Building Synthetic SPY: Fake Data to Test Real Strategies

Part 18 is about using synthetic data to test models and build resiliency

This is part 18 of my series — Building & Scaling Algorithmic Trading Strategies

One limitation of any systematic strategy project is that you only get one historical tape to train and validate on. SPY has one path. QQQ has one path. Every backtest you run is conditioned on that single realization of history.

(This is especially true of equities — FX has the advantage that you can use sampling windows for ticks, which provides greater disparity and hence great variety.)

But strategies don’t blow up on the past. They blow up on regimes that haven’t happened yet.

So I built something that I’ve been wanting to for a while:

A synthetic data generator — a reproducible dataset that looks and feels like any ticker I choose, but follows entirely new price paths, vol regimes, and macro-shock behavior.

This lets me test my strategies on unseen-but-familiar data to see what survives outside the historical record.

My first use case was to see most recent hybrid ML ensemble would really work as well in these synthetic scenarios. As it turns out, it works well-enough, but still at a degraded performance when tested against the synthetic data.

1. Why Synthetic Data?

Because overfitting is sneaky.

Every time I tune thresholds, pick hyperparameters, or choose a sleeve to keep, I’m subconsciously optimizing for the one timeline I have: 1993–2025 SPY.

Synthetic data gives me:

fresh paths that follow familiar statistical structure

alternative regimes that didn’t appear historically

macro shocks that mimic 2020-style chaos without reusing 2020

longer forward samples (e.g., 2026–2031)

stress environments beyond anything in the actual SPY tape

And most importantly:

It reveals which models are brittle — the ones that quietly overfit calm regimes or rely on structural assumptions that break fast.

2. First Version: A Bootstrap-Based Synthetic SPY

The first generator I built was simple but effective:

Block-bootstrapped log returns

Sample historical 5-day return blocks from SPY

Glue them together to form a new time series

Preserves clustering, serial correlation, and volatility bursts

Realistic high/low/open/close reconstruction

Rebuilt intra-block ranges and gaps

Ensured the synthetic OHLC data “looked” real

Microstructure noise

Resampled volume and trade counts

Added VWAP-based noise to mimic intraday behavior

Complete SPY-like schema

Same as my real data:

ticker, timestamp, open, high, low, close,

volume, trade_count, vwap, dateForward window

Generated business days from 2026–01–05 → 2031–12–31, seeded at the latest real SPY close.

The result was… surprisingly convincing. If I didn’t label the file, I could easily mistake it for historical SPY.

But there was a problem:

It lacked real regime structure.

The bootstrap reproduced SPY’s history faithfully — but didn’t create new dynamics.

So I upgraded it.

3. Version Two: Regime-Based Volatility + Macro Shock Injection

This is where things got interesting. I added a regime engine (because my middle name is chaos):

A. Three volatility regimes

Calm: low σ, low kurtosis

Normal: baseline

Volatile: elevated σ, fatter tails

With configurable:

dwell times

transition probabilities

per-regime volatility multipliers

B. Random macro shock injection

As in “give me a 5% down day even if the bootstrap wouldn’t normally produce one.”

Configurable parameters:

shock frequency

shock magnitude (e.g., ±1.5% → ±5% or more)

shock direction weighting

C. Block scaling

Return blocks are scaled by regime multipliers:

calm: σ × 0.5

normal: σ × 1.0

volatile: σ × ~2.0–3.0

D. Realistic tails

In one example run:

horizon: 2026–2031

σ ≈ 1.3%

shocks up to ±7%

frequent volatility clustering

This already looked more like a “future SPY variant” than a bootstrap remix.

I now have a CLI where all knobs can be set:

--calm-scale 0.5

--volatile-scale 2.2

--shock-frequency 0.05

--shock-min 0.015

--shock-max 0.05

--seed 777Different seeds → different synthetic universes. I plan to stash multiple versions as a synthetic suite for robustness testing.

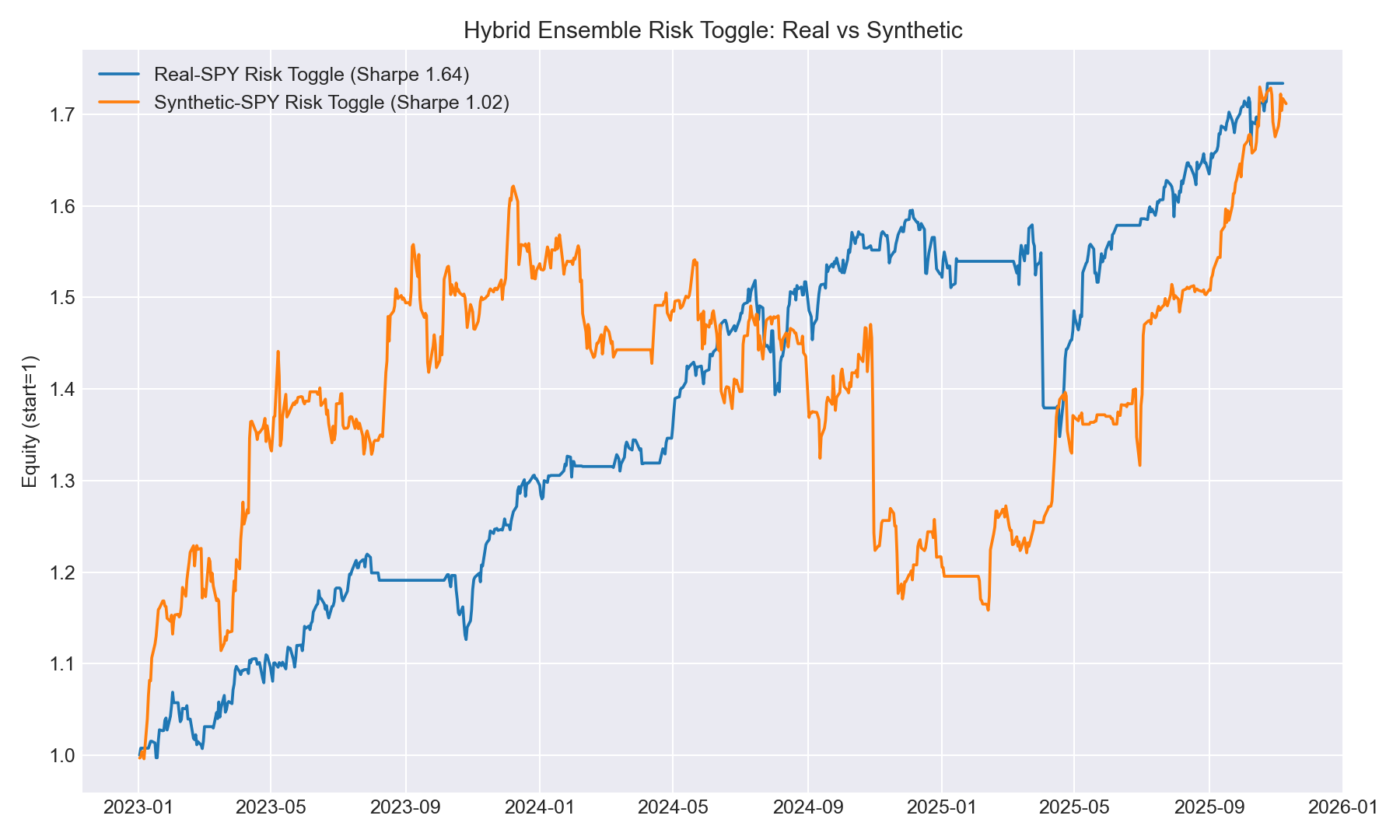

4. First Real Test: Run the Hybrid Ensemble on Synthetic SPY

I pushed the hybrid ML ensemble (the risk toggle from the last post) through both:

real SPY (final holdout 2023+), and

synthetic SPY (2026–2031)

Same model, same features, same thresholds but completely different environments.

Here’s what happened.

5. Results: Real SPY vs Synthetic SPY

A. Model performance (risk classifier)

Real SPY

ROC–AUC: 0.614

Accuracy: 0.697

Recall (stress class): 0.38

Synthetic SPY

ROC–AUC: 0.574

Accuracy: 0.643

Recall (stress class): 0.13

Interpretation: The hybrid model still works, but synthetic regimes break its ability to detect stress events. Shocks were too fast and too unfamiliar relative to training data.

B. Strategy overlay performance

Apply a simple toggle on SPY long exposure:

Risk Threshold: 0.4

Real SPY: ROI ~??, Sharpe ~1.6+

Synthetic SPY: ROI 113%, Sharpe 1.47, Max DD –21%

Risk Threshold: 0.5 (default)

Real SPY: ROI 73.4%, Sharpe 1.64, Max DD –15.5%

Synthetic SPY: ROI 71.2%, Sharpe 1.02, Max DD –28.6%

Risk Threshold: 0.6

Real SPY: Sharpe ~1.8

Synthetic SPY: Sharpe ~1.1

Interpretation: Synthetic shocks force the strategy into whipsaws more often, so bigger drawdowns and lower Sharpe.

The synthetic path was harder than real SPY.

C. Feature importance divergence

Real SPY (via SHAP):

rates vol (DGS1, DGS10)

yield-curve slope

FX/rates entropy

VIX beta

Synthetic SPY:

SPY skew

SPY kurtosis

entropy of SPY/VIX joint distribution

Interpretation: Real SPY’s stress is rate-driven but synthetic SPY’s stress (by construction) is price-driven.

The model is trained for the former — not the latter.

6. What I Learned

A. Models trained on calm-rate regimes underreact to shockier worlds

Because synthetic regimes injected faster, harsher volatility cycles, the classifier failed to identify stress early.

B. Toggle behavior degrades in unseen environments

Sharpe dropped from ~1.6 to ~1.0 with deeper drawdowns. The model implicitly leaned on rate-complex signals — and synthetic shocks didn’t follow those patterns.

C. This experiment gives me a path forward

I should retrain the ensemble using:

augmented data (real + synthetic)

volatility-aware calibration

macro-shock aware sampling

regime-balanced loss weights

D. Synthetic data is about resilience

Or as Taleb would call it, “anti-fragile.” After all, you’d want strategies that survive distributions you haven’t seen yet.

If you can’t find ‘em, make ‘em.

7. What’s Next

Build multiple synthetic universes. Different seeds, different parameters and a portfolio of synthetic tickers with various regimes.

Retrain hybrid ensemble on mixed real + synthetic. Make it robust to shocks not in the historical record (including some extreme ones).

Add synthetic paths to the dual allocator tests. Does the core engine survive “shockier” worlds? If not, I need structural changes.

Use synthetic stress windows for threshold tuning: Instead of tuning thresholds only on real history, tune on multi-world averages.

Eventually test the full blended portfolio (dual + trend + vol sleeve + toggle) — all on synthetic regimes.

Closing

Synthetic SPY isn’t meant to replace real data. It’s meant to answer one question:

Will my strategy survive a world that doesn’t look like the past?

As a next step, I hope to retrain the hybrid ensemble using synthetic regimes and see whether the Sharpe recovers.

The information presented in Math & Markets is not investment or financial advice and should not be construed as such.