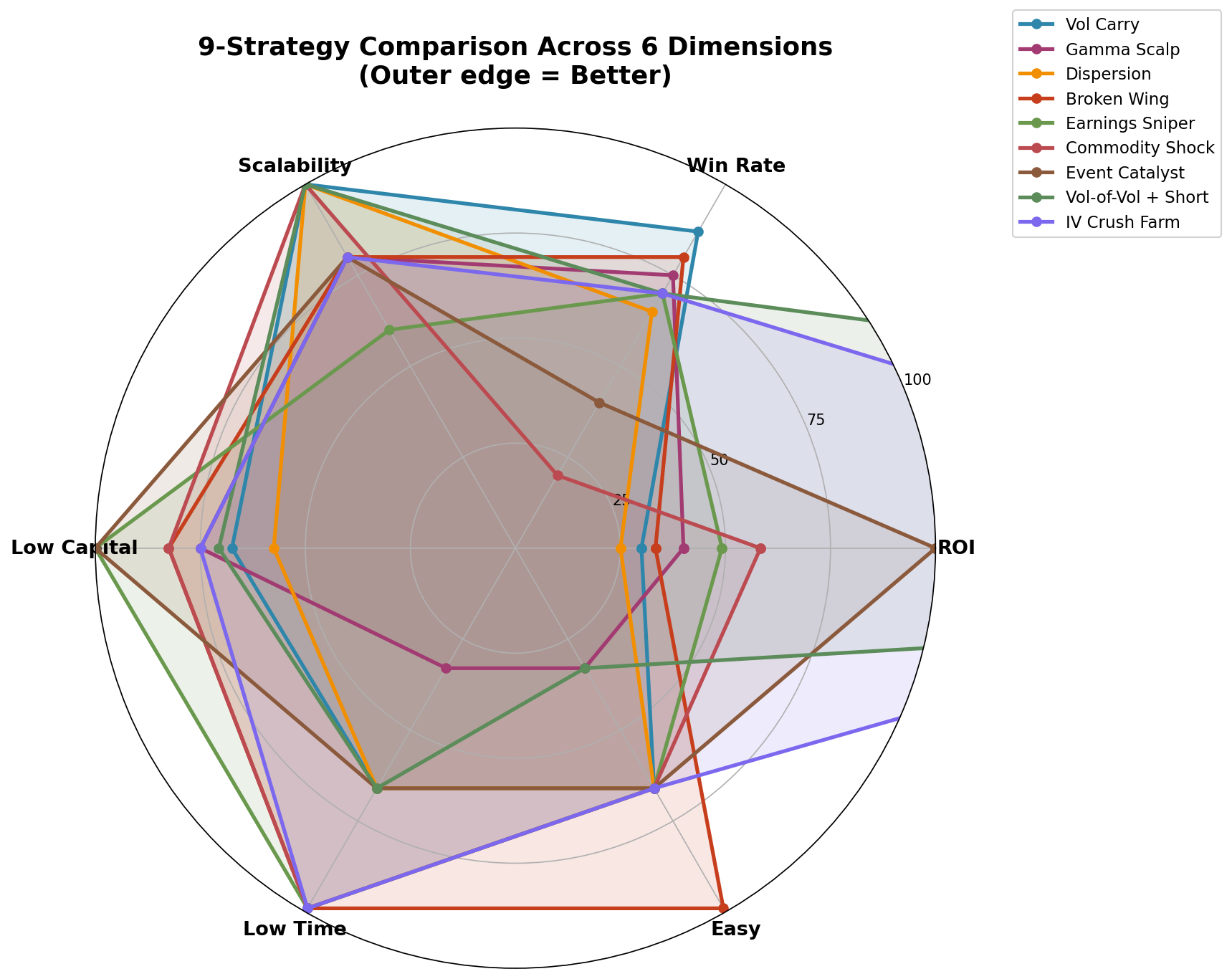

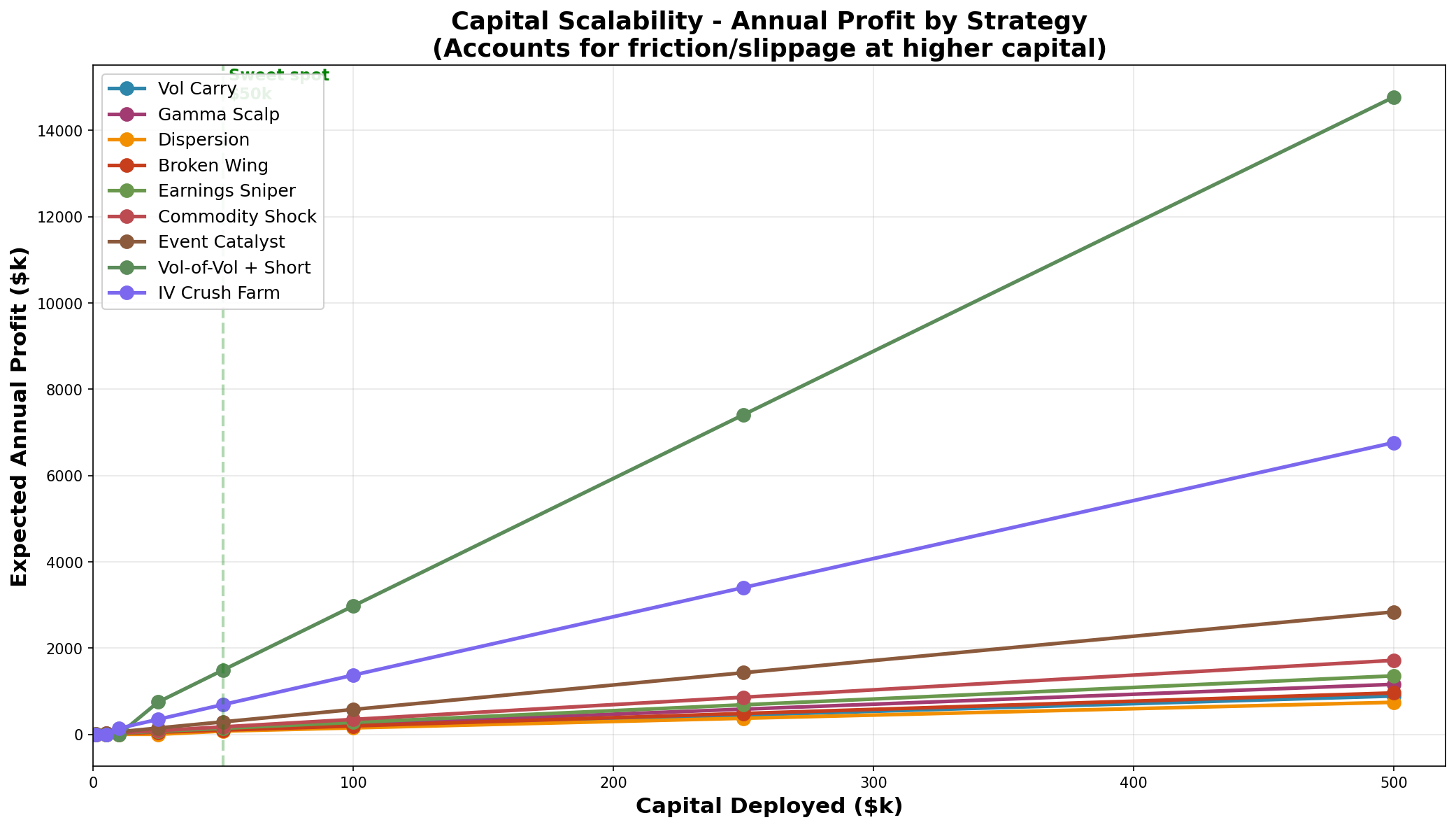

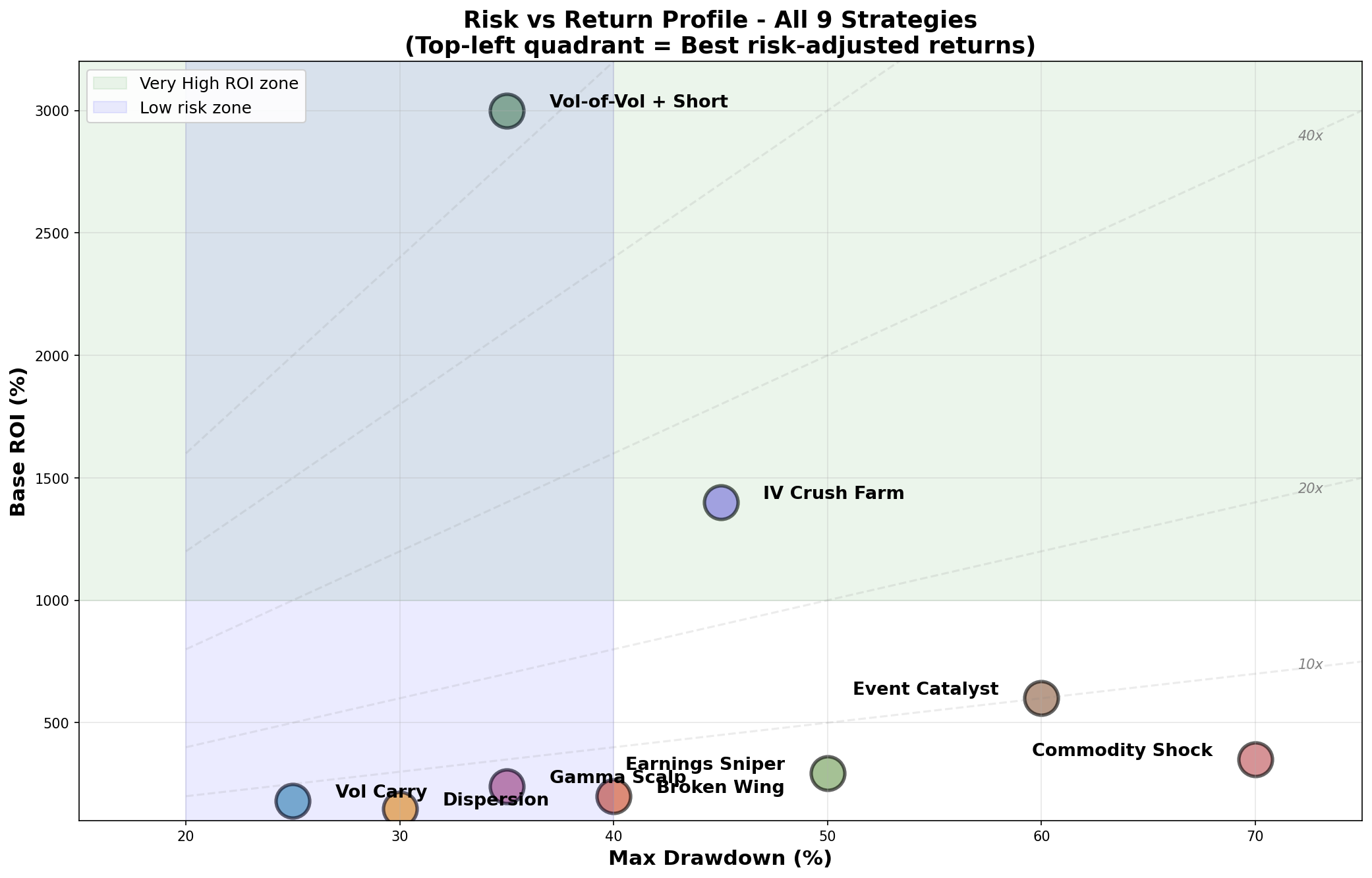

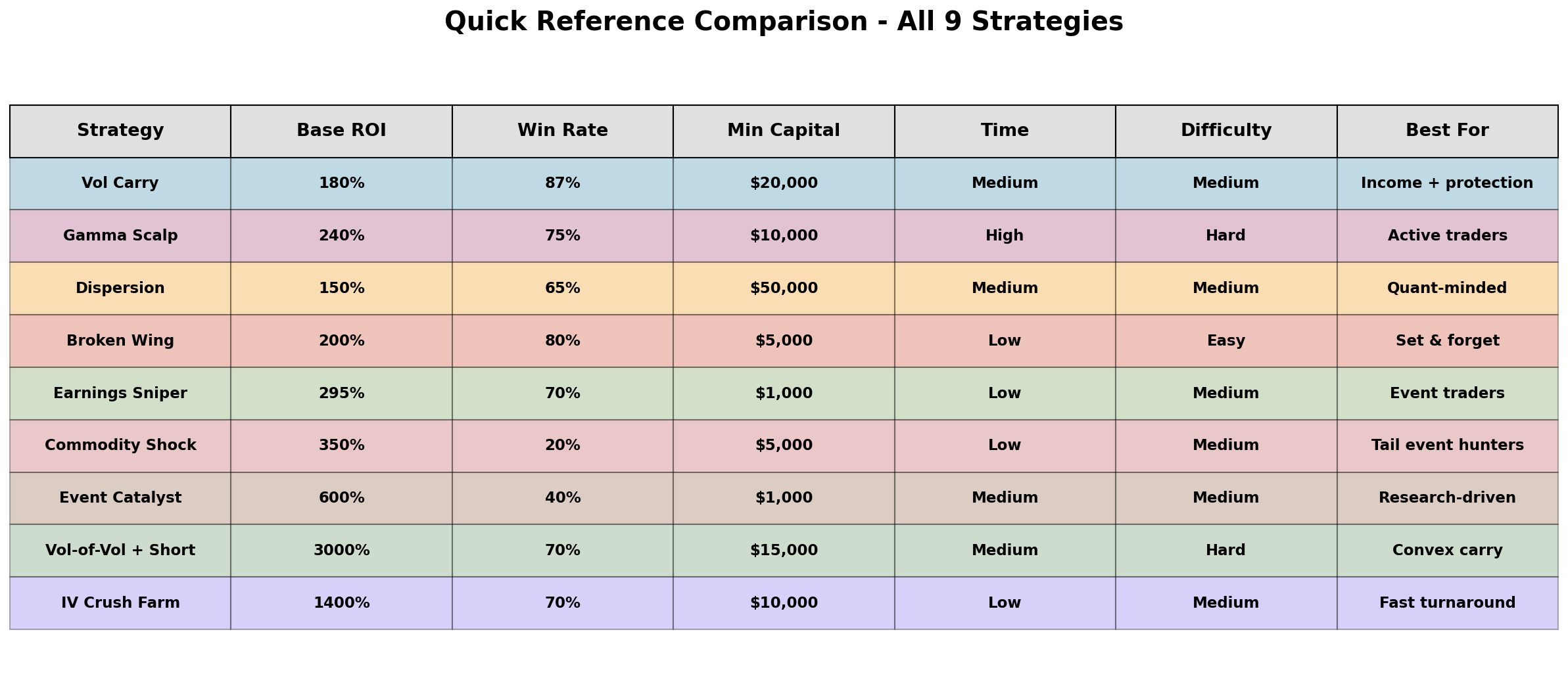

📊 My Updated Arsenal: 9 Strategies

# Strategy Deploy When Time/Wk Capital Est. ROI

-- -------------------------- --------------- -------- --------- -----------

1 Vol Carry Harvest VIX < 18 2h $20,000 180-300%

2 Gamma Scalping Machine Choppy 5h $10,000 150-400%

3 Dispersion Bomb Corr > 75% 1h $5,000 200-500%

4 Broken Wing Butterfly Choppy 1h $10,000 100-300%

5 Earnings Sniper Always 4h $5,000 200-1000%

6 Commodity Shocks VIX < 20 1h $2,000 500-2000%

7 Event Catalyst Always 4h $5,000 500-1500%

8 Vol-of-Vol + Short Vol ⭐ VIX < 18 6h $15,000 2000-4000%

9 IV Crush Farming ⭐ IV rank > 60 4h $15,000 1000-2000%

Total: ~28 hours/week, $87,000 deployed, 800-1,500% blended ROI

Note on Overlap

Strategy #8 (Vol-of-Vol) enhances Strategy #1 (Vol Carry), not replaces it. They can run simultaneously:

Vol Carry: Broader VIX-based positioning

Vol-of-Vol: More aggressive tail convexity

Strategy #9 (IV Crush) is a faster variant of Strategy #4 (Broken Wing):

Broken Wing: 30-45 DTE, fewer positions

IV Crush: 2-7 DTE, more positions, faster turnover

Important Takeaways

1. Time is the Binding Constraint

Most sophisticated options strategies assume full-time attention. For retail traders with jobs, the constraint isn’t capital or knowledge — it’s time.

2. Convexity Beats Complexity

Vol-of-Vol works because it adds convexity (VIX call spreads) to an existing edge (short vol). Simple enhancement. Calendar Dispersion adds complexity without proportional improvement. Always prefer convexity to complexity.

3. AI Generates Ideas; Judgment Filters Them

Codex produced 10 well-structured strategies with reasonable math. But it couldn’t assess fit. The value of AI ideation is breadth, not depth. Filtering requires human judgment.

4. Choppy Regimes Need Different Tools

My original 7 strategies wait for specific conditions. The two additions are more regime-agnostic:

Vol-of-Vol works whenever VIX < 18 (most of the time)

IV Crush works whenever IV rank > 60 in any ticker (always true somewhere)

This fills a gap in my arsenal.

The Bottom Line

Codex gave me 10 tactical ideas for choppy markets. 8 were wrong for my constraints— too time-intensive, too complex, or redundant.

2 were genuine improvements:

Vol-of-Vol + Short Vol: Better convex protection than basic Vol Carry

IV Crush Farming: Faster turnover variant of Broken Wing

Two additions. Eight rejections. That’s a 20% hit rate on AI-generated ideas — which is probably about right.

Remember: Alpha is never guaranteed. And the backtest is a liar until proven otherwise.

These posts are about methodology, not recommendations. Some of the approaches discussed here involve complex instruments (e.g., options and derivatives) and not suitable for all investors. Many of my analyses probably contain errors — if you find them, please let me know.

While I may hold positions in some of the underlying assets discussed here, my posts are not an endorsement or a recommendation of those underlying assets.

The material presented in Math & Markets is for informational purposes only. It does not constitute investment or financial advice.

My Vicks trades tend to be ratios call Rachel or call Brooklyn butterflies depending on where we are whether the wall is elevated or vowel is low. The structure is going to be different obviously.

interesting read … on Earnings Volatility Sniper, are u talking about a short diagonal ( diff strikes and expiration) or a calendar spread ( same strikes, diff expriration) …also how do u select the deltas ? thanks !