End In Sight: Separating Signal from Noise

Part 23 is about selecting strategies to promote into production

This is part 23 of my series — Building & Scaling Algorithmic Trading Strategies

I am almost at the end of this phase — I need to step back, consolidate everything I’ve built, and decide which strategies are truly production-worthy, which need more time in the lab, and which should be shelved.

I now have a functioning algorithmic trading stack with multiple sleeves, toggles, and overlays. The goal isn’t having a lot of strategies — rather, it’s having a small set of high-quality, uncorrelated, robust sleeves.

Below is the consolidated assessment, the operational criteria I’m using to pick winners, and the two strategies I’m promoting into production.

“…it comes to be that the soothing light at the end of your tunnel is a freight train coming your way.” — Four Leaf Clover, Metallica

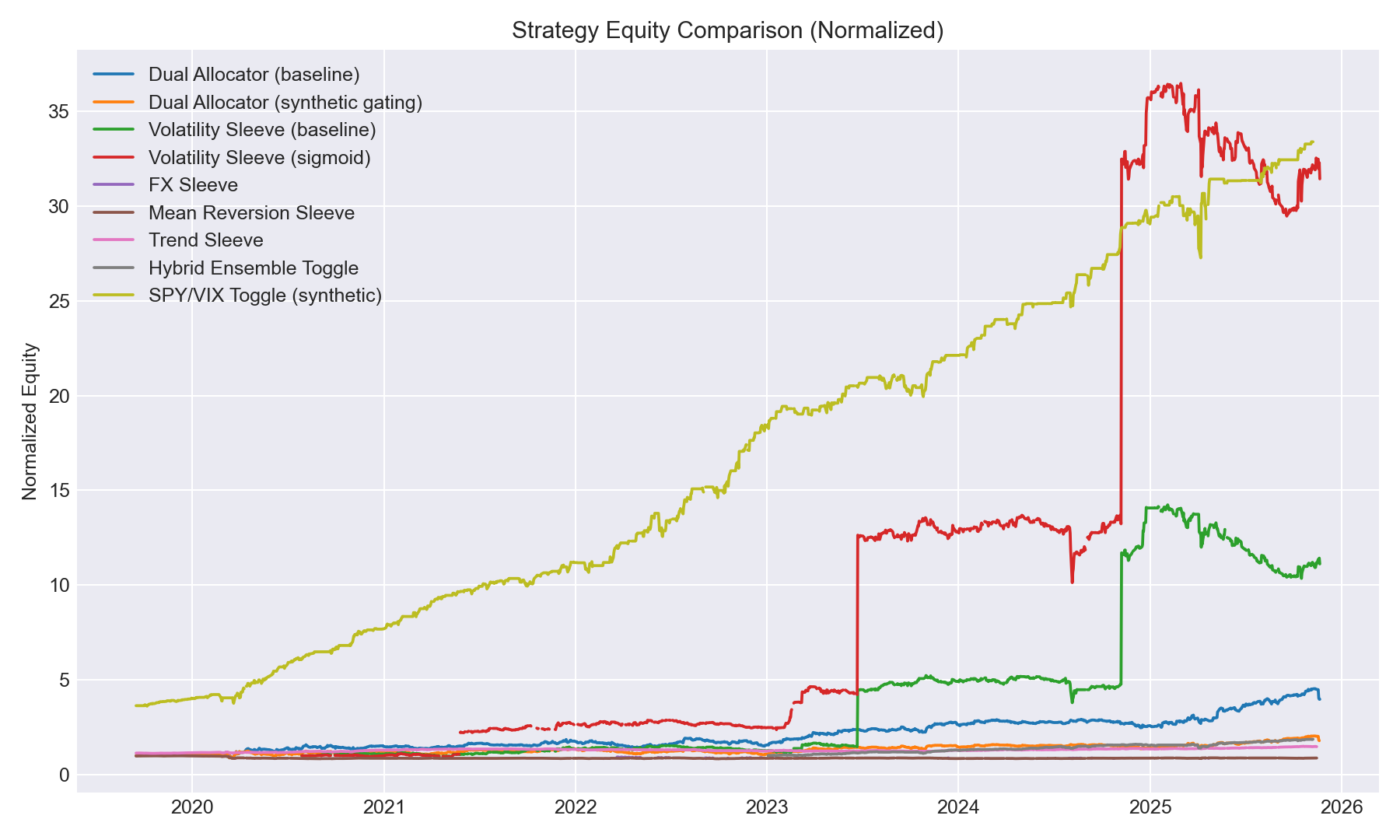

1. Consolidated Performance — What the Data Says

A quick snapshot of all sleeves tested so far:

Dual Allocator (baseline): ROI ~298%, Sharpe ~0.94, DD ~–25%

Dual Gating (SHAP v1): ROI collapsed to ~79%, Sharpe ~0.49

Volatility Sleeve (Sigmoid): ROI ~3,089%, Sharpe ~0.87, DD ~–26%

Volatility Sleeve (Legacy Step): ROI ~1,028%, Sharpe ~0.70

Trend Sleeve: ROI ~48%, Sharpe ~0.85

Hybrid Ensemble Toggle: ROI ~87%, Sharpe ~1.85, DD ~–12%

SPY/VIX Synthetic Toggle: ROI ~3,238%, Sharpe ~2.92, DD ~–10.6%

FX Sleeve: ROI ~–12%, Sharpe ~–0.92

Mean Reversion Sleeve: ROI ~–12%, Sharpe ~–0.27

When visualized together, the strongest performers are obvious: the sigmoid VIX sleeve and the synthetic SPY/VIX toggle tower over the rest in both ROI and risk-adjusted returns.

2. Promotion Decisions

✅ Volatility Sleeve (Sigmoid Sizing)

A direct upgrade with huge improvement and well-behaved risk.

ROI 3,089%

Sharpe 0.87

DD –26%

This will replace the old step-based version after a short burn-in period.

✅ SPY/VIX Synthetic Toggle

Massive Sharpe, strong ROI, low drawdown, independent return stream.

ROI 3,238%

Sharpe 2.92

DD only –10.6%

Needs a 3-month paper-test before going live — but this is by far the most exciting output of Phase 1.

✅ ⚠️ Dual Allocator (Baseline)

Stable, proven core engine with consistent behavior. It’s not retired, but it’s not fully promoted either. I’d say this strategy is on an extended probation.

⚠️ Trend Sleeve

A reliable diversifier with shallow drawdowns and Sharpe ~0.85. Okay-ish. Benched but not fired.

⚠️ Hybrid Ensemble Toggle

Sharpe 1.85 with mild drawdowns. A disciplined overlay rather than a standalone sleeve.

❌ Dual Allocator Gating (SHAP v1)

Sharpe collapsed, ROI cratered. Good concept, but execution isn’t usable yet.

❌ FX Sleeve

Negative ROI and Sharpe. Shelve or rebuild from scratch.

❌ Mean Reversion Sleeve

Also negative — fragile and not worth deploying.

Pending / Monitor

Legacy VIX Step Sleeve: Will fully retire once the sigmoid version passes forward-testing.

Macro/Credit Overlays: Not yet built — these are the entire focus of Phase 2.

What’s Next

My next focus will be building a macro/credit strategy using cross-asset volatility, credit spreads, and macro stress indicators — the missing pillar that rounds out the system.

The information presented in Math & Markets is not investment or financial advice and should not be construed as such.